mtx Equities

Seeking to invest in leading businesses with high and growing profitability, leading industry positioning and strong sustainability characteristics in emerging markets, Asia and China.

In many investors’ minds, emerging markets remain strongly associated with cyclical economies, entirely dependent on the dynamism of international trade and especially on demand from developed-country consumers. Many still consider them as greatly vulnerable to political and geopolitical risks, as well as to rapid US dollar (USD) appreciation and destabilizing capital outflows in times of crisis. More fundamentally, emerging markets remain too often associated with a global economy of “tangibles” (commodities, natural resources, low-value manufacturing goods) at a time when intangibles (AI model training and inference) are resetting the world.

Based on such a perception, there are two scenarios under which emerging markets as a whole should have, if not collapsed, at least dramatically underperformed:

These are exactly the two shocks that global markets experienced over the last twelve months. Yet far from collapsing, MSCI Emerging Markets index over that period has delivered the most persistent and sizeable outperformance registered in more than 18 years.

How to explain such a gap between those developments and the expectations inherited from legacy perceptions? Since early 2025, we have been vocal about the fact that many emerging markets underwent a fundamental transformation over the past decade: their fiscal positions became sounder, their monetary frameworks more credible, their corporate governance improved and, ultimately, their reliance on domestic demand and on trade with other partners within emerging markets grew, while they took key leadership in many of the winning themes of increasingly bifurcated economies. We concluded that this transformation cemented the source of their recent resilience and the way they weathered the recent shocks that would have proved extremely destabilizing in the past.

We believe it is now high time for investors to fully accept this new reality and incorporate it into their allocation, at the risk of missing further opportunities.

Watch the replay of our webinar “EM equities: from lost decade to essential diversifier?” to explore the key forces influencing emerging markets today — and what these developments could mean for investors.

Today’s emerging markets have achieved a level of structural resilience that was unimaginable a decade ago. Through the Liberation Day tariff shock of 2025 and now a nine-week Middle East conflict, the MSCI Emerging Markets index has accumulated an outperformance over the MSCI World index, now close to 15%. In emerging market fixed income, local currency (valued in USD) has outperformed Global Aggregate (USD hedged) by over 11.5% since Liberation Day, whilst emerging market hard-currency sovereigns have added 9.5% over and above the Global Aggregate. More importantly, those markets – yesterday prone to rapid destabilization during each severe global crisis – have demonstrated remarkable stability, with no dramatic capital outflows or local currencies’ free fall, in fact quite the contrary. Even when the USD was re-appreciating somewhat at the start of the conflict with Iran and expectations about interest rate cuts by the US central bank were reversing rapidly, outflows remained modest in volume.

On multiple occasions1 over the last 15 months, we have communicated about the structural drivers behind this renewed source of resilience. We can only repeat and summarize them here: stronger fiscal and foreign exchange (FX) reserve positions, more credible monetary policy frameworks, deeper and – at the margin – better functioning domestic capital markets with sizable local investors have somewhat reduced dependence on fickle foreign flows.

On the sovereign and institutional level, internal vulnerabilities in emerging markets have been reduced through the implementation of sounder fiscal policies, more credible monetary frameworks coming from independent central banks, including free floating currencies, and inflation targeting in many countries. This disinflation trend in emerging markets has been notable to such a point that aggregated inflation levels in the main emerging economies are now on par with inflation in the developed world, down from much higher levels in the past. China/Asia has been a significant contributor to the recent deflationary pulse in emerging markets. Besides, proactive institutional reforms and – sometimes – painful austerity measures have been employed, and not just in Argentina, to address structural imbalances, which were plain to see during the Covid pandemics and the 2022 cost of living crisis. Such measures have frequently been shunned in many developed markets, perceived as being too politically unpalatable, leading to the perception of a narrowing risk between emerging and developed markets (see below).

External vulnerabilities have also, on aggregate, decompressed indirectly through the development of local financial markets, which has reduced dependency on USD denominated debt (less sensitivity to “the original sin”), whilst fostering a network of domestic real money investors (banks, pension funds, insurers) to offer a local bid for emerging assets. This mechanism has facilitated the recent notable trend of FX reserve accumulation, reducing external vulnerabilities, through injecting the local currency into the market to buy USD (or gold), enhancing liquidity in the local market, and providing demand for local currency bonds. In turn, reducing the “original sin” risk.

