Fixed Income Boutique

Based in Zurich and New York, the Fixed Income Boutique is an active manager aiming to capitalize on market trends and inefficiencies.

In both the US and Japan, monetary policy is expected to support fiscal policy, even when central banks have other plans in mind. Kevin Warsh, the designated new US Federal Reserve (Fed) chair, envisions creating an “ideal Fed”. However, his restructuring plans are in direct opposition to US President Donald Trump's desire to maintain low interest rates. Similarly, the Bank of Japan (BoJ) aims to normalize interest rates and reduce its balance sheet. Yet, this is at odds with Prime Minister Sanae Takaichi's priorities, as she seeks support from the central bank for her economic policies.

Kevin Warsh faces a Herculean task as he aims to create an "ideal Fed" and maintain low financing conditions while simultaneously reassessing the collaboration between the Fed and the US Treasury. Each of these objectives may seem theoretically reasonable, but their combined implementation could prove counterproductive in practice.

Warsh believes that monetary policy should be based on convictions rather than being data- or forecast-driven. However, this approach would increase the likelihood of prolonged periods of excessively loose monetary policy, which could push long-term interest rates higher. One of Warsh’s convictions is that AI-driven productivity gains could enable higher economic growth without triggering inflation. Additionally, Warsh advocates for reduced transparency, meaning less communication from Federal Open Market Committee (FOMC) members. This lack of clarity could increase uncertainty among market participants regarding monetary policy, resulting in greater interest rate volatility and potentially increasing the term premium. Furthermore, Warsh has been a strong opponent of balance sheet operations such as Quantitative Easing (QE), which has historically been focused on the longer end of the yield curve and contributed to its flattening. In our view, these proposed Fed reforms are factors that would lead to a steeper yield curve, essentially the opposite of low financing conditions Warsh aims to achieve.

As if the task of creating lower interest rates under his vision of an “ideal Fed” were not daunting enough, Warsh also aims to realign the Fed’s collaboration with the US Treasury. In his view, the 1951 Accord conflicts with current practices, as the distinction between the central bank and the fiscal authority has become increasingly blurred. As a result, Warsh has called for a new accord to create a framework that would enable the Fed and the Treasury, potentially in collaboration with housing agencies Fannie Mae and Freddie Mac, to jointly address the reduction or adjustment of the balance sheet's size and composition.

One approach to reducing the balance sheet could involve gradually replacing maturing long-term bonds with shorter-term securities, such as Treasury bills (T-Bills). Alternatively, the portfolio of mortgage-backed securities (MBS) could be exchanged for T-Bills, aligning with recent announcements from Fannie Mae and Freddie Mac regarding their plans to purchase MBS to help reduce mortgage costs. This coordinated effort aims to minimize market volatility while shrinking the balance sheet. To offset the resulting tightening of financial conditions, Warsh may consider lowering policy rates.

Warsh frequently underscores the significance of the Fed's independence, but he also argues that fiscal policy should drive economic growth through low taxes and limited regulations, while monetary policy should focus on encouraging investment by maintaining low interest rates. This perspective evokes comparisons to the mid-1960s, when the Fed, under William McChesney Martin Jr., adopted a more supportive stance toward fiscal policy. However, we believe that such alignment between monetary and fiscal policy could, in practice, undermine the Fed's independence. The assumption that higher economic growth alone can stabilize deficits, despite increasing defense spending and ongoing government bond issuance, is likely to push term premiums higher, particularly when coupled with concerns about the erosion of the Fed’s independence.

In contrast, Donald Trump's economic agenda places a strong emphasis on housing affordability, with a particular focus on achieving lower mortgage rates. However, both a reduction in the Fed's balance sheet and a shortening of the maturity structure, as previously mentioned, would likely exert upward pressure on US Treasury yields and, by extension, on mortgage rates. We believe this highlights a clear conflict between Warsh's proposed plans and the objectives of the Trump administration. While Warsh contends that a smaller role for the central bank in the government bond market could promote fiscal discipline and eventually lead to lower long-term interest rates, this perspective appears to overlook the fact that higher long-term interest rates would initially be necessary to restore fiscal discipline.

