Fixed Income Boutique

Based in Zurich and New York, the Fixed Income Boutique is an active manager aiming to capitalize on market trends and inefficiencies.

In our previous Fixed Income Quarterly publication, we highlighted the surge in investments in artificial intelligence (AI). Since then, this trend has accelerated at an impressive pace. This was evident during the most recent reporting season, as several hyperscalers significantly increased their already ambitious capital expenditure (capex) projections. For example, Google raised its capex forecast for 2026 to approximately USD 185 billion, a substantial leap from the 2025 level of around USD 91 billion.

This shift appears to reflect a broader industry trend, with hyperscalers moving away from the traditionally asset-light business model of previous years to a more capital-intensive approach.

As a result, we have already observed a wave of bond issuances from hyperscalers in the early weeks of 2026. Notably, Alphabet/Google executed a multi-tranche bond issuance in USD, GBP, and CHF in February. The GBP and CHF issuances were particularly remarkable, with issue sizes of GBP 5.5 billion and CHF 2.75 billion, respectively, across multiple tranches. These represent the largest corporate bond offerings in their respective markets in the past 20 years.

The GBP issuance was especially noteworthy, as it included a rare 100-year bond that attracted significant interest from investors eager to extend the duration of their portfolios. This overarching trend is expected to continue, and it would not be surprising if 2026 becomes another record-breaking year for bond issuances.