As important has been the reorientation of trade. Flows within emerging markets have grown substantially, with China, India, and the members of the Association of Southeast Asian Nations (ASEAN) increasingly trading with one another, rather than serving exclusively as manufacturing hubs for Western consumption. Trade between emerging markets, regional supply chains, and — above all — the rise of domestic consumption have reduced the correlation between emerging economies’ growth and Western business cycles. We believe that when developed-market demand softens, emerging markets now should have alternative engines to sustain momentum.

This shift is underpinned by a profound demographic and income transition. The emerging-market middle class has grown to rival developed economies in both size and sophistication. In China, emotion-driven consumption is reshaping entire sectors, as consumers prioritize experiences and identity expression. In Brazil and Mexico, domestic-focused companies are benefiting from easing cycles and stable consumer demand, even as external conditions fluctuate and sometimes deteriorate. This consumption base provides a natural buffer against external shocks and has materially reduced the export dependency that once made the universe so vulnerable.

Markets have begun to recognize this. Emerging-market equities’ volatility has declined meaningfully relative to historical norms, while the ex-ante risk premium required to hold emerging equities has declined – sometimes substantially in 2025 – through the rise of valuation multiples. Coincidentally, this overall reassessment of emerging markets’ risk has collided with an erosion of the perceived US exceptionalism, at least the strengths of some of its institutional pillars. This combination made emerging assets - both equities and debt – much stronger candidates to diversify portfolios still mainly concentrated in US assets.

A similar dynamic has taken place on the emerging-market debt side. Both sovereign and corporate bond spreads for example, typically a measure of relative default risk, have notably compressed. While this compression partially results from improved fundamentals of the bulk of emerging-market issuers, with the strongest in a decade upward average re-rating experienced since the downgrade nadir of 2022, it also reflects the increasingly elevated term premium requested by fixed-income investors to hold long-term US treasuries.

Emerging markets have never truly behaved like a single block. However, now that their traditional common vulnerabilities have been fading, the idiosyncrasies in their specific dynamics appear more explicitly.

China obviously deserves its own distinct narrative. It is still struggling with strong deflationary forces, even if some very preliminary green shoots in early 2026 may suggest some relief – at least temporarily. The government’s “anti-involution” policies — designed to curb overcapacity and excessive price competition — may progressively help stabilizing margins and profitability in upstream sectors, while rising energy costs will still put additional pressures on downstream sectors. At the same time, consumption is tracking its own K-shape recovery: while overall consumer sentiment remains sluggish, premium consumption, such as luxury goods and Macau gaming, is showing double-digit growth. The rise in experience-oriented and emotion-driven consumption, like travel or outdoor activities, is also outpacing significantly.

India was reaching more compelling valuation levels when hit by the rise in energy prices that could put earnings growth at risk in the second half of 2026. Ahead of the crisis, earnings of companies represented in India’s leading equity index (NIFTY) were projected to accelerate sharply in fiscal year 2027, with consensus expecting a potential +15.5% year-over-year, which would position India as the fifth fastest-growing market globally.

Latin America: the great rotation gains momentum. The MSCI EM Latin America index is currently the best-performing regional index year-to-date, up 18%, with Brazil possibly offering up to 27% upside for foreign investors, according to our estimates. Brazil stands out on two counts: it is set for a significant easing cycle, which has begun in March 2026, and it benefits as an energy exporter in a world of higher commodity price floors. Mexico, meanwhile, is showing resilience to election uncertainty, benefiting from USMCA (United States – Mexico – Canada Agreement) renegotiation catalysts and lower interest rates, with nearshoring beneficiaries particularly favored. Political cycles introduce meaningful dispersion: upcoming elections in Brazil, Colombia, and Peru will determine whether the rotation might be sustained or partially reversed.