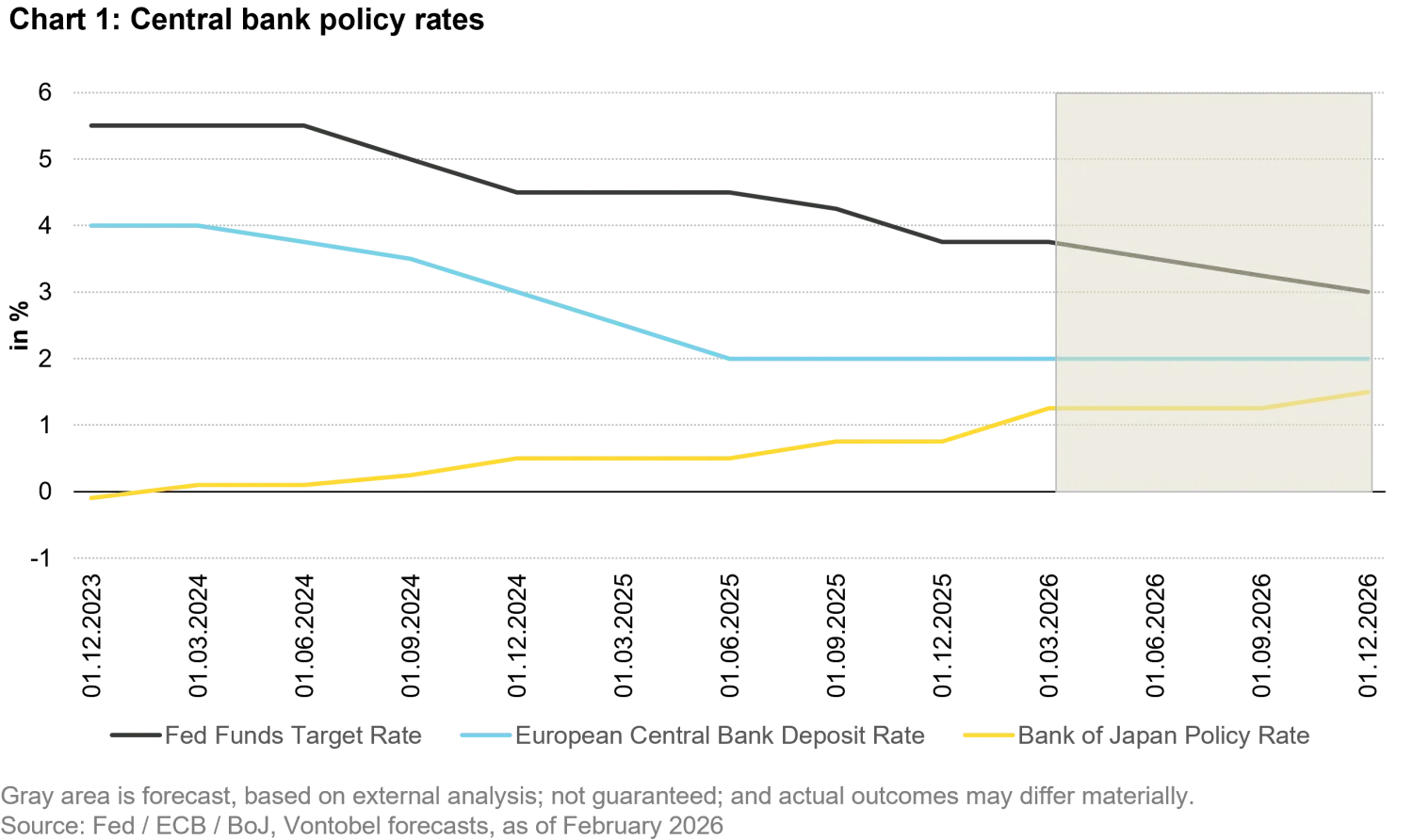

Even with oil prices spiking, we expect the Fed to cut interest rates in 2026. Before the oil price increase, the Fed Funds rate stood at 3.75%, which was above the neutral range of 2.5% to 3.5% and therefore remained slightly restrictive. Against the backdrop of a weakening labor market, our view aligned with market consensus that at least two rate cuts (25 basis points each) would take place in 2026. However, the market now assumes there will be no rate cuts this year. Despite this shift in market expectations, we continue to believe that at least two rate cuts will occur in 2026. However, we see limited potential for further declines in long-term yields, which is likely to result in a steeper US yield curve. Additionally, we expect the US dollar to weaken under this scenario.

