Key takeaways

- Recent inflation data, coupled with the measured stance of central banks, implies that market rates may be too high

- Diversification and downside protection remain valuable, but we expect credit spreads to tighten given very strong technicals

- The challenges facing private credit are not over and should not be ignored

- Credit fundamentals, particularly in investment grade, remain very strong

- Equity valuations are entering greed territory. As such, a risk-off event cannot be discounted. This may be a good opportunity to add risk.

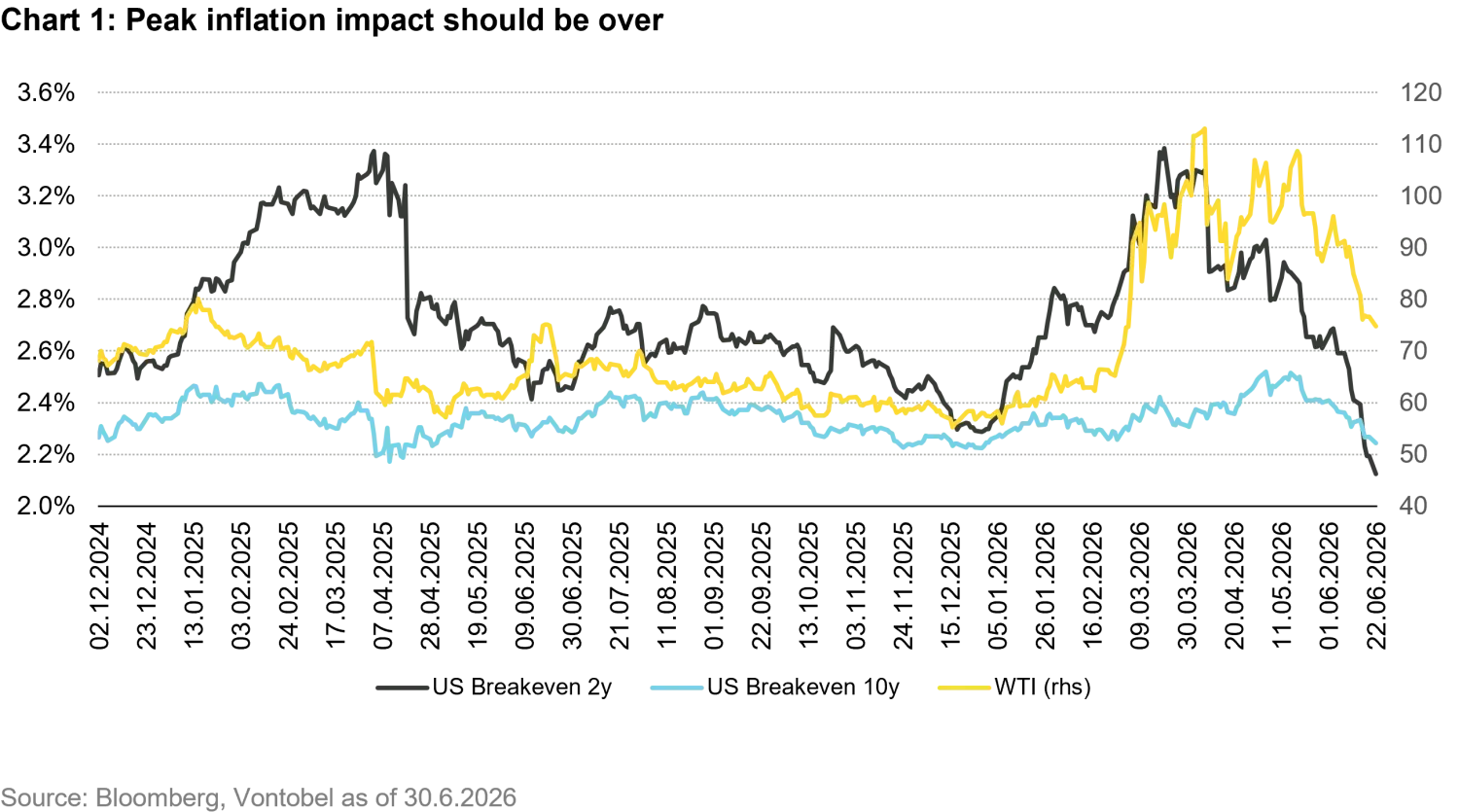

The re-opening of the Strait of Hormuz is undoubtedly a positive development, as it reduces the probability of longer term, pernicious inflation. That said, the degree to which inflation risk is already reflected in asset prices is a key area of analysis and is likely to remain a focus for markets, particularly Fixed Income markets, for the foreseeable future.

