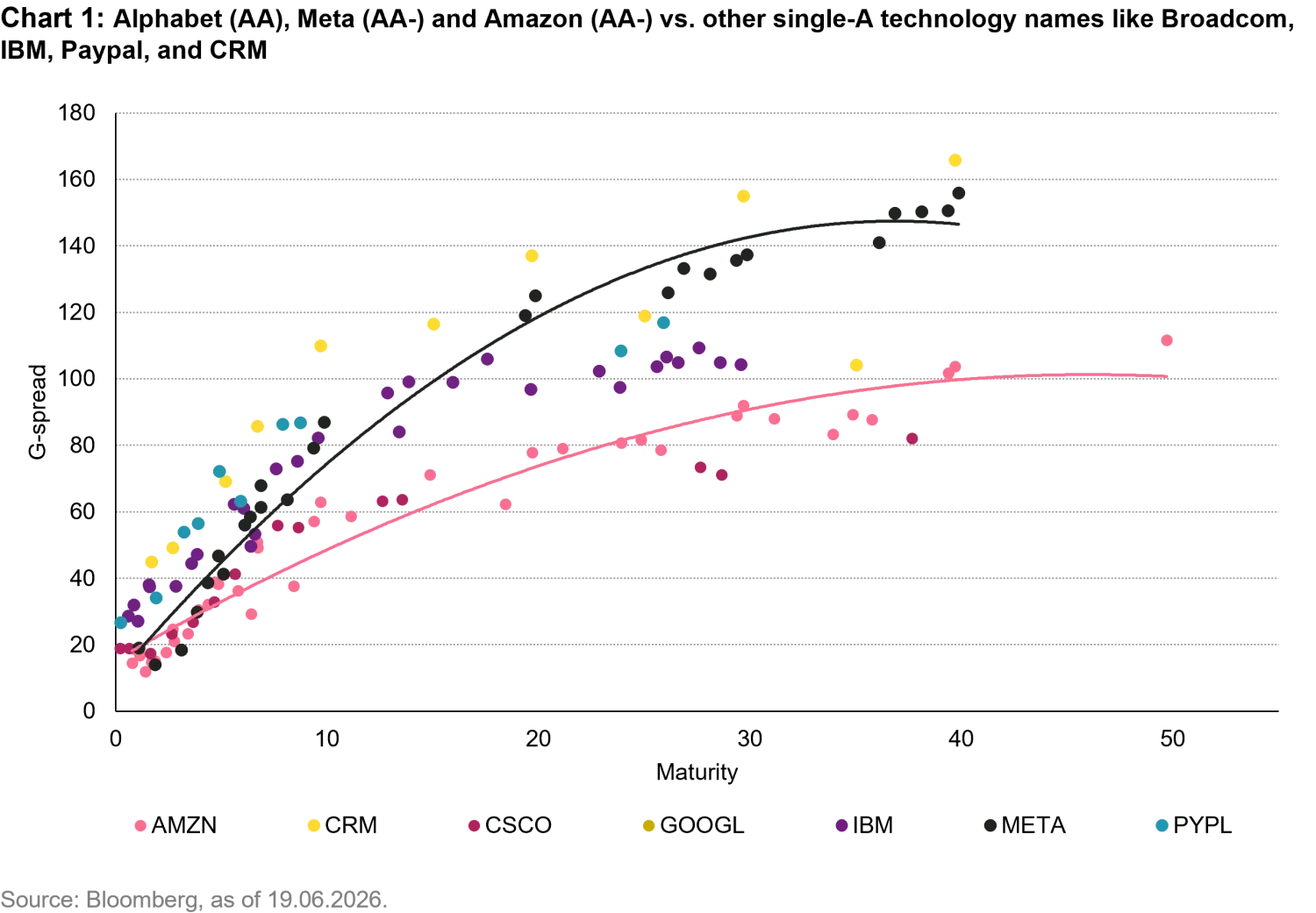

Hyperscalers reshape IG credit markets: AI capex boom shifts focus to security selection

Hyperscalers operate data centers and cloud infrastructure at massive scale. In the investment grade (IG) market, this group is largely limited to five well-known companies: Amazon, Microsoft, Meta, Alphabet, and Oracle. For most of the past decade, these companies ranked among the highest-quality non-financial IG issuers: characterized by net-cash balance sheets, low leverage, capital expenditure (capex) covered by internal cash flow, and accordingly very tight credit spreads.