Beyond local specificities, emerging markets do not escape the forces resulting from increasingly bifurcated economies. Like in developed markets, those forces are increasingly rewarding winners while penalizing losers. We define these winners as industry leaders with rising return on investment capital (ROIC). Currently, we find this type of business in the following three areas:

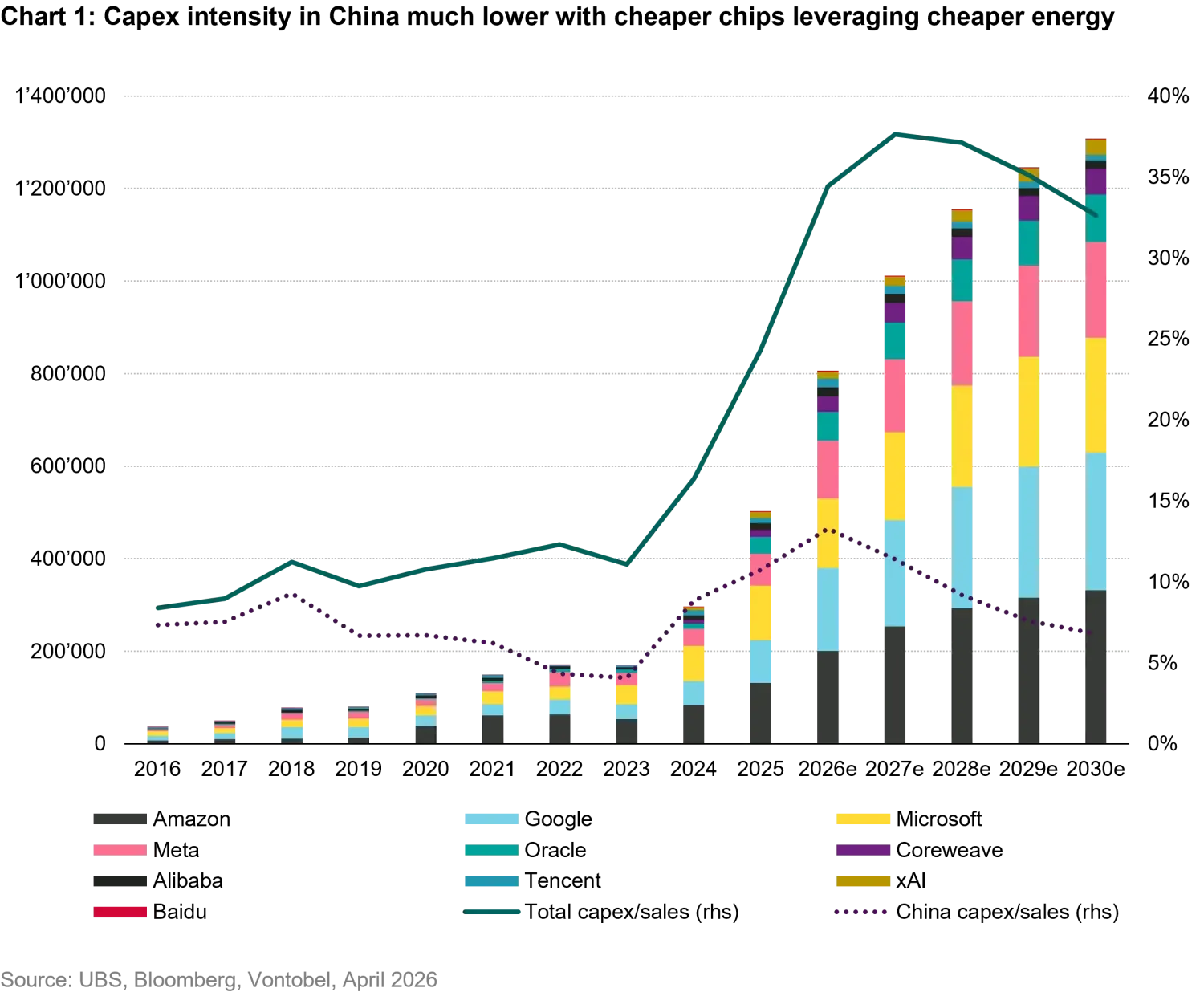

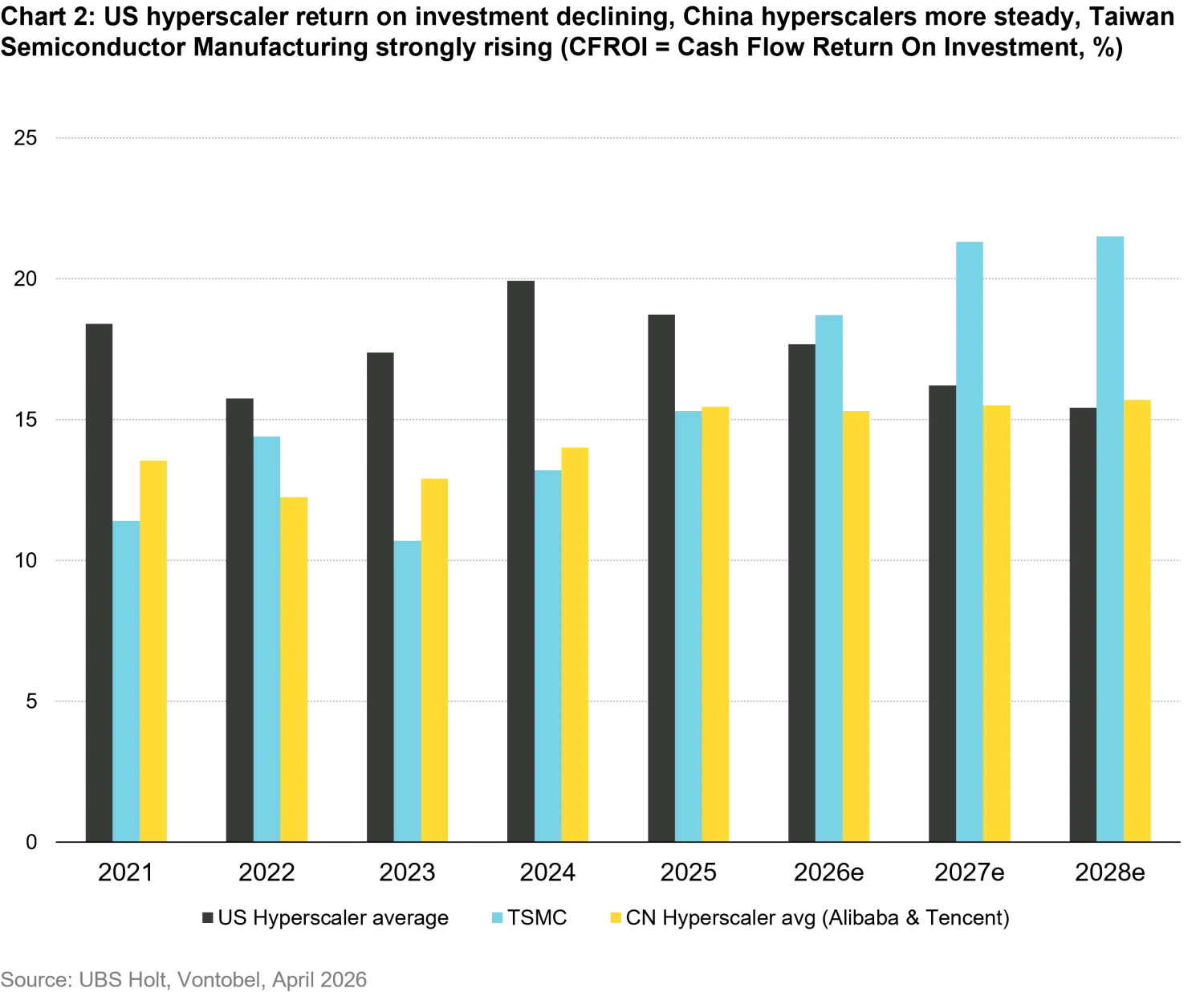

The first is obviously the supercycle of capital expenditure (capex) in artificial intelligence (AI). Hyperscalers’ capex is projected to grow over 60% in 2026 and to surpass USD 900 billion by 2027, creating sustained demand for advanced semiconductors and hardware and positioning Taiwan, South Korea, and to a lesser extent also China as the primary beneficiaries. While the former two are major winners of the ever-increased spending from US hyperscalers, China has been patiently building its own ecosystem, not as spectacular but more autonomous, while still supplying large segments of the AI-value chain equipment needs, both domestic and overseas.

The AI infrastructure boom is increasingly affecting not only the most advanced AI chips and high-end servers, but also more traditional processors and hardware needed for the execution of growing agentic AI applications. It is supporting not only semiconductor and server manufacturers, but an entire ecosystem of power infrastructure, grid equipment, and data center suppliers. And with the gap between AI compute demand and infrastructure supply still widening, many companies experience even accelerating earnings growth, as the deepening undersupply drives massive price hikes. Therefore, it is even more important to select industry leaders with pricing power and products with little substitutes. Memory makers or cutting-edge chip manufacturers, for instance, can pass on rising input costs, impose much higher selling prices, and lock in longer capacity commitments, as customers are desperately looking for supply.