In bond markets, good news is often bad news. When the economy performs well, bond prices tend to fall, and interest rates rise. As a result, borrowing becomes more expensive for debtors. This dynamic is particularly significant for Prime Minister Sanae Takaichi, who leads one of the world’s largest borrowers.

After her overwhelming victory in February’s snap elections, which secured her Liberal Democratic Party (LDP) a two-thirds majority, Takaichi now faces significant pressure to deliver ambitious reforms. With this supermajority in the upcoming lower house, the LDP will gain full control over all parliamentary committees, including the influential budget committee. This dominant position enables the party to pursue its vision of a "responsible and proactive" fiscal policy without needing to negotiate compromises with opposition parties.

The bond market is expected to closely scrutinize the government’s initial policy proposals to gauge how the LDP plans to balance "proactive" measures with "responsible" fiscal management in tangible terms. In recent years, the Japanese government has been working to consolidate its budget, with a target of limiting new debt issuance to approximately 2% of GDP by 2026. However, during her tenure leading a minority government, Takaichi had already signaled her willingness to expand this deficit. The specifics of her fiscal plans are therefore eagerly awaited and will become clearer in the coming weeks.

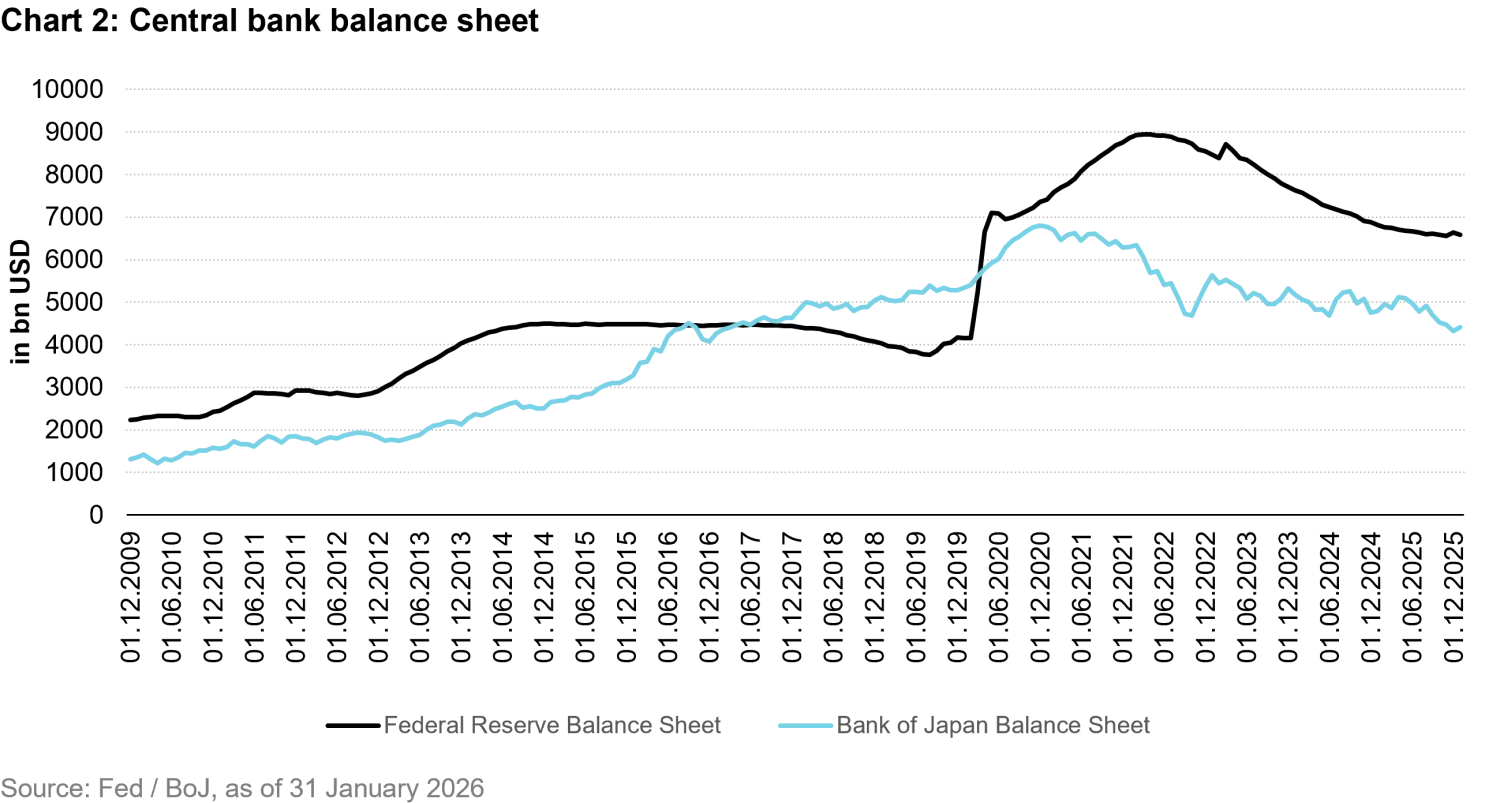

Japan's gross government debt recently exceeded 200% of GDP, a level considerably higher than that of most other developed countries. This high debt ratio was not a significant concern for many years, as interest rates in Japan remained near zero. Furthermore, the BoJ played a key role in keeping interest rates low by implementing its QE program, during which it consistently purchased more government bonds than the government issued.

In recent years, however, rising inflation has led the BoJ to gradually raise policy rates and reduce its bond purchases, buying fewer new bonds than those maturing. Over the past two years, this shift has led to a steady decline in the BoJ’s bond holdings. Consequently, the refinancing costs for government bonds have increased, potentially placing greater pressure on the national budget in the coming years. Since the end of 2022, the yield on 10-year Japanese government bonds (JGBs) has risen sharply, increasing by nearly 200 basis points from 0.25% to 2.2%. As a result, interest expenses are projected to rise significantly in the near future.

