Emerging Markets Bonds

A high-conviction and contrarian approach, combining bottom-up and relative-value strategies.

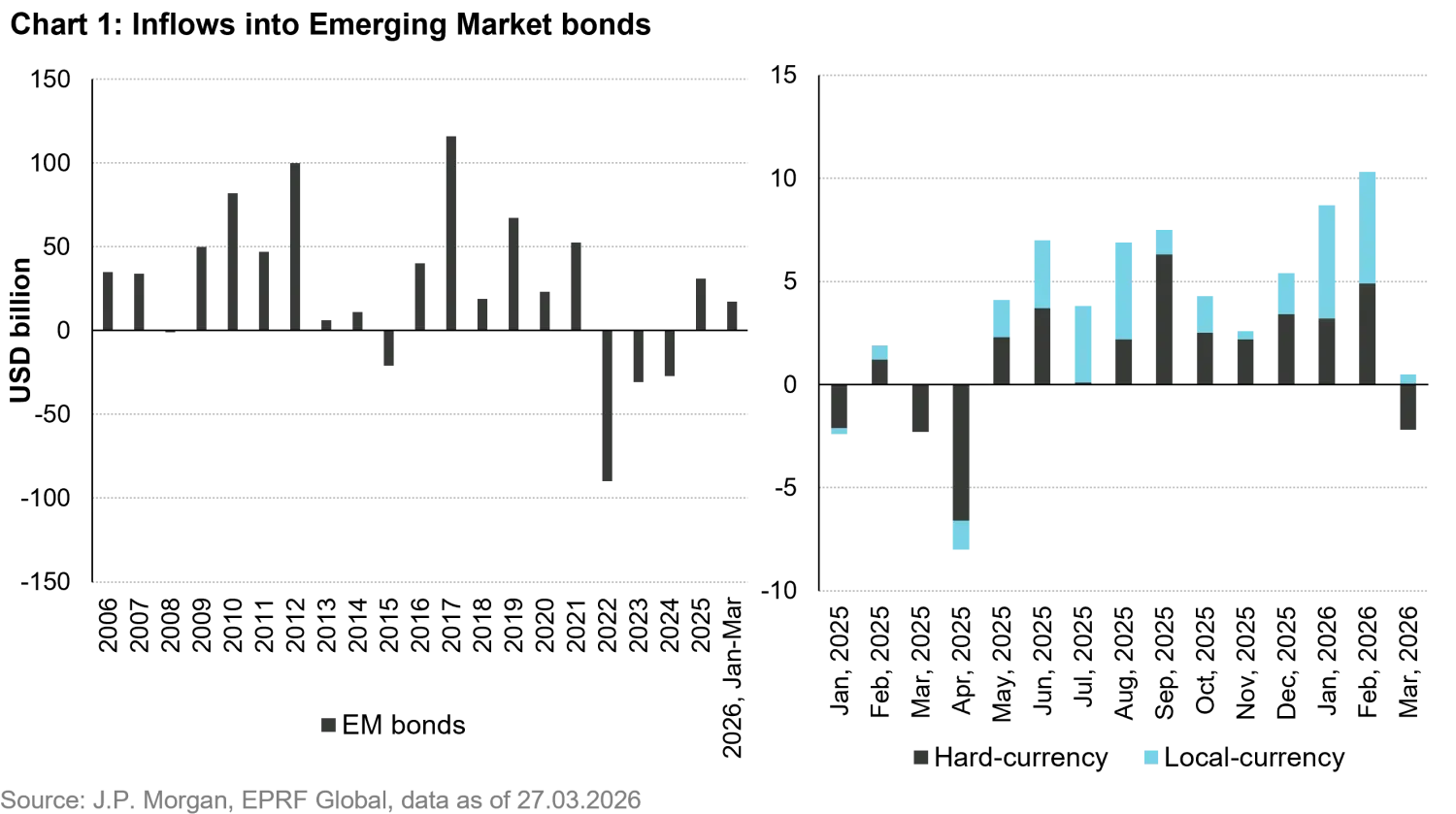

In December, we published an optimistic outlook for Emerging Market (EM) bonds, which proved to be correct until the end of February. As we had expected, the positive credit rating trend among emerging sovereigns, underpinned by a significant accumulation of foreign exchange (FX) reserves through 2025, continued. This, combined with elevated global equity valuations, favorable inflation dynamics in most EMs, and faster-than-expected global growth and the search for diversification away from the US, resulted in an acceleration of inflows into EM bonds during the first two months of the year. These inflows, in turn, supported further spread compression in January and February, until the onset of the war in Iran.