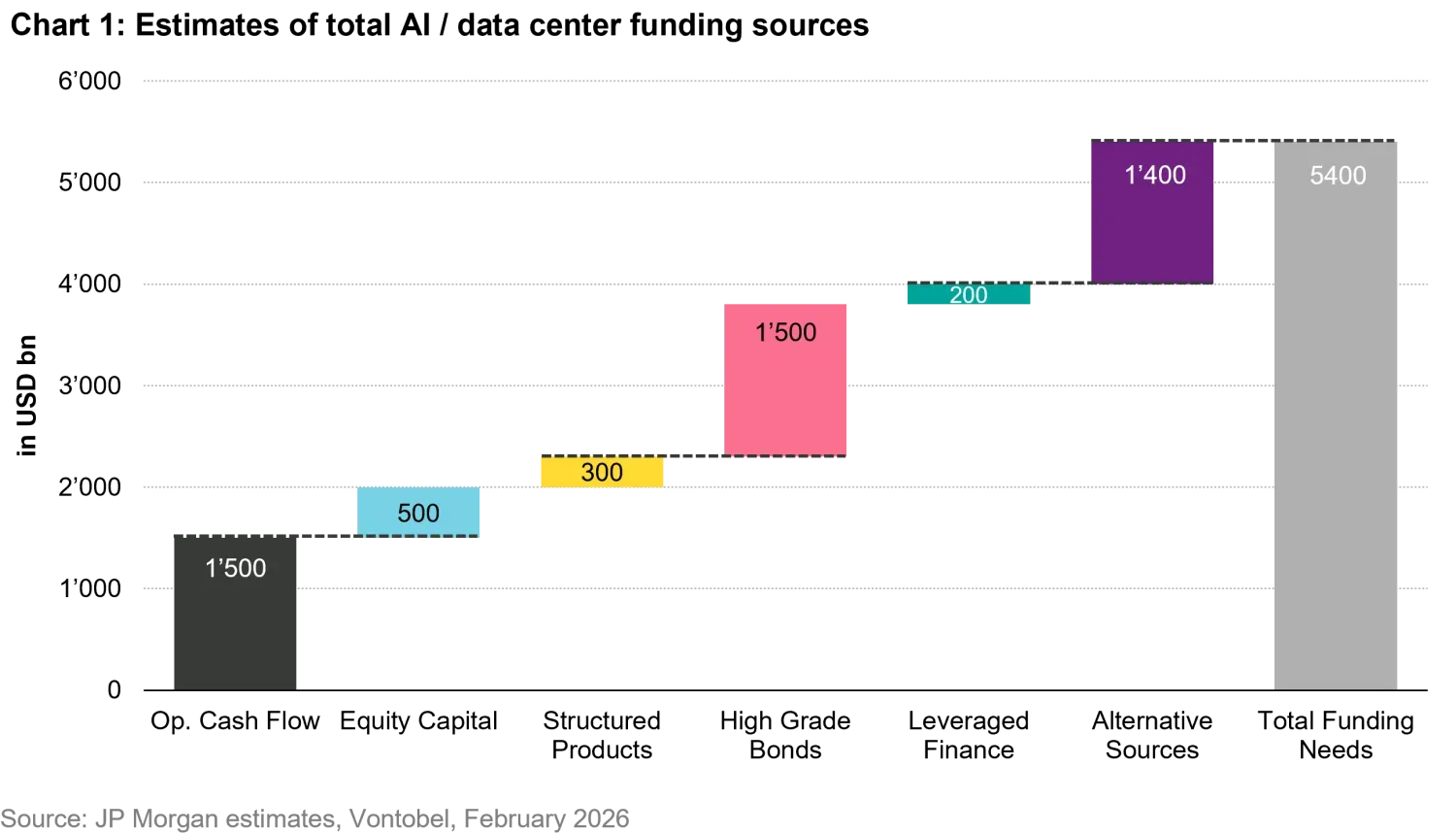

A key challenge for large US tech firms is ensuring that their ambitious capex plans are executed smoothly without causing market disruptions. We believe that these substantial investment requirements will be only partially financed through the public bond market, with other segments, such as private credit and leveraged finance, playing a significant role. Some estimates suggest that total funding needs for AI and data centers will exceed USD 5 trillion, with the majority expected to be financed through the public high-grade bond market, while a substantial portion is likely to come from the private debt market.

As a result, AI-related exposure is becoming increasingly widespread across asset classes and investment portfolios, heightening correlation risks if AI-related developments fail to meet market expectations. Indeed, it remains uncertain whether these investments will generate the anticipated revenues and cash flows. The stock market has already begun to question some of these ambitious plans, as evidenced by the underperformance of US hyperscalers relative to the broader equity market year to date.

In addition to ambitious funding plans, we believe investors may want to remain mindful of the evolving composition of many bond indices, which are likely to be reshaped by the surge in bond issuance. Historically, US banks, such as JPMorgan and Bank of America, have held significant weights in corporate bond indices, with Oracle being the only US tech firm among the top 10 largest issuers.

Looking ahead, assuming approximately 20% of the substantial capex requirements are financed through the public bond market, US hyperscalers could dominate these indices, potentially occupying 5 out of the top 10 positions. This would surpass traditional heavyweights like Citigroup and Goldman Sachs. As a result, the ongoing AI-driven capex boom will be increasingly difficult for investors to ignore going forward.

We believe the significant capex funding needs will likely impact the business models and credit profiles of the large US hyperscalers, shifting the sector from low to high debt levels. Spreads may widen due to increased issuance, while also potentially raising questions about whether this capex boom will ultimately translate into higher earnings and cash flows.

Passive investment strategies may face challenges as they replicate index weights, while active investors have the flexibility to adjust their positions, underweighting weaker firms and overweighting potential winners. We anticipate that dispersion within the sector may increase further from this point. Additionally, portfolio diversification will become increasingly important, with a focus on market segments that are less directly exposed to the AI capex boom. Such diversification can provide a degree of insulation in case outcomes turn unfavorable. We will continue to closely monitor developments in the ongoing AI revolution.

AI disruption continues to dominate investing headlines in 2026, and global high yield (HY) is no exception despite its relatively lower overall exposure. Initially, investors focused on bond issuance by hyperscalers to fund capex related to data centers. This focus shifted to software in mid-January, following the watershed moment of Anthropic’s release of the Claude Cowork AI tool and the subsequent threat to software providers.

The rise of agentic AI and its perceived impact on multi-step workflows have sparked a powerful debate. The central question is whether the proliferation of AI agents will lead to the rapid replacement of existing software tools or if the transition will be more complex, given the challenges of replacing embedded institutional knowledge.

Regardless of the outcome of this debate, AI is reshaping the technology segment of the HY market. What was historically a carry-efficient beta trade is evolving into a deep-dive credit selection opportunity set. While increased volatility may offer tactical entry points, we believe successful allocation will depend on the ability to differentiate between temporary valuation dislocations and permanent technological obsolescence.

