In April, we argued that emerging markets (EM) fixed income was better positioned to withstand the oil shock than it had been in 2022, and that we believed the asset class was poised for a strong rebound if de-escalation occurred in a relatively short time frame. De-escalation took longer than both we and the markets had expected, with the full-blown war lasting almost four months rather than weeks. But the rebound thesis was correct.

As the Strait of Hormuz has partially reopened, oil prices have fallen almost 40% from their March peak (although they remain 20% higher year-to-date (YTD)), and the inflation shock has been milder and shorter-lived than expected and likely to fade much faster than it did four years ago. As a result, pre-war trends have reasserted themselves, as expected. Inflows into EM fixed income were interrupted only in March and resumed in April, while the credit rating upgrade trend we had been observing continued through Q2, despite the war.

Oil volumes through the Strait of Hormuz started to recover even before the signing of the agreement between the US and Iran. As of the third week of June, oil flows were still roughly two-thirds lower than pre-war levels, but about three times higher than in May, and rising rapidly. Brent crude oil prices have now fallen to the low USD 70s per barrel. This is still a supportive level for oil-exporting countries and oil-related corporate issuers, while also being a price level that the global economy can handle well.

The second global inflation shock that markets were pricing in back in March did not materialize with anything like the magnitude of 2022. Headline inflation spiked, but core measures of inflation remained broadly anchored. While some EM central banks raised rates, most did not have to, and certainly not to the extent that markets had priced in back in March. This likely reflects the considerable credibility they have built over the past four years relative to their developed-market peers.

This outcome vindicates the core argument of our April article. After four years of restrictive monetary policy globally, the pass-through from an oil supply shock to consumer inflation is structurally smaller than it was in the aftermath of the pandemic, when policy was extremely loose and aggregate demand was rebounding into supply constraints. This more muted inflation shock, combined with yields that remain elevated, has allowed the asset class to remain resilient and deliver positive YTD returns, a sharp contrast to the double-digit negative returns of 2022. Moreover, recent inflation data from Eastern Europe to Mexico, coupled with the aforementioned drop in oil prices, suggest that this inflation cycle will also be much more short-lived than in 2022, which bodes well for fixed income, and particularly via local-currency rates.