That has changed. The scale of capital required to build out AI now exceeds what even these businesses can self-fund. In 2025, the five issuers collectively raised just under USD 100 billion in the global IG bond markets. And 2026 supply is projected to reach USD 250-300 billion globally to fund a combined capex of USD 800 billion1, of which EUR 50 - EUR 100 billion is expected to be issued in the EUR IG market. Such volumes are putting investors on the backfoot, raising questions about the implications of credit both on technicals and fundamentals.

The benchmark impact is visible: From the beginning of the year through mid-June 2026, the combined weight of hyperscalers in the ICE BofA Global Corporate Index has increased by approximately 50%, rising from around 1.9% to 2.8%. New issue premiums have widened relative to typical IG deals, with typically low-double-digit basis points (bps) pick-up to secondary curves, as investors demand a concession for the volume offered.

Despite the credit-negative aspect of such elevated issuance and capex, we believe these issuers offer interesting mitigants:

First, the sector entered this cycle with exceptionally strong ratings, ranging between AAA and AA- (with Oracle being the exception at mid-BBB with a negative outlook). That quality is itself being actively defended: the flip side of needing so much debt is that these issuers have every incentive to protect their ratings and keep interest costs down. Hence the recent credit-positive actions to issue fresh equity: Alphabet's approximately USD 85 billion equity raise and Oracle's announced USD 25 billion equity issuance are appreciable credit-friendly attitudes. But not every issuer is equally proactive: Meta has been less vocal in defending its rating trajectory, underscoring the importance of security selection rather than treating the group as a bloc.

Second, issuers have found creative ways to curb cash needs. "Bring-your-own-chip" arrangements and installment-based payment models for servers have been built, helping to shift the heaviest cost upstream to the customer instead of the hyperscaler.

Third, several of these businesses benefit from highly diversified core operations, such as Amazon's retail engine and Alphabet's and Meta's core advertising franchises, which provides a cash-generative buffer to support the AI side of the business.

Fourth, the development of in-house chips (e.g., Google's TPU, Amazon's Trainium, etc…) offer an alternative to Nvidia's GPUs while vertically integrating the supply chain. Not all of them can do this, and the chips are not yet as efficient as Nvidia's, but with demand this strong the strategy has so far paid off. Although not a near-term cash saver, this strategy could support improved cost efficiency over the longer term.

Finally, investors are gradually adapting to jumbo supply. The surprise effect is fading as investors progressively find the fair value of this new debt. Hyperscalers already trade at levels comparable to issuers rated two-to-three-notches-lower, meaning that much of the harmful repricing has already taken place.

These names will therefore likely remain in the IG investor landscape for a while as their weight in the indices has grown over the years. So, we believe it is paramount for investors to understand and embrace this significant new segment of the corporate bond market.

Optimizing returns through the bond lifecycle

While structural themes such as hyperscaler investment continue to shape the long-term opportunity set in credit markets, portfolio returns are ultimately determined by thousands of smaller allocation decisions. In a market where yields remain attractive but spread dispersion is limited, extracting value increasingly depends on understanding the relative return drivers embedded within individual securities.