As depicted in Chart 1, EM fixed income experienced some outflows in March. However, this trend was not unique to EM; developed market credit also saw outflows, reflecting a broader albeit modest global derisking.

In March, the blockade of the Strait of Hormuz triggered a sharp spike in oil prices that fundamentally changed the outlook for the global economy and asset prices. The markets’ reaction has been significant but relatively contained, considering that this is the largest disruption to global oil supply in history (approximately 13-15% after considering oil rerouting via pipelines). For comparison, the disruption was approximately 10% during the 1956 Suez Crisis, 7-9% during the OPEC oil embargo in 1973, and the Gulf war in 1990. The International Energy Agency’s agreed release of 400 million barrels from global stockpiles can only be deployed at an average pace of 3.3 million barrels per day. It is not enough to compensate for the supply shortage, requiring oil prices to remain above USD 100 per barrel to cause demand destruction.

There are good reasons for this relatively contained correction. The Trump administration has strong incentives to keep its word regarding the relatively short duration of the conflict. Politically, an inflation spike driven by higher oil prices could be very costly ahead of the mid-term elections in November, especially given that Trump campaigned against “forever wars.” At the time of writing (third week of March), Trump appears to be looking for ways to de-escalate the conflict.

From a military perspective, there are concerns that the US and its allies could deplete their stockpiles of anti-ballistic missile ammunition and interceptors before Iran runs out of missiles – i.e., unless most Iranian missile launchers are destroyed first. From a resource point of view, some countries and entire industries could face physical shortages of oil, helium, and other commodities.

EM fixed income has been resilient to the shock. EM hard-currency sovereign bonds (EMBIG Diversified) declined by 3.3% in March, a similar performance to the 3.1% decline in the Bloomberg Global Aggregate (Legatruu Index) over the same period.

EM corporate bonds (CEMBI BD) held up even better due to their lower duration, declining by 1.8%. Importantly, 1.4% of the EMBIG’s 3.3% decline was due to spread widening, while only 0.6% of the drop in the CEMBI was due to higher spreads, while the rest of the negative return was explained by higher US Treasury yields, implying that, even in this risk-off environment, markets remain relatively sanguine about EM.

EM local-currency bonds (GBI-EM) experienced a more pronounced decline of 5.5%, which is partly explained by the 2.4% recovery of the US dollar vs its main peers (DXY index). Importantly, once carry is included, EM FX performed in line with the euro.

The second element explaining the relative underperformance of local-currency bonds is that EM yield curves sold off more aggressively than developed-market (DM) curves. Several local-currency yield curves are now pricing in rate hikes by many EM central banks, a scenario we doubt will materialize. That said, the reaction of EM local-currency bonds has been relatively contained when compared to Emerging Market equities, with the MSCI EM down by 13.3% in March.

There are some similarities to the 2022 oil shock but also some key differences. The magnitude of the oil supply disruption is even larger, but the price reaction has been more contained due to expectations of a shorter conflict. Additionally, global macroeconomic conditions today are very different. After the pandemic, both monetary and fiscal policy were extremely loose. While fiscal policies remain lax in the developed world, monetary policy globally has been tight for the past four years. The 2022 oil shock played a role in the inflation spike of that year but was not the sole cause. Other factors, such as extremely loose monetary policies, supply constraints, and rapidly recovering aggregate demand after the pandemic, also contributed to the inflation overshoot.

In 2022, interest rates had to adjust sharply from historically low levels, while the required adjustment today would be much smaller even if the current oil shock persists. This difference in the macroeconomic backdrop suggests that the market correction currently required is smaller than the one seen four years ago, despite the larger oil supply shock.

This resilience is justified by the fact EMs have larger buffers today than during the 2022 oil shock, in our view. Four years ago, many EM economies had not yet fully recovered from the pandemic’s impact. Tourism-dependent economies were in particularly bad shape, and most high yield (HY) issuers had lost market access. Although debt burdens remain heavy for many EMs, external accounts appear healthier for most countries. This improvement is reflected in the significant accumulation of FX reserves, which we will discuss in detail below.

