For a year, investors debated how quickly central banks would cut rates. An exogenous shock has since flipped the question to whether any rate cuts will occur at all. The US and Israel’s attack on Iran in late February led to the closure of the Strait of Hormuz, a route that carries a fifth of the world's seaborne oil. The resulting spike in energy prices pushed inflation higher across all major economies just as it appeared to be under control.

In a single week in June, three major central banks responded to this changing backdrop from different starting points, yet all moved in a more hawkish direction: the European Central Bank (ECB) implemented its first hike in nearly three years, the US Federal Reserve (Fed) delivered a hawkish hold, and the Bank of Japan (BoJ) raised rates for the fifth time.

The ECB: If all you have is a hammer, everything looks like a nail

After the Iran conflict dragged on longer than markets had hoped, with the Strait of Hormuz remaining largely blocked for more than three months and Brent crude trading well above USD 100 for extended periods, the resulting jump in energy prices pushed euro area inflation higher and unsettled inflation expectations. Despite weakening economic activity and a softening growth outlook, the ECB felt compelled at its June meeting to raise policy rates by 25 basis points, lifting the deposit rate to 2.25%. Faced with rising prices, the ECB inevitably reached for familiar tools.

Because neither the ECB nor the market can forecast how the Gulf, and therefore oil, will evolve, President Christine Lagarde emphasized that further decisions would remain data dependent. The Governing Council is working meeting-by-meeting and has explicitly declined to commit to any future rate path, framing the latest hike as a sensible response that would hold up across a range of scenarios, rather than the start of a new tightening cycle.

That leaves the ECB with plenty of flexibility. For now, however, there are few catalysts pointing toward lower rates, even after the ECB incorporated a "milder" energy price scenario into its projections, in which core inflation remains at 2.5% in both 2026 and 2027. Following the meeting, the market, contrary to our view, continued to price in more than one additional rate hike this year, encouraged by Lagarde's assessment that services inflation had become broader-based.

Here is where we part company with consensus. Even before the reopening of the Strait, we saw no evidence that the energy shock was feeding into wage growth, nor any indication of wages and prices starting to chase one another. The ECB's own wage tracker supports this view, with bargaining pressures stable into 2026.