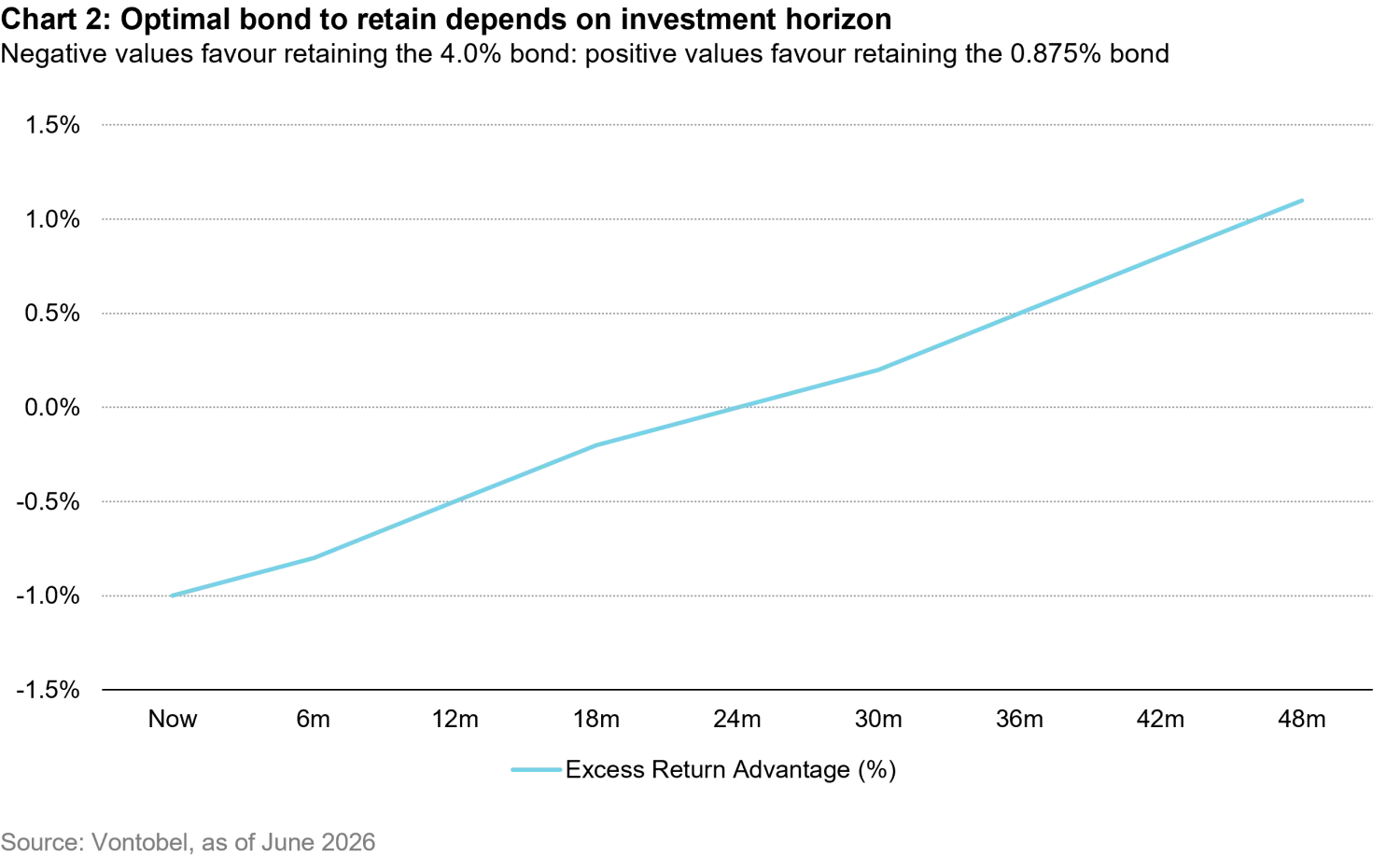

Consider two bonds issued by Enel Finance International. Both are senior unsecured, euro-denominated bonds with almost identical maturities in 2031. The key difference lies in their coupon structures. One bond carries a low coupon of 0.875% and trades well below par, while the other offers a 4.0% coupon and trades slightly above par.

At first glance, the two securities appear remarkably similar. Their yields to maturity are nearly identical, implying that the market views them as broadly equivalent from a valuation perspective. However, the path through which investors earn that return differs substantially.