In this article, we highlight the drivers and degree of volatility within the HY market and how we are carefully navigating the software and technology sectors to identify attractive alpha opportunities.

Technology and software issuers have historically traded at tighter spreads within HY, supported by (i) recurring revenues, (ii) asset-light business models, and (iii) strong free cash-flow generation. However, the emergence of agentic AI introduces a challenge to the defensibility of selected workflow-driven software models, particularly those reliant on user-interface-driven workflows and seat-based pricing structures.

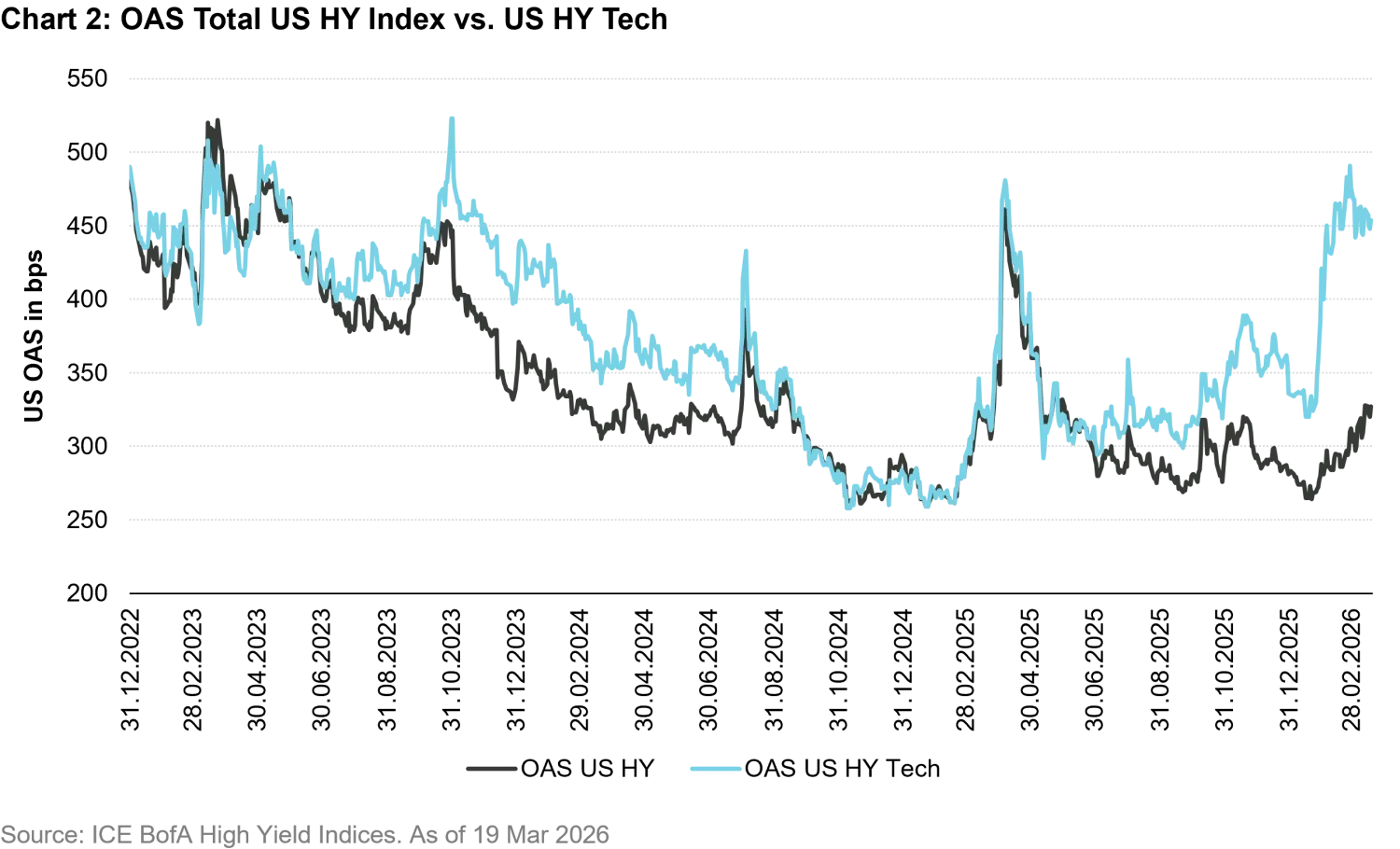

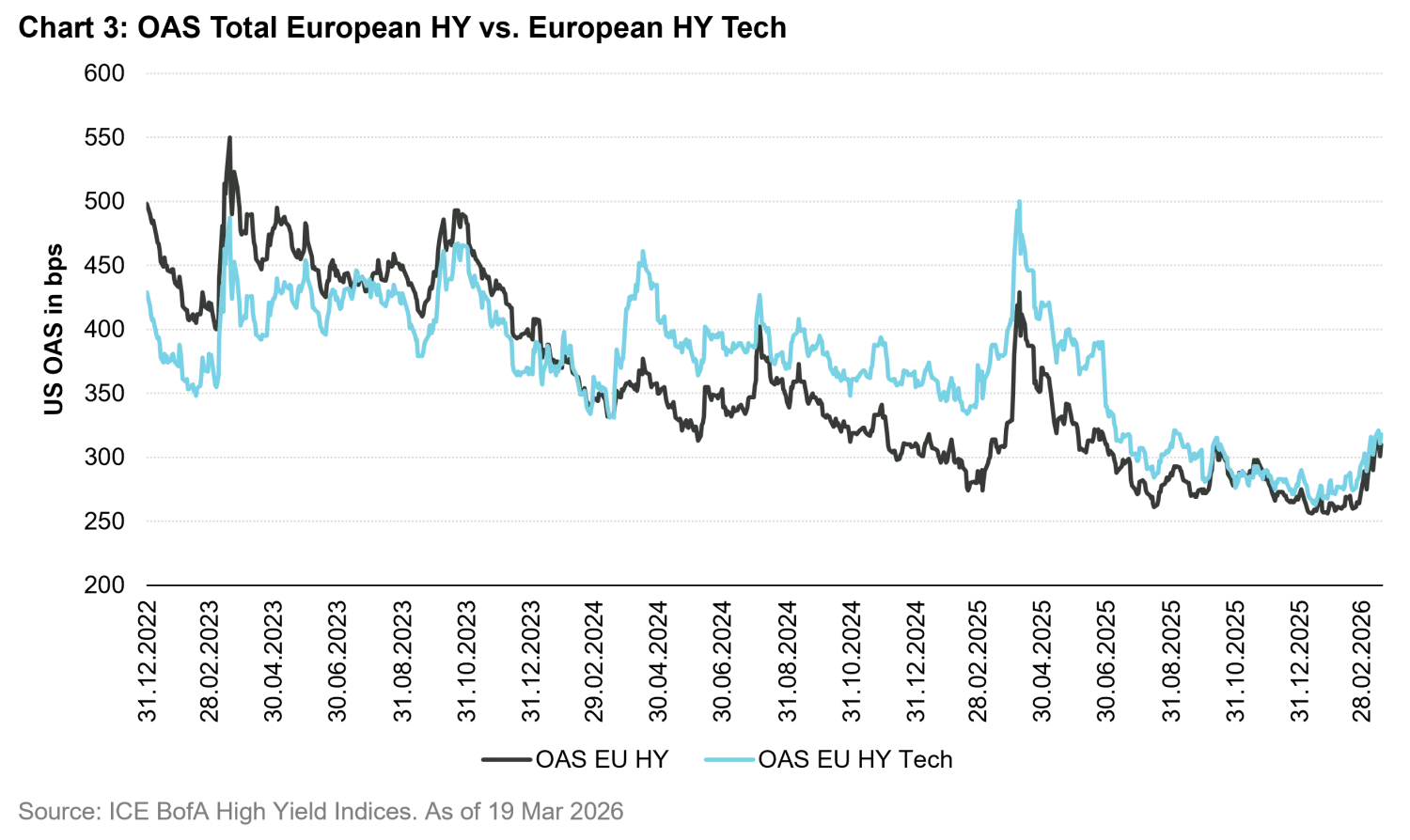

Since January 2026, US HY technology spreads have widened by approximately 130 basis points (bps) compared to the broader HY index (Chart 2). This repricing reflects a combination of lower equity valuations, heightened perception of refinancing risks, and expected pricing pressure across SaaS models. In EU HY technology, the spread widening was initially 30 bps but has narrowed to roughly 8 bps, driven by recent geopolitical developments that have since evened out the playing field (Chart 3).