EMs have not lost market access this time around, while many issuers are postponing new issuances until market conditions improve. Others, including low-rated sovereigns, like Angola and Egypt, have been able to issue Eurobonds even during these volatile markets. In fact, B-rated sovereign spreads remain below 400 basis points (bps), having only retraced to their September 2025 levels, which are below their long-term average. Thus, we believe market conditions would need to deteriorate significantly for HY issuers to face the same loss of market access experienced in 2022.

An important factor preventing such an event is that EMs have already gone through a full cycle of defaults between 2020 and 2023. Fragile sovereigns and corporates have already defaulted and restructured their debts and have repaired their balance sheets. As a result, the asset class may be more resilient to turbulence compared to four years ago.

EM issuers have also undertaken significant liability management operations over the last two years. In 2025, EM sovereigns issued a record amount of hard-currency bonds, according to JP Morgan data, which included a large amount of liability management operations and hence significantly reduced or eliminated maturity walls for the next two years.

The Middle East is in the eye of the storm, but it’s not among the hardest hit regions and has not been a drag on the broader EM asset class. This contrasts with 2022, when countries directly involved in the Ukraine war suffered the most and hurt the performance of the asset class. Ukrainian bonds were restructured and lost three quarters of their value in 2022, while Russia and Belarus were sanctioned and legally unable to continue servicing their external debt.

This time around, Middle East bonds are not suffering disproportionately, despite being in the eye of the storm. Almost all Gulf countries are high-quality investment grade (IG) issuers, with strong balance sheets and sufficient buffers to withstand a prolonged period of significantly reduced oil and gas exports.

For example, Saudi Arabian sovereign bonds have declined by 2.6% this month, primarily due to higher US Treasury yields and have actually outperformed the EMBIG index. UAE bonds are down 4.3%, with more spread widening, reflecting the greater impact of the conflict on its economy. Meanwhile, Saudi and UAE corporates are down 3.4%, and 3.5%, respectively, and Midde East corporates are down 2.6% on average, which isn’t much worse than the CEMBI BD index.

Chart 2: What’s different today vs 2022? Contained market and inflation impact

| 2022 oil shock | Today’s oil shock | |

|---|---|---|

| Macro economic conditions | Extremely loose monetary and fiscal policies before the war; Interest rates had to adjust sharply from historically low levels. | Tight monetary policy globally for past 4 years and fiscal policies remain lax only in DMs. Smaller adjustments needed, even if the oil shock persists. |

| EM buffers | EM economies recovering from pandemic; tourism-dependent economies vulnerable. | EMs have healthier external accounts; significant accumulation of FX reserves. |

| Market access | Many HY EM issuers lost market access. | EMs have retained market access. |

| Debt restruct- uring | Fragile EMs had not yet gone through debt restructuring. | 2020-2023: fragile EMs defaulted, restructured debts, and repaired balance sheets. |

| Regional impact | Countries involved in the Ukraine war suffered severely, dragging down the broader EM asset class. | Middle Eastern bonds are not disproportionately impacted; almost all Gulf countries are investment-grade issuers. |