A useful framework is to decompose expected bond returns into their main building blocks:

Expected Return = Carry + Roll-down + Pull-to-Par

Carry represents the coupon income earned while holding the bond. Roll-down captures the price appreciation generated as a bond moves down a normally upward-sloping yield curve. Pull-to-par reflects the tendency of bond prices to converge towards their redemption value at maturity.

The higher-coupon bond generates most of its return through carry. Investors receive a meaningful coupon stream while holding the security, making it particularly attractive over shorter investment horizons. The lower-coupon bond, by contrast, offers limited income but benefits from a stronger pull-to-par effect, as its price gradually converges towards par.

This distinction creates an interesting optimization problem. Suppose a portfolio holds both bonds in equal proportions and may need to raise liquidity at an uncertain future date. Which bond should be sold?

Under a simplified framework, the answer is relatively straightforward. Assuming an unchanged yield-curve shape, unchanged credit spreads, pull-to-par evolving as expected and roll-down occurring along today's curve, carry dominates expected returns over shorter horizons. In this environment, the higher-coupon bond is generally preferable to retain, while the lower-coupon bond becomes the natural source of liquidity.

As the investment horizon extends, however, the balance gradually shifts. The low-coupon bond increasingly benefits from capital appreciation as its discount to par narrows. At the same time, its slightly longer duration provides greater exposure to roll-down effects. Eventually, these factors offset the carry advantage of the higher-coupon bond. The optimal source of liquidity is therefore not static but depends on the anticipated holding period.

In this example, the crossover occurs roughly halfway through the remaining life of the bonds. During the first half, the higher-coupon bond is generally preferable to retain, while in the second half the discounted bond becomes increasingly attractive as pull-to-par and roll-down effects dominate the return profile.

Importantly, market expectations matter. The previous framework implicitly assumes a stable rates environment. If investors instead expect a bull-steepening of the euro yield curve, the balance shifts earlier towards the lower-coupon bond. Its higher duration and stronger pull-to-par profile allow it to capture a larger share of the capital gains associated with falling yields. In such a scenario, retaining the lower-coupon bond may become preferable even at relatively short horizons.

High yield

Global high yield: surface calm, deep dispersion

The global high yield (HY) market enters the second half of the year on a dual track, where headline index stability contrasts sharply with deeper structural fragmentation beneath the surface. For the most part, public credit markets have effectively looked through recent Middle East frictions. Indeed, US high yield spreads have tightened by 50 bps since the conflict started, while European spreads compressed by 24 bps, allowing both markets to trade comfortably below pre-conflict levels.

This baseline stability is particularly evident in the US primary market, where gross supply is currently running 30% ahead of last year's pace. This primary strength is fundamentally driven by elevated all-in yields that continue to attract substantial institutional inflows, alongside a powerful structural capex cycle driven by investment in technology infrastructure and data center operators, which alone accounts for roughly 20% of US HY tech gross supply year-to-date.