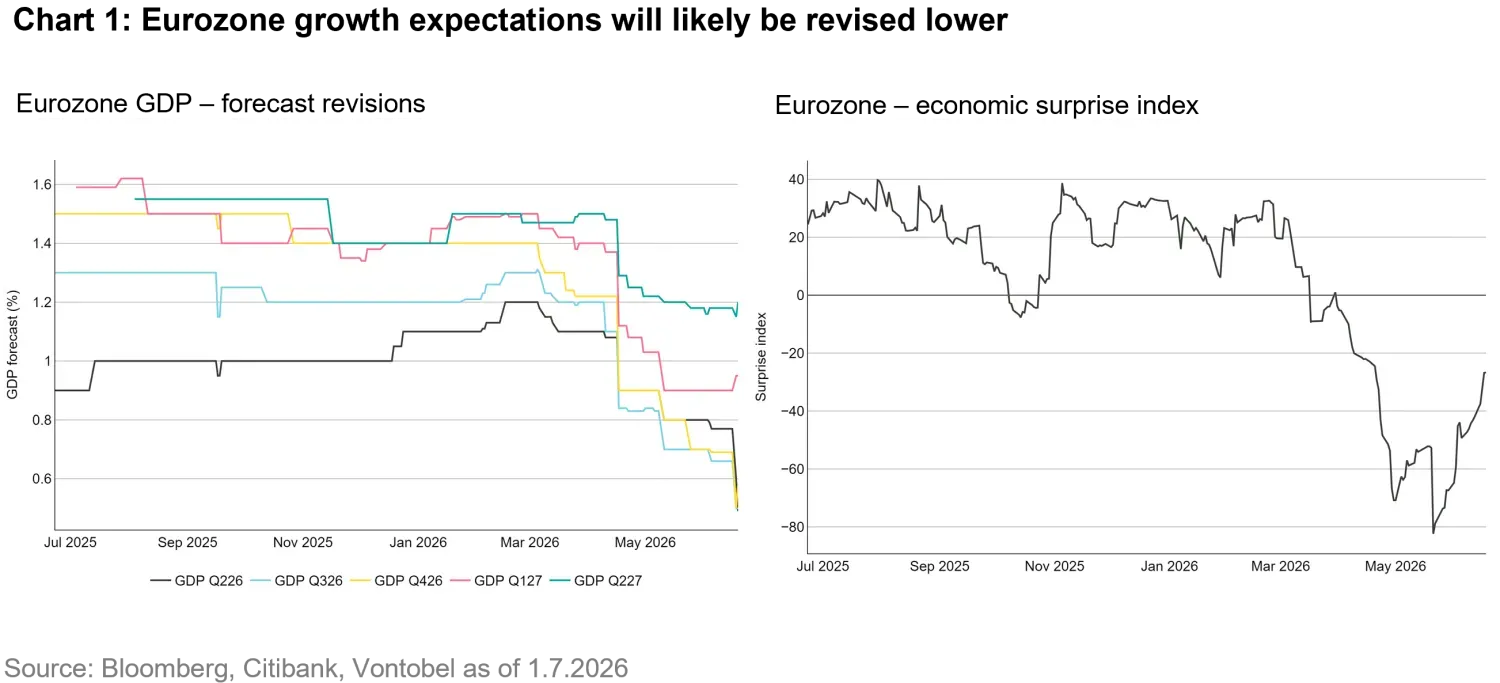

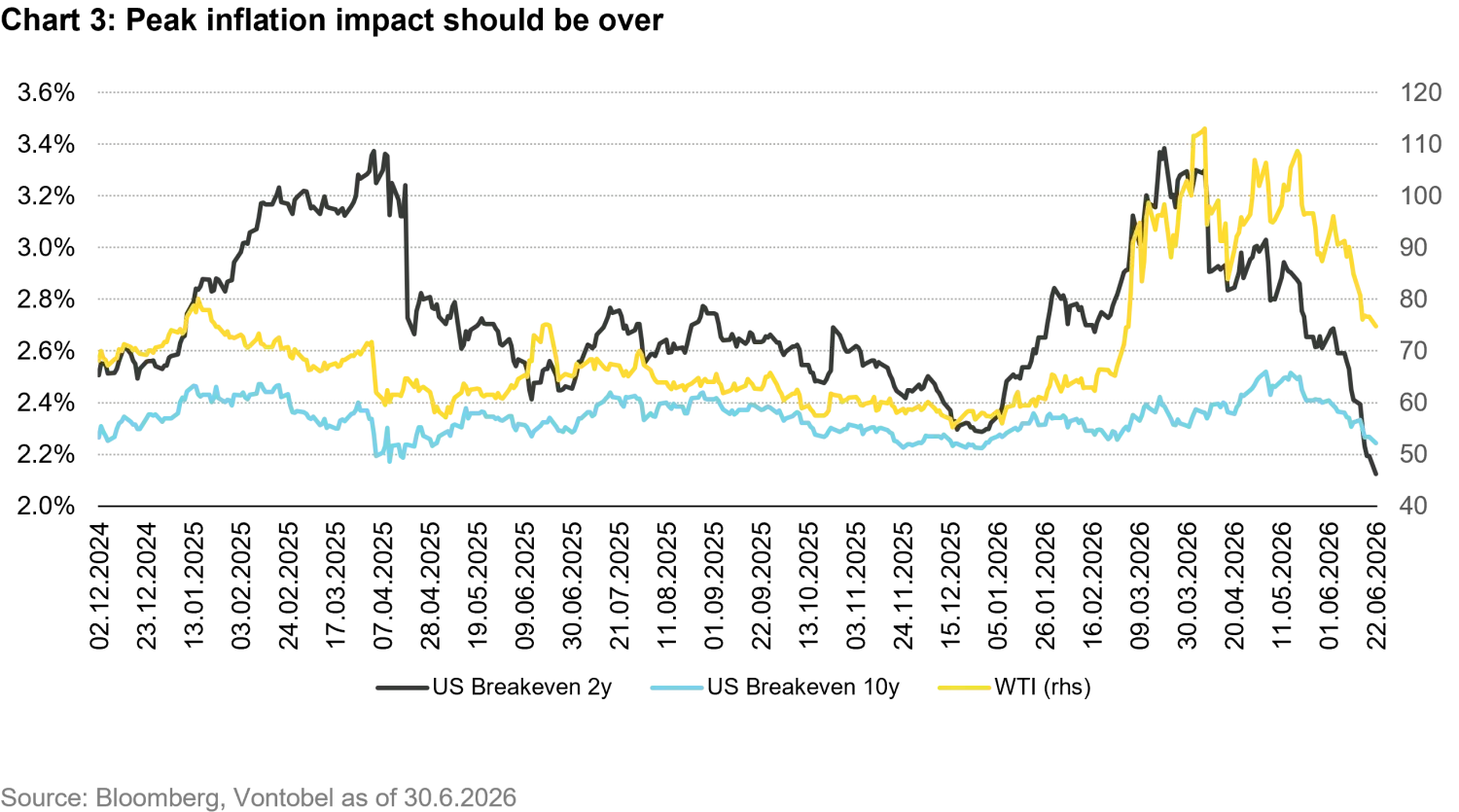

That structural argument has now been joined by a decisive cyclical one. With an agreement reached and the Strait reopening, Brent crude has fallen by roughly 40% to its lowest level in three months, near USD 76 per barrel. At the same time, the International Energy Agency (IEA) is warning of a supply glut in 2027. A supply shock that is visibly unwinding does not, in our view, call for more tightening.