Source: Vontobel

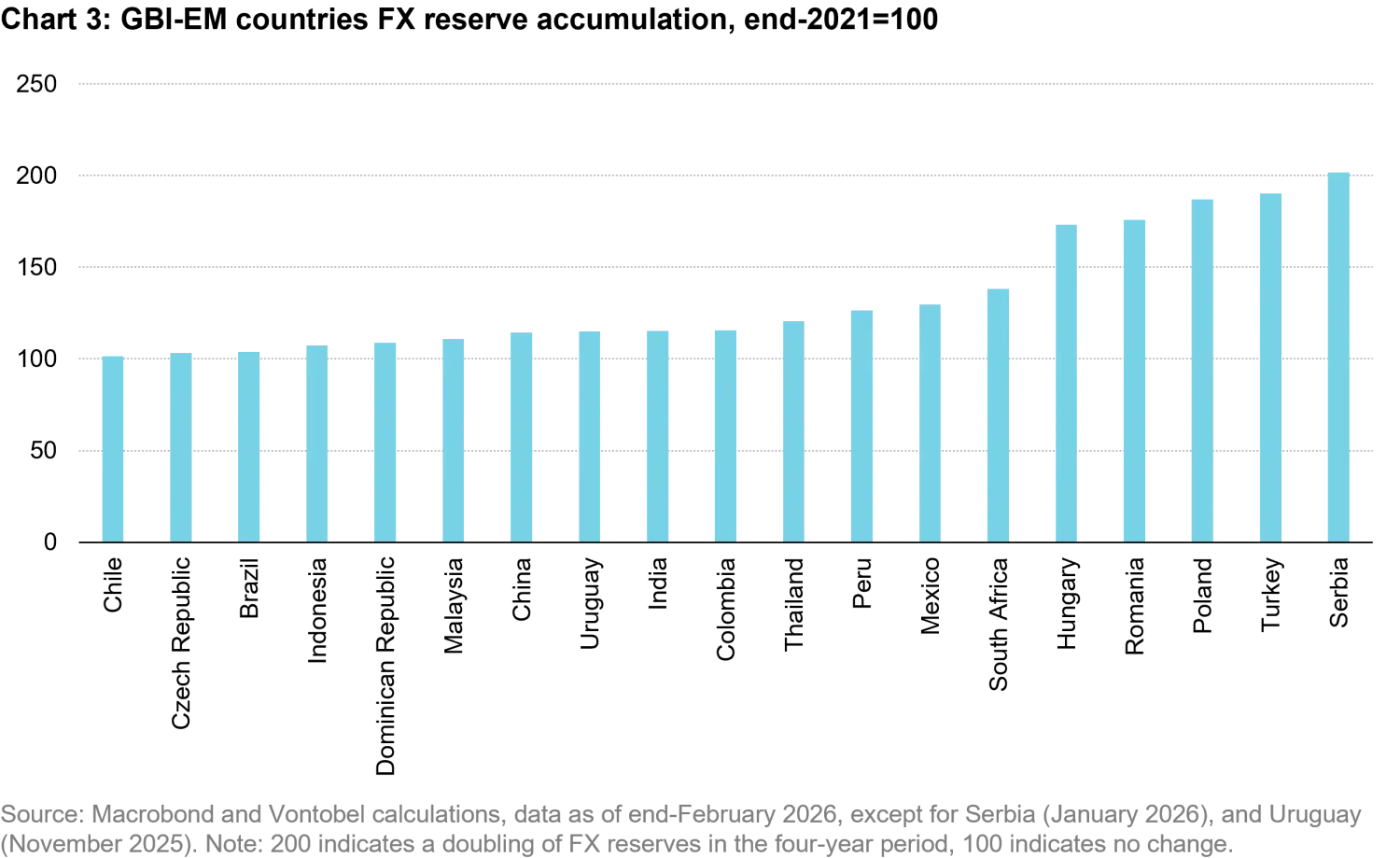

In the last four years, all 19 GBI-EM countries accumulated FX reserves (Chart 3). These countries are typically larger, liquid EMs with developed local-currency markets. This reflects improved balance of payment positions. In other words, even typically fragile countries with historical twin deficits (like Turkey) are in a stronger external position today compared to four years ago.

Some highly-rated countries, such as Chile and Czechia, or those like Brazil that were already in a strong external position, have not significantly increased their reserves, while others have seen their reserves grow by more than 50%. Turkey’s policy turnaround after the appointment of Mehmet Şimşek as Minister of Treasury and Finance in 2023 has been quite impressive, even though the country has not yet completed its macroeconomic adjustment. This reserve cushion has enabled the Turkish central bank to maintain its usual pace of currency depreciation, outperforming other EM currencies, which is exactly the opposite of what occurred in recent crises.

Central and Eastern Europe (CEE) stands out as one of the largest accumulators of FX reserves among GBI-EM countries, and that matters in this context because CEE countries are heavily dependent on energy imports. Serbia, for instance, has leveraged its booming Information and Communications Technology (ICT) sector to more than double its FX reserves over the past four years.