I believe it would be unwise to suggest that any further geopolitical escalation would challenge markets, given how incredibly sanguine investors have been to date. Even so, I am surprised by how market participants are so unconcerned by the lack of predictability of the current US administration.

Putting that significant market-moving consideration aside for a moment, Fixed Income markets look remarkably attractive given current credit spread levels. Credit spreads are tight and, particularly within higher-risk sub-asset classes, there is less upside from here than one would require to justify an extremely bullish stance. However, I do expect credit spreads to tighten over the summer.

Clearly, there are risks to that view. Spreads could widen materially and rapidly, particularly given how widely held that view has become, but I still believe it’s an accurate reflection of the forces currently shaping markets. The lack of a “short squeeze” following the announcement of an agreement to end the conflict in Iran supports this view, as do credit fundamentals, Fixed Income market technicals, and the broader economic backdrop. Notably, markets are feeling rather bearish on the path of interest rates. Hence, we feel modestly positive on the markets, while favoring higher-rated areas and those that offer diversification benefits. Our portfolio management approach remains very active, and turnover continues to be high.

One major note of caution is the complacency we are seeing around private credit. The consensus view (in this instance, a nearly universal one) is that conditions are probably fine: underlying credits are in better shape than the market perceives, and once all of the current challenges are worked through, conditions should return to “normal.”

That strikes me as hugely complacent. I have seen asset classes impose gates and subsequently recover; indeed, that is generally the path taken. However, there is clearly a small risk that this does not happen. If it doesn’t, the consequences could be far more severe than a handful of gated funds.

The path to an adverse event and contagion could look like this:

- A gated fund receives a request for an extension, refinancing, or a top-up.

- The fund has to decline the request because it is focused on managing existing problem loans.

- The borrower turns to another lender, who offers to provide financing, but at much higher rates.

- The cycle repeats.

Potential consequences are:

- The loan market reprices.

- Interest coverage ratios worsen.

- A small number of loans move toward restructuring.

- A material increase in the probability of steps one through four recurring.

- More funds impose gates and apply discounts.

I have seen this occur previously, even with fundamentally sound borrowers in the loan market. While it is rare, I am surprised by the arrogance and complacency of managers who launched funds with liquidity terms they are now describing as “normal,” when they were clearly inappropriate in my view. At a conference I recently attended, I sat through several private credit sessions. Not a single manager or sponsor expressed any real contrition regarding the gating of their BDCs. Sometimes our industry does not help itself.

For that reason, among many others, we continue to encourage investors to increase their allocations to active Fixed Income strategies. We believe that the alpha generated by our active approach over the past few years will continue to crystalize in the years ahead.

There is considerable value in being flexible in today’s markets. But when we talk about flexibility, we do not mean taking more risk. In fact, several of our strategies have used their flexibility this year to take less risk than usual. As a result, we find ourselves leaning more heavily into interest rate duration risk of Fixed Income and less into credit spreads.

Recent inflation data, the gradual reopening of the Strait of Hormuz, and the moderate and temperate language and actions of developed market central banks have given us some comfort around rate risk. We will continue to monitor these parameters closely.

Meanwhile, politics in the United Kingdom remain chaotic. Just a couple of years after winning a landslide victory for his Labour party, Sir Keir Starmer has been forced to stand down by members of his own party. It now appears almost certain that Andy Burnham, the former Mayor of Manchester, will become the next prime minister. Political uncertainty will not be reducing, and it is possible that markets, particularly the gilts market, will have plenty to worry about.

With Germany already out of the World Cup and Switzerland and England still in, maybe the market will be distracted and calm over the summer… somehow, I doubt it!