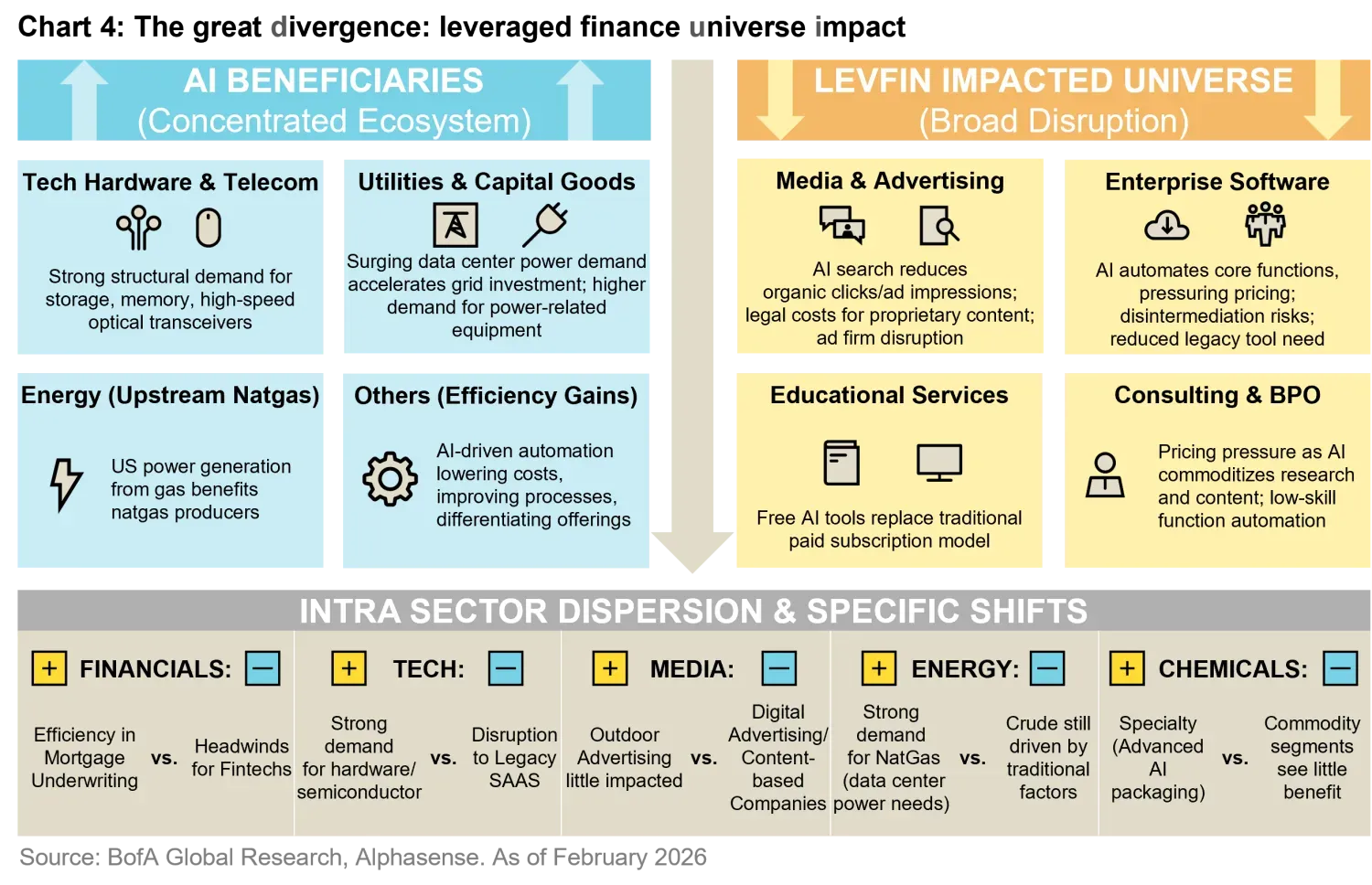

Despite what appears to have been a broad-based sell-off, this AI disruption is introducing structural dispersion rather than a broad-based deterioration in sector fundamentals. This creates opportunities for investors to generate excess total returns by identifying credits with sound underlying fundamentals, while also increasing the risk of allocating capital to issuers exposed to structural AI-driven disruption.