In Poland, the central bank has purchased over 300 tons of gold in the last three years, making it the largest gold buyer in the world in 2025. Poland and Hungary’s trade balances have structurally improved as they have become the key battery production hubs of Europe. Poland is now the second-largest exporter of electric batteries (after China). Electric battery and EV production has also grown fast in Hungary, enabling the country to successfully navigate the relative decline of German internal combustion engine (ICE) vehicles and parts manufacturing.

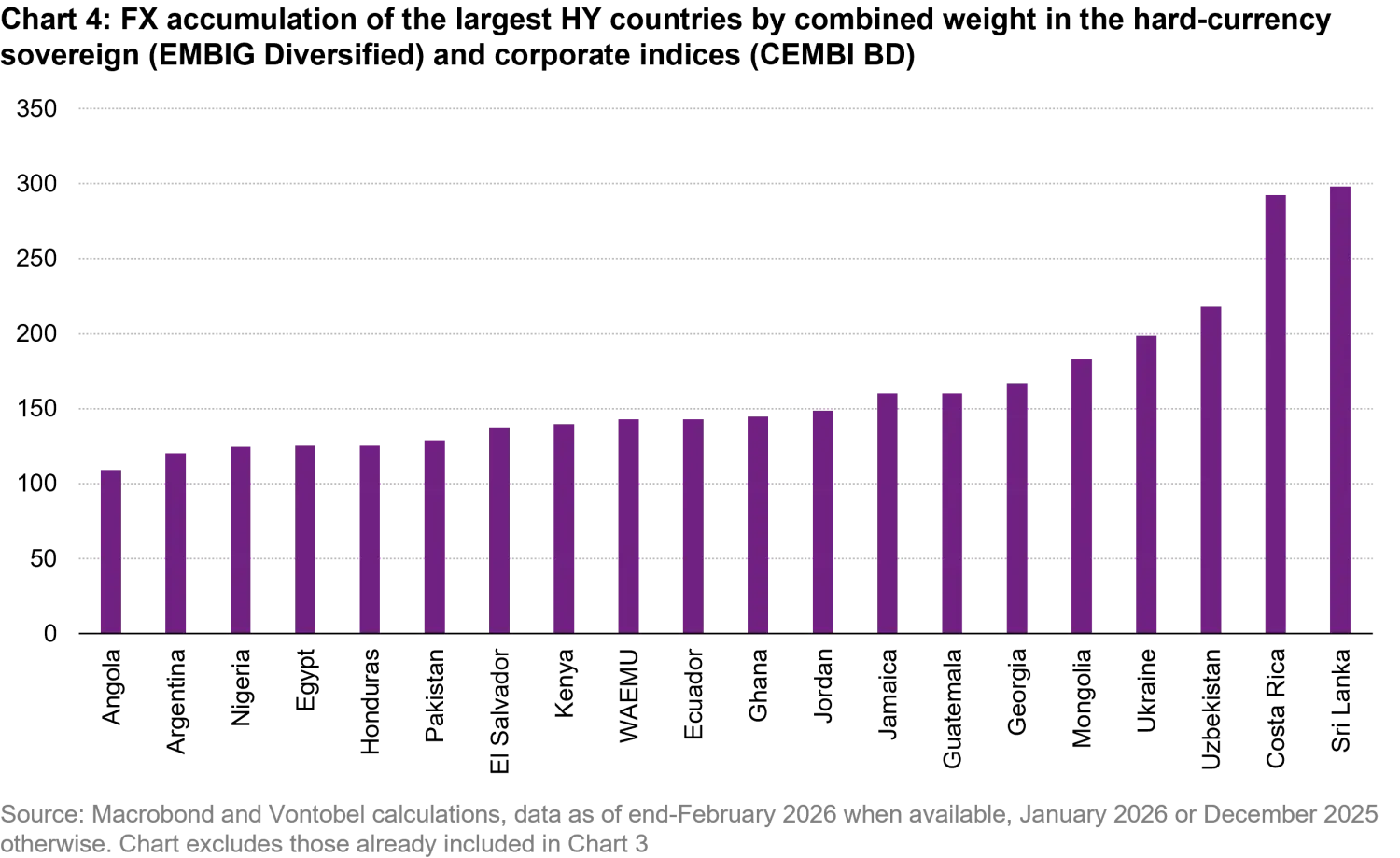

FX reserve accumulation matters the most for HY countries, particularly those with the lowest credit ratings, which can occasionally lose market access, as was the case in 2022. In Chart 4, we focus on the largest HY countries by combined weight in the hard-currency sovereign (EMBIG Diversified) and corporate indices (CEMBI BD) with available data, excluding those already included in Chart 3.