The second is energy security, which has moved from a background topic to a front-and-center investment theme, supported by both AI exponential needs and national security concerns, naturally amplified since the beginning of the Middle East conflict. Among emerging markets, India, Thailand, and Taiwan are the most exposed to a Hormuz disruption, while China holds a unique buffer, as it has accumulated the largest oil reserves globally. Taiwan and Korea could afford to pay up for gas given record high prices for AI driven technology reports. China and India could also afford some substitution away from oil and gas in power generation towards coal-fired generation, even if coal-switching would probably take longer to be implemented.

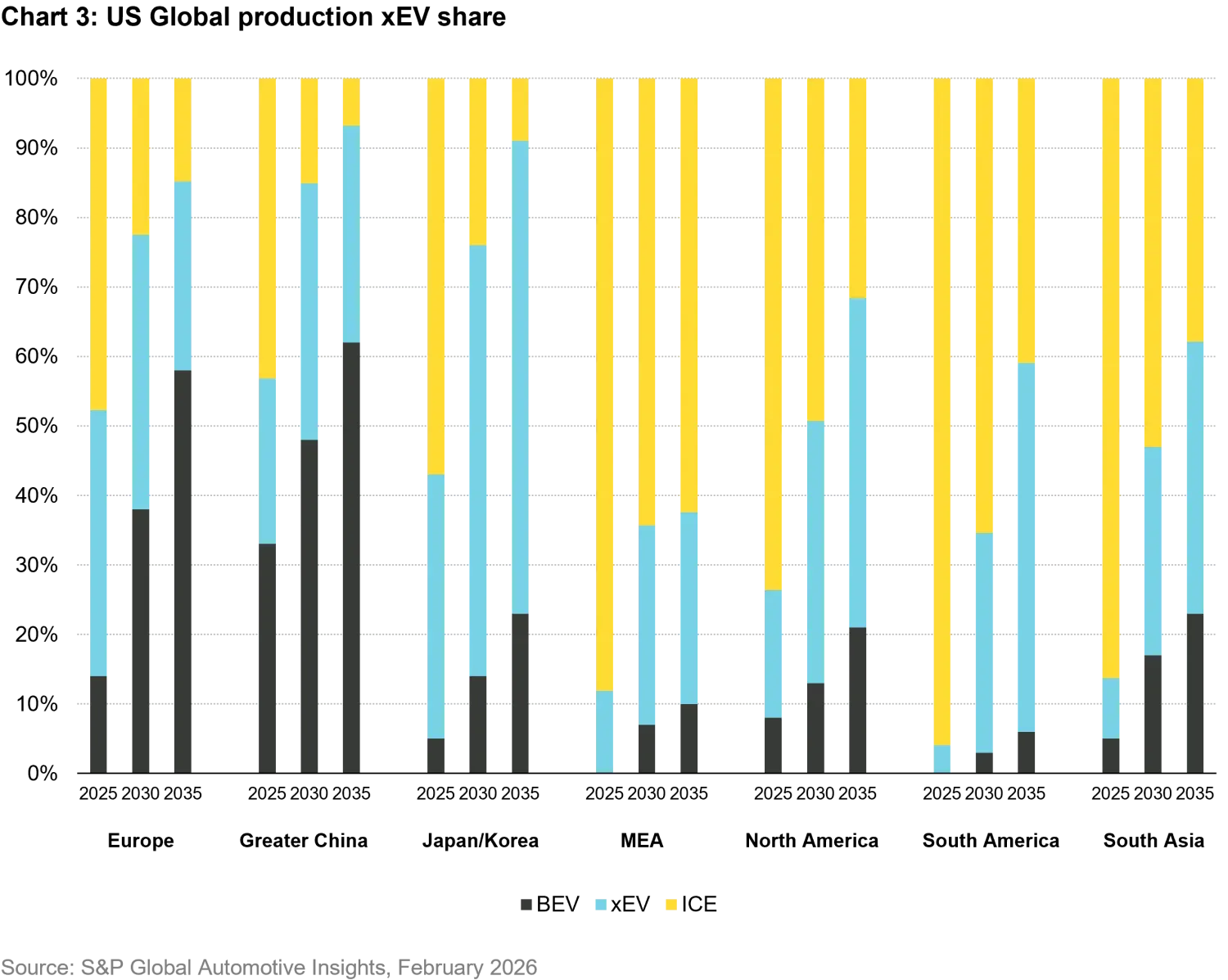

Beyond the current conflict, the post-Hormuz disruption world would likely look structurally different, not just cyclically tighter. First, the shock is likely to accelerate the push toward alternatives: higher and more volatile fossil fuel risk strengthens the investment case for electric vehicle (EV) adoption over internal combustion engine (ICE) vehicles, faster rollout of renewables, including battery storage systems, and renewed interest in nuclear power as a stable, geopolitically insulated baseload. This shift is inherently materials-intensive, boosting strategic importance and demand for copper, aluminum, lithium, and other critical minerals. In short, the focus is shifting from efficiency-optimized energy systems to robust, redundancy-driven ones, with lasting implications for prices, investments, and capital allocation. Many leading providers in the energy security space are based in emerging markets.

The third is a wave of corporate governance reforms gathering pace across multiple markets, with the potential to unlock substantial shareholder value. Five of the six major Southeast Asian economies are implementing meaningful improvements simultaneously, including Vietnam’s upgrade to emerging-market status, while Indonesia was forced to follow MSCI-suggested reforms. The track record elsewhere is compelling: reform programs in South Korea and China have been associated with indices trading on average 25% higher post- than pre-reforms. South Korea’s “value-up” program is particularly noteworthy, encouraging large, family-owned conglomerates, so-called chaebols, to concentrate resources on their most promising growth units while banning dual listings that previously diluted parent-company value. This is not simply a technical adjustment but should rather be seen as a fundamental shift in how emerging-market companies treat minority shareholders and allocate capital. Over the last decade, shareholders and earnings per share (EPS) have been diluted by the issue of new shares and convertible bonds, driving parts of the underperformance of emerging markets versus developed ones. Increased focus on corporate governance and shareholder return have already reverted this trend, and share buy-backs and dividends have been rising2.