One key consideration is that current and near-term expected performance remains strong for most issuers in software and technology. The decline in equity valuations appears to be more related to concerns about the sustainability of this performance over the longer term, which has led to a decline in terminal values. When evaluating potential winners and losers at this stage, business models that boast solid vertical integration and/or those requiring high trust and reliability tend to have a higher cost of failure and, therefore, face lower risk. On the other hand, products centered around content creators and data analytics can be viewed as higher risk.

Larger but still growing software firms can benefit from the use of AI tools, as these tools can reduce engineering costs and help offset margin erosion associated with both higher AI model development costs as well as declines in seat-based pricing (as fewer humans may be needed to perform increasingly complex functions). Finally, the quality of management teams remains highly important as they must effectively deploy AI within their business to remain competitive while ensuring that their services remain relevant and necessary.

When comparing US and European subsectors, we do note some broad differences. The European HY technology sector is over 6% of total market exposure and is more concentrated in IT services and telecom-adjacent infrastructure. As such, it features lower exposure to venture-style SaaS growth models, which helps explain the relative stabilization in these credits, despite AI disruption remaining a key concern.

The technology exposure in US HY is similarly low, at 4%, but within the software space, it does have a larger share of sponsor-backed issuers that tend to have higher leverage. While cash flow remains the focal point, credit spreads in the US appear more closely correlated to public market equity prices and a stronger reliance on enterprise valuations. Bond issuers do benefit from lower loan-to-value (LTV) ratios, although there are some reduced recovery expectations for unsecured creditors.

It is important to understand market themes and drivers of credit spread volatility within sectors in order to identify attractive idiosyncratic opportunities. The broad sell-off has clearly created some interesting investment opportunities, but as always, timing is critical, especially when assessing risks associated with rapidly evolving technological changes. As such, we focus on companies with strong market shares and defensible business models that provide critical products and services, where improper substitution would carry a high risk of failure. AI disruption is unavoidable, but we believe the winners will be able to improve cash flows through production efficiencies both internally and for their customers.

The Swiss bond market began 2026 with strong momentum. By mid-February, the Swiss Bond Index (SBI) gained +1.23%, marking one of its strongest starts in recent years. New issuance activity remained elevated, and the prominent AI-driven capex theme has now reached Switzerland. A landmark CHF 3.05 billion multi-tranche transaction by Alphabet (Google) brought global attention to the CHF credit market, temporarily widening A-rated spreads by 5 – 10 bps.

A significant portion of this transaction was financed through pronounced selling of Swiss government bonds, which triggered a sharp repricing in the sovereign segment. The 10-year point widened by roughly 15 bps versus swaps, thereby normalizing previously stretched levels.

Despite this repricing, primary markets remain aggressive. Many new issues are priced at or even inside outstanding issuer curves, offering limited concessions to investors. We therefore favor maintaining a disciplined and selective approach when adding credit exposure. Although valuations are elevated, we see limited near-term catalysts for broader spread widening in the current low-yield environment, where investors continue to compress risk premia in search of incremental carry.

We favor an overweight position in shorter-dated credit to capture additional yield while limiting spread volatility. We remain cautious on lower-rated or subordinated bonds offering insufficient compensation. In the foreign segment, selective opportunities persist, particularly among financial issuers trading at attractive levels in CHF relative to EUR or USD markets.

On rates, we expect the 10-year CHF swap rate to fluctuate within a 0.40% - 0.65% range and recommend tactical positioning within that corridor. Meanwhile, the CHF has appreciated against both the EUR and USD, increasing speculation about potential intervention by the Swiss National Bank (SNB) and a possible return to negative interest rates. We do not view another rate cut as imminent and expect the SNB to remain on hold. Should the Governing Board decide to ease policy, however, we would anticipate a decisive 50 bps cut accompanied by adjustments to the current tiering framework.