All of these top 20 largest HY countries (that are not in the GBI-EM) have accumulated FX reserves. Sri Lanka stands out, having almost tripled its FX reserves, albeit from a critically low level. After defaulting in 2022, Sri Lanka completed a debt restructuring in 2024 and has since been on a successful IMF program, which has allowed it to regain macro stability. Costa Rica also stands out, as its central bank has been purchasing FX reserves to avoid excessive currency appreciation amid a booming MedTech export sector and strong tourism.

In our view, a few global trends have supported FX reserve accumulation in several countries:

We believe the oil & gas sector still offers value even after outperforming in this market. However, the unanswerable question is how long the war, and its associated oil shock, will last. And given this uncertainty, we find it appropriate to maintain overweight positions to oil-exporting countries and oil & gas companies, as this appears to be one of the few investments that can partly hedge portfolios from a longer-than-expected conflict.

Moreover, even if the war in its intensity is over and the Strait of Hormuz fully reopens in the next few weeks, we think it is likely that oil will continue trading with a USD 10-15 per barrel risk premium as Iran is likely to maintain leverage over the Strait of Hormuz. We believe a world with an oil price in the mid-to-high USD 70s is much more favorable for oil producers than markets expected at the start of the year, and thus we think that the outperformance of energy producers month-to-date makes sense.

The damage to the Ras Laffan LNG facility in Qatar could remove c.17% of the country’s LNG capacity for the next 3–5 years. This is supportive for companies providing LNG infrastructure across liquefaction, transport and regasification, particularly those with floating liquefied natural gas (FLNG) assets—offshore units that process and liquefy natural gas at sea for export—as it reinforces the value of non-Hormuz supply routes and improves near-term visibility on project pipelines.

Overall, the war is a net positive for FLNG infrastructure players, with stronger demand for diversified gas supply, improved pricing power on contract renewals, and greater scope to monetize commodity-linked upside. Going into the conflict, we were already exposed to the only EM player providing these services, and its bonds have performed well (+6.7% year-to-date), reflecting the improved underlying fundamentals.

Local-currency is likely to rebound strongly in a de-escalation environment. As mentioned earlier, local-currency bonds have been hit harder during the current market turmoil. We believe this is partly due to a stronger dollar, which has once again rallied in a risk-off event, as it typically does. Additionally, since the US has been a net energy exporter since 2014, it stands to reason that the US dollar would fare better than the euro and the currencies of energy-importing EM markets.

However, the story is not all about the dollar. EM rates have also increased more sharply than US Treasury and German bund yields. The GBI-EM yield to maturity increased by 56 bps in March to 6.4%. This increase is much more likely a result of carry trade positioning, driven by technical factors and de-risking, rather than fundamentals.

Index composition also plays a role. The GBI-EM has become an oil importer, on aggregate, since Russia exited the index in 2022, while the EMBIG remains an oil exporter, on aggregate. That said, the inflationary impact of the current oil shock on GBI-EM countries should be lower than that on the eurozone, as the GBI-EM index still includes a few oil-exporting countries. In our view, there are no reasons to believe that the credibility of EM central banks’ inflation targeting regimes will be undermined by this shock; on the contrary, they have gained credibility relative to DMs over the past four years.

Thus, while the GBI-EM was hit harder, it should also rebound more strongly upon a de-escalation event, if it occurs in a relatively short time frame. While adding duration during an inflation shock is typically a risky proposition, we believe it is less risky to do so in EM than DM, given the stronger correction in EM rates.

Overall, we believe EM fixed income is in a better position today than four years ago. This, combined with still high equity valuations and abundant global liquidity, justifies a more moderate market reaction so far in our view, despite the uncertainty surrounding the duration of the war and the significant magnitude of the oil supply disruption. If a de-escalation event materializes in the short term, we think the asset class is well positioned for a strong rebound amid a likely resumption of most of the pre-war global market trends including diversification away from US-centric portfolios.