Similar to the US government, Prime Minister Sanae Takaichi advocates for a more accommodative fiscal policy and has called on the central bank, under the leadership of Kazuo Ueda, to maintain low interest rates to encourage investment and support ambitious spending plans. Nonetheless, we anticipate a gradual increase in policy rates as part of the ongoing normalization of monetary policy. In this context, 10-year yields are expected to approach 2.5%, particularly if political priorities remain undefined through 2027 and fiscal uncertainties persist.

Although 10-year real yields in Japan have recently turned positive, we believe they remain less attractive compared to real yields in the US or the Eurozone. Additionally, the supply of long-term bonds is projected to rise significantly. With the BoJ further reducing its bond purchases, the net issuance of JGBs to the private sector is expected to increase this year.

Against the backdrop of continued wage growth of 5%, we expect the BoJ will implement two additional 25 basis-point hikes, bringing the policy rate to 1.25% by the end of 2026. As a result, the Japanese yield curve is likely to experience a bear flattening.

The restructuring of the Fed, along with the US rate cuts we anticipate, is likely to weaken the US dollar against the euro. This could dampen inflation in the Eurozone, as import prices (particularly for raw materials and energy) would likely decrease, while the competitiveness of European exports could be negatively impacted. Additionally, Chinese goods, which may be redirected to the European market due to reduced demand in the US, could exert further downward pressure on prices.

At the same time, it remains uncertain whether economic growth in the Eurozone will be robust enough to prevent inflation from falling too far below the European Central Bank's (ECB) 2% target.

The ECB considered itself to be "in a good place" prior to the onset of the Iran conflict, and we initially agreed with market expectations that there would likely be no further policy rate adjustments in 2026. However, the ECB has a history of so-called "policy mistakes," and the market now anticipates that the ECB may have no choice but to raise rates in response to rising inflation. If the duration of the conflict extends beyond 4 to 6 weeks from the time of writing, there is a significant likelihood that the ECB could implement two rate hikes this year. This is particularly plausible given that the current deposit rate of 2% is at the lower end of the neutral range of 2% to 3%.