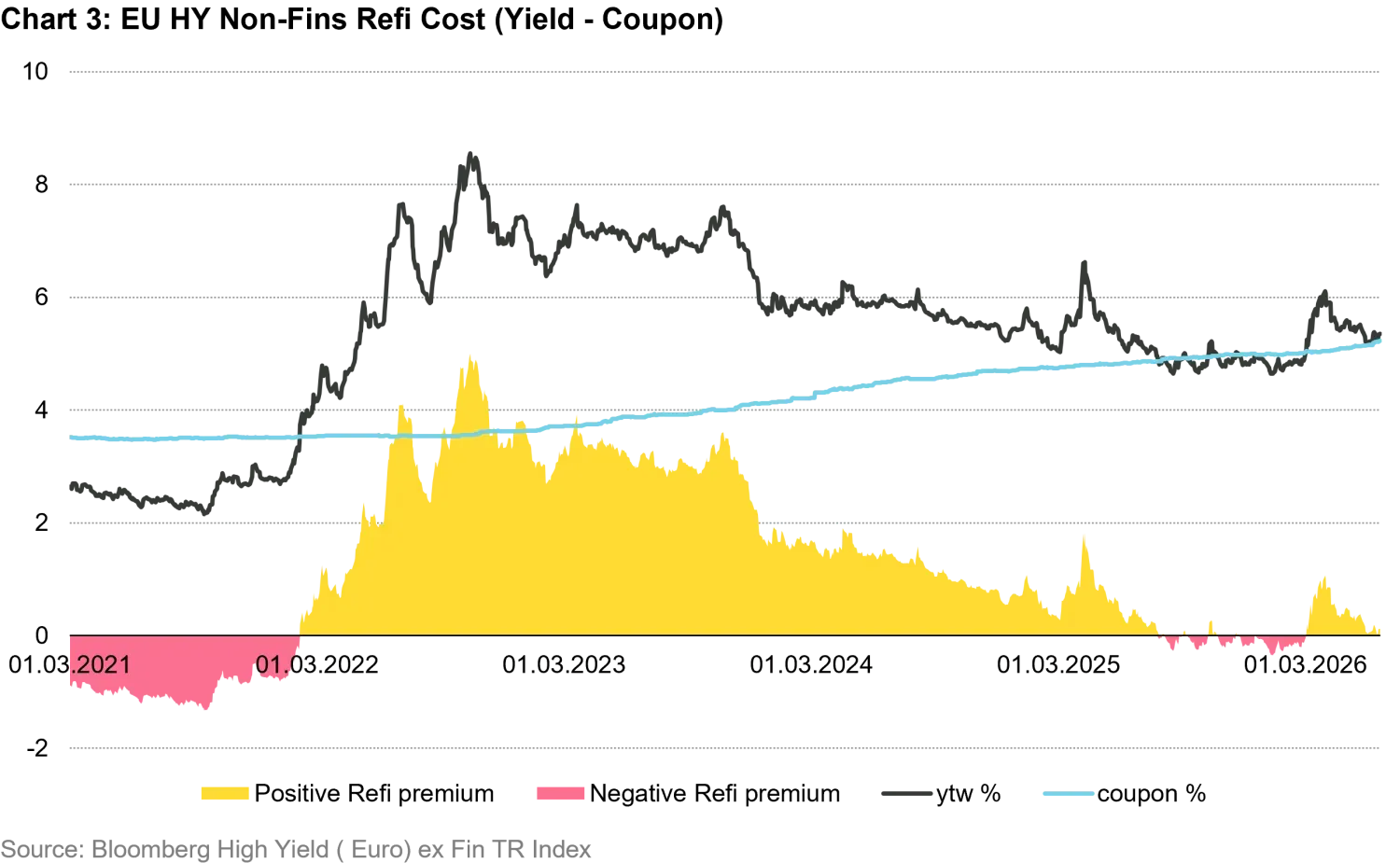

Concurrently, the European primary market is on track for another record year, with net supply up 40% year-on-year at the end of June. This issuance pattern represents a fundamental structural shift: sustained high interest rates are pushing issuers away from leveraged loans and toward public fixed-rate bonds as a way to lock in coupons and eliminate floating-rate volatility. As shown in Chart 3, this pivot is further accelerated by a steadily diminishing refinancing cost. Because the gap between current market yields and outstanding coupons has narrowed, the hurdle of a refinancing shock has largely disappeared.

Driven by this dynamic, European corporates are accelerating liability management exercises (LMEs) to opportunistically address their maturity walls early, rather than delaying execution. Ultimately, this heavy supply has been easily absorbed by deep institutional cash balances, providing a powerful technical anchor for the entire asset class.

Yet, this strong primary demand masks an environment where credit-by-credit dispersion remains near historical highs. This is particularly clear in the technology sector. While infrastructure investment continues to drive primary volumes, the broader integration of artificial intelligence is simultaneously emerging as a main source of long-term concern for legacy business models in the secondary market.