On the growth side, we see more downside risk and fear that markets are still too complacent about the adverse effects of the supply shock on real activity. Growth expectations will likely be revised lower over the coming months, which makes further rate hikes unlikely, in our view. Taken together, we expect no further ECB hikes in 2026 and lean toward a longer duration view in the Eurozone.

The Fed: All bark, no bite

On June 17, the Fed held the federal funds rate unchanged between 3.50% and 3.75% for a fourth consecutive meeting, a unanimous decision with no dissents. The rate decision itself was a sideshow. The meeting was Kevin Warsh's debut as Fed chair, and he used it to reshape how the Fed communicates.

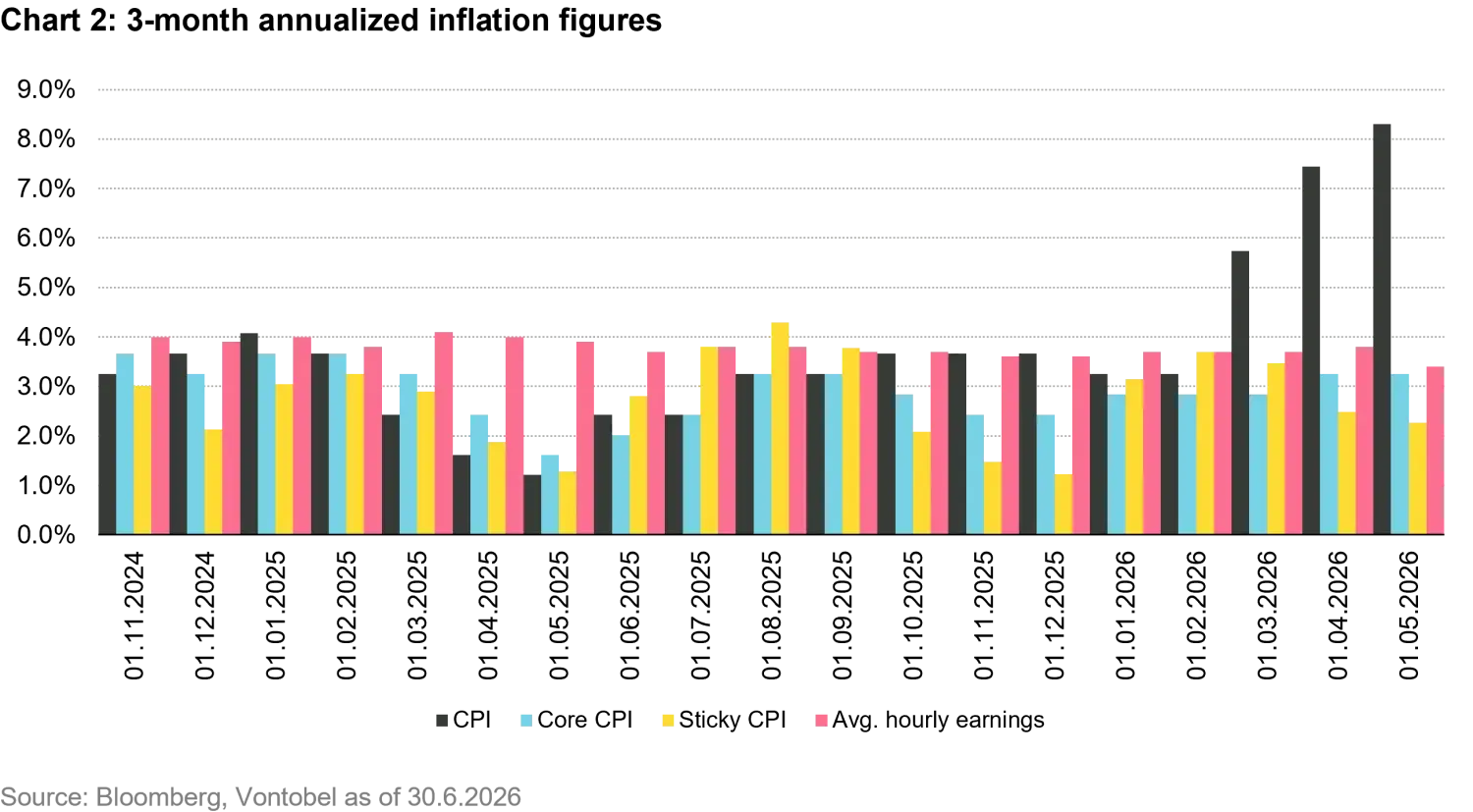

Forward guidance was dropped entirely, the statement was pared back to a simple commitment to restoring 2% inflation, and five task forces were established to study various aspects of policy. In place of guidance, the message was carried by the dot plot, and it was unambiguously hawkish. The median projection for end-2026 rates rose to roughly 3.8% from 3.4% in March. Nine of the members who submitted dots expected at least one hike this year, while six anticipated two or more, and the projection for 2026 core inflation lifted to 3.3%.