Our positioning reflects both the conviction and the risk hierarchy described above, and currently translates in our emerging-market portfolios as follows:

Overweight Asian AI infrastructure enablers. Taiwan and Korea remain the most direct expressions of the AI capex cycle. Our highest conviction is in suppliers to hyperscalers, advanced packaging, and custom silicon, complemented by selective exposure to Southeast Asian data-center ecosystems in energy-secure markets.

Overweight Brazil. The combination of an easing monetary cycle, commodity-price tailwinds, and attractive valuations — Brazil trades as the second-cheapest major market globally, based on forward price-to-earnings (P/E) ratios — may create an asymmetric opportunity. Mexico complements this exposure through nearshoring beneficiaries.

Continued underweight India, albeit to a smaller extent than over the last two years. After a significant derating over recent quarters, Indian stocks look less expensive than in the past, but catalysts are missing to justify an aggressive repositioning, while the oversensitivity of the Indian economy to fossil fuel prices put both revenue growth and profitability of many Indian companies at risk in the second half of 2026.

Selective overweight in the EM industrial-capex complex. Suppliers of power equipment, grid technology, and data-center infrastructure — in India, China, and selected ASEAN markets — sit at the intersection of our strongest cross-regional themes. We favor names that we believe combine pricing power with long order backlogs.

Emerging markets have just passed two major stress tests — a trade-war shock and an energy shock that would have been devastating in the old framework. Their outperformance is not a paradox to be explained away; it is the confirmation of a transformation that has been in the making over the last decade. Domestic demand has replaced Western consumption as the primary growth engine. Trade among emerging economies has partially reduced USD-denominated dependency. Governance reform has begun to reduce the historical quality discount on the corporate side. And in the themes that define the next cycle — AI infrastructure, electrification, and energy sovereignty — emerging economies are no longer followers but global leaders in key segments.

The risk of under-allocation in emerging assets is now, in our view, significantly higher than the risk of over-allocation. Many investors missed last year’s rebound following the Liberation Day correction, because they remained anchored in a framework that no longer describes the emerging-market universe. The same instinct that led some of them to reduce risk at the outset of the Iran war again risks keeping them under-exposed. Markets have turned the page on emerging markets. We believe investors should do the same.