This secular trend is causing a sharp internal bifurcation, with legacy software and IT services companies facing increasing margin pressure as they struggle to adapt to rapid technological evolution. Crucially, this disruption risk is increasingly migrating into the opaque private credit channel, where vulnerable legacy issuers are relying heavily on direct lending funds, effectively masking fundamental deterioration and leverage strains with a significant time lag relative to public markets.

Outside of technology, polarization is equally pronounced. The energy sector remains a clear global outperformer across both US and European markets, with spreads tightening by 150 bps since the geopolitical shocks began. Far from being a short-term story, this transatlantic outperformance is rooted in years of organic deleveraging and fortress balance sheets, which have translated into solid total returns of +4.2% in the US and +4.1% in Europe. Conversely, European manufacturing is facing a conventional, macro-driven economic slowdown, experiencing severe margin compression driven by sticky input costs and weak domestic demand.

Looking ahead, while the Iran conflict has not triggered systemic macroeconomic disruptions in Europe, the upcoming Q2 earnings season will likely reveal visible margin pressures. This fundamental friction could drive a moderate spread widening in the near term. However, we view this potential soft patch as a tactical window to gradually rebuild exposure to high-conviction names that are currently trading at excessively tight levels.

Our portfolio strategy remains firmly anchored in a strong relative value preference for high-quality single-B credits over BBs, as the latter appear too compressed to compensate for cyclical and duration risks, in our view. As we move into Q3, execution will depend on highly rigorous credit selection, meaning we will strictly avoid structurally deteriorating credits, regardless of transient geopolitical impacts, and heavily penalize companies that fail to demonstrate robust, organic cash generation.

Swiss bonds

“The final countdown": attractive yields before the summer supply drought

The past few months have been dominated by geopolitical headlines, shifting policy expectations and elevated market volatility. Yet beneath the noise, the picture for Swiss fixed income remains relatively straightforward.

Swiss inflation has continued to surprise on the downside, allowing the Swiss National Bank (SNB) to remain patient despite global uncertainty. While markets briefly priced in renewed tightening risks amid concerns over energy prices and geopolitical tensions, these expectations have largely faded. We see little reason for the SNB to adopt a more hawkish stance and continue to expect a supportive interest rate backdrop. For investors, this leaves CHF bond yields at attractive levels. While all-in yields remain elevated relative to recent years, we believe the direction of travel is lower.

Credit valuations are admittedly tight, but tight valuations alone rarely trigger spread widening. More importantly, we see few catalysts that could materially weaken the market. Investor demand remains healthy, fundamentals are stable, and lower government bond yields are poised to continue to support the asset class.

The primary market has remained highly active, with total issuance volume exceeding CHF 11.8 billion year-to-date. Several debut issuers tapped the Swiss franc bond market for their inaugural transactions. Despite this substantial net supply, new issues have been very well absorbed by investors without requiring higher credit spreads. As a result, credit spreads remained broadly stable over the reporting period.

Seasonality could provide an additional tailwind. As summer approaches, primary market activity is expected to slow significantly. The combination of limited new supply, healthy cash balances, and investors looking to lock in attractive yields has historically created a supportive environment for CHF bonds.

The setup for the coming weeks appears constructive. While headline risks remain ever-present, the combination of subdued inflation, a patient SNB, supportive technicals, and an approaching summer issuance drought is poised to create a favorable environment for CHF bonds.

Investors waiting for significantly wider spreads may find themselves disappointed. Instead, we believe the more likely scenario is one of gradually compressing yields and steady carry-driven returns.

In other words, the final countdown may have already begun. Investors may therefore wish to review portfolio exposure sooner rather than later, enjoy the summer, and when you return from the beach, the market may have already delivered the performance you were waiting for.

1. Source: Morgan Stanley

Investing involves risk, including possible loss of principal. Any projections, forecasts or estimates contained herein are based on a variety of estimates and assumptions. Market expectations and forward-looking statements are opinion, they are not guaranteed and are subject to change.