Markets took the cue. Front-end Treasury yields moved higher and overnight index swaps (OIS) began pricing in a full rate hike by October. On the surface, with inflation at its highest level in three years, a lot points to tighter policy.

We don't buy it. Our base case is that there will be no rate hike this year and that the Fed's next move, when it comes, will be a cut rather than a hike, most likely in 2027.

There are two reasons for this view. First, the inflation reflected in the dot plot is largely the result of a supply-side shock that is already reversing. The spike stemmed from the closure of the Strait of Hormuz. Now that the US and Iran agreement has been signed and oil prices have fallen by some 40% to their lowest level in three months, the energy pulse should soon drop out of the annual comparisons, rather than compound. Warsh himself downplayed the conflict's inflationary impact and conceded that members of the FOMC remain divided on whether the shock argues for higher or lower rates. Tightening policy into a fading supply shock is exactly the error a data dependent Fed should want to avoid.

Second, and perhaps more importantly, is the political backdrop. Warsh was appointed by President Donald Trump, whose administration has left no doubt that it favors an easier policy stance. Delivering a hike in an election year, contrary to the President's stated wishes, by the chair he just installed, is an extraordinarily high bar.

With midterm elections in November, we believe the path of least resistance is for the Fed to remain on hold and, once falling oil prices and softer growth provide sufficient cover, to begin easing. We therefore view the hawkish dot plot as a credibility signal rather than a plan that the Committee will execute. Plenty of bark, little likelihood of bite.

This view places us below market pricing, which implies a hike by October and a possible additional hike in 2027. We don't dispute the textbook case, since inflation is high and the economy robust; we simply judge that a supply-driven shock and election-year politics will override it.

The implication for portfolios is a steeper yield curve. At the front end, we continue to fade the hawkish repricing and stay long duration, with two-year Treasury yields at their highest in a year looking stretched, the dots appear to be overstating the likelihood of rate hikes, and summer technicals supportive into the autumn. The long end is another matter. If the Fed remains on hold while growth and inflation stay robust, longer-dated maturities could reprice higher, so we maintain a cautious stance there.

The BoJ: He who hesitates is lost

As both we and the market expected, the Bank of Japan raised its policy rate by 25 basis points to 1.0%, its highest level since 1995 and another step in the gradual normalization of monetary policy. The decision passed by a vote of seven to one, with newly appointed board member Toichiro Asada dissenting. The BoJ continues to describe its stance as accommodative. With underlying inflation approaching the 2% target and financial conditions still supportive, overall policy remains expansionary.

That said, Japan’s inflation dynamics warrant closer scrutiny. Measured headline inflation is actually low at around 1.4%, held down by government measures such as the removal of the gasoline tax and free high school education. Strip out those temporary factors, however, and the picture looks very different. Wholesale inflation hit a three-year high of 6.3% in May as firms passed through higher energy costs. That gap is precisely why the BoJ frames its target in terms of underlying inflation, and why, in our view, it cannot afford to wait.

We continue to believe that the additional hike we have long anticipated, to 1.25%, will arrive by December at the latest. However, this might not be enough. While the BoJ acknowledges the need for further policy normalization, there are growing signs that it may move more cautiously than what the macroeconomic backdrop warrants.

Asada represents the reflationist camp and reflects Prime Minister Sanae Takaichi's preference for running the economy hot through proactive fiscal and monetary stimulus. Balancing that political pull toward only gradual normalization against rising inflation risks and a weak yen, we see a risk that the BoJ falls further behind the curve.

The bond market already appears to be making that point for the BoJ as investors have pushed the 10-year Japanese government bond (JGB) yield to around 2.8%, near its 30-year high, effectively tightening on the central bank's behalf. As a result, long-term rates may rise more sharply than we had previously anticipated.

Alongside the rate increase, the BoJ announced that it will suspend the gradual reduction of its JGB purchases from April 2027 onward. However, because the maturities of JGBs already held on its balance sheet will continue to exceed its ongoing purchases, the supply reaching the market should still rise, adding further upward pressure on long-term JPY rates. We therefore remain short duration on JGBs, but have started to reduce our underweight position, given the attractive hedged and roll-down yields.