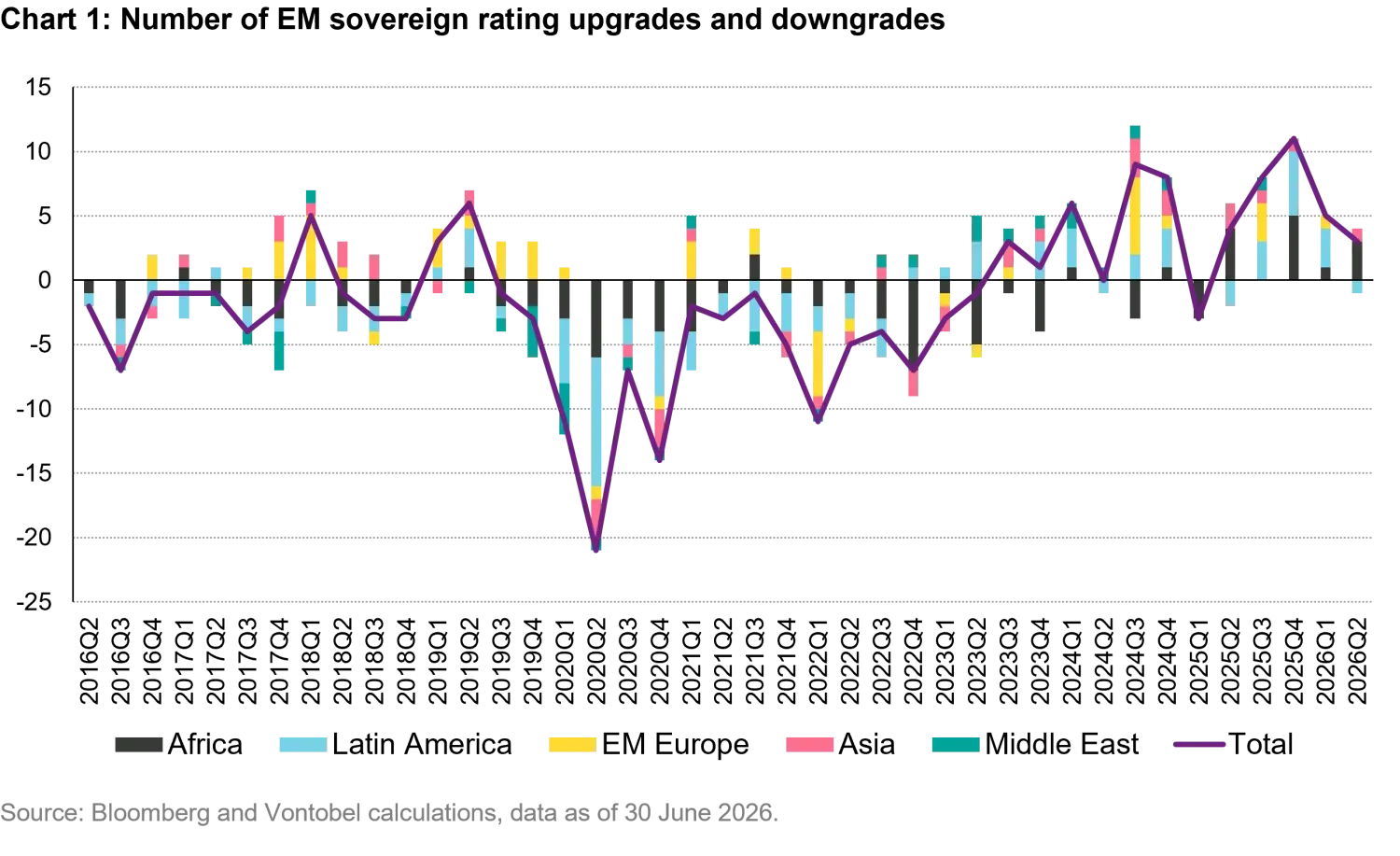

EM fundamentals have remained resilient through the war-induced shock. Over the past year and a half, we have highlighted the strong trend of sovereign rating upgrades, and we believed that there was a risk that this trend would at least pause during the war period as rating agencies could have waited for the uncertainty to dissipate. Instead, the trend continued unabated during Q2 2026.

Two major downgrades took place in Latin America (Colombia and Mexico) driven by long-term fiscal deterioration that was unrelated to the war and was largely anticipated. Meanwhile, several countries continued to be upgraded on the back of medium-term structural reforms. Argentina was upgraded by two agencies to B- in the same quarter; South Africa and Uzbekistan obtained their third BB equivalent rating; the Bahamas secured its third BB- equivalent rating; Nigeria and Ghana were upgraded to B by S&P and Fitch, respectively, and the Maldives avoided default and was upgraded to CCC-.

One of the common trends driving rating upgrades at a global level has been the accumulation of international reserves across continents. There was a risk that some EM central banks would make use of these reserves to defend their currencies. Only the Turkish central bank did so in a significant magnitude in order to defend the Turkish lira’s crawling peg, which is key to its disinflation program.

The other relevant pre-war trend, inflows into the asset class, also resumed after a brief interruption in March. As the oil shock faded and risk appetite returned, the pre-war inflow trend reasserted itself, with significant flows into the asset class during each month in Q2. Crucially, the AI boom that has supported a stronger-than-expected US economy and a rebound in the US dollar, has not derailed this trend. Global asset allocators appear to remain focused on seeking geographical diversification away from US-centric portfolios, a dynamic that we identified as structurally supportive of the asset class.

Global risk appetite remains elevated, and we expect this to remain the case over the summer, which bodes well for EM fixed income. EM hard-currency sovereign and corporate spreads are now back to their early February pre-war levels. Therefore, upside coming from spreads is now more limited on aggregate, but there are still ample relative value opportunities. And with the two previous trends being reasserted, we think that tight spreads are likely to persist for longer.

Oil-related relative value trades have been abundant this year. Six months ago, market sentiment toward oil prices was negative, and spreads from oil-exporting high-yield (HY) countries and oil companies were very elevated. At the time, we interpreted this as an asymmetric opportunity with greater upside than downside, given already depressed valuations for oil and oil-related issuers. By March, HY oil importers underperformed due to high oil prices, despite expectations that the conflict would be short-lived. By June, however, oil prices tumbled and oil importers once again outperformed exporters.

What we now see is that oil exporters are in a stronger position than before the war, as the average oil price for 2026 should remain substantially higher than the market expected at the start of the year. Oil-exporting sovereigns and oil and gas companies are poised to see stronger fiscal and external accounts this year, with some of them deleveraging significantly. Meanwhile, oil importing nations should still see some external (and in some cases fiscal) deterioration in 2026. The devil is in the details, and outcomes will vary on an issuer-by-issuer basis.

The dollar conundrum makes EM local currency tactically challenged but structurally well supported. An interesting tension for the second half of 2026 is the coexistence of a tactically strong dollar with structurally attractive EM currencies and rates. The US dollar has rallied recently, supported by US growth outperformance and the AI investment boom, which has drawn capital toward US assets. Unlike last year, when EM local assets had a stellar performance of almost 20%, this year, EM local has underperformed hard currency. That said, the asset class has been able to deliver positive returns (measured in USD) despite the recent dollar strength. There are several key themes that continue to support the asset class.

Tactically, while further dollar strength is possible, we believe elevated global risk appetite will also attract capital to carry trades in local-currency, including Frontier markets. In fact, four high-yielding Latin American currencies, the Colombian peso (COP), Brazilian real (BRL), Argentine peso (ARS), and Dominican peso (DOP), have delivered double-digit USD returns YTD despite the strong dollar.

Strategically, we view the asset class as relatively attractive. While hard-currency spreads are historically tight, local-currency real rates are near one standard deviation above their 10-year median. Moreover, the aforementioned diversification trend extends beyond credit risk and geographical diversification through EM hard-currency and encompasses currency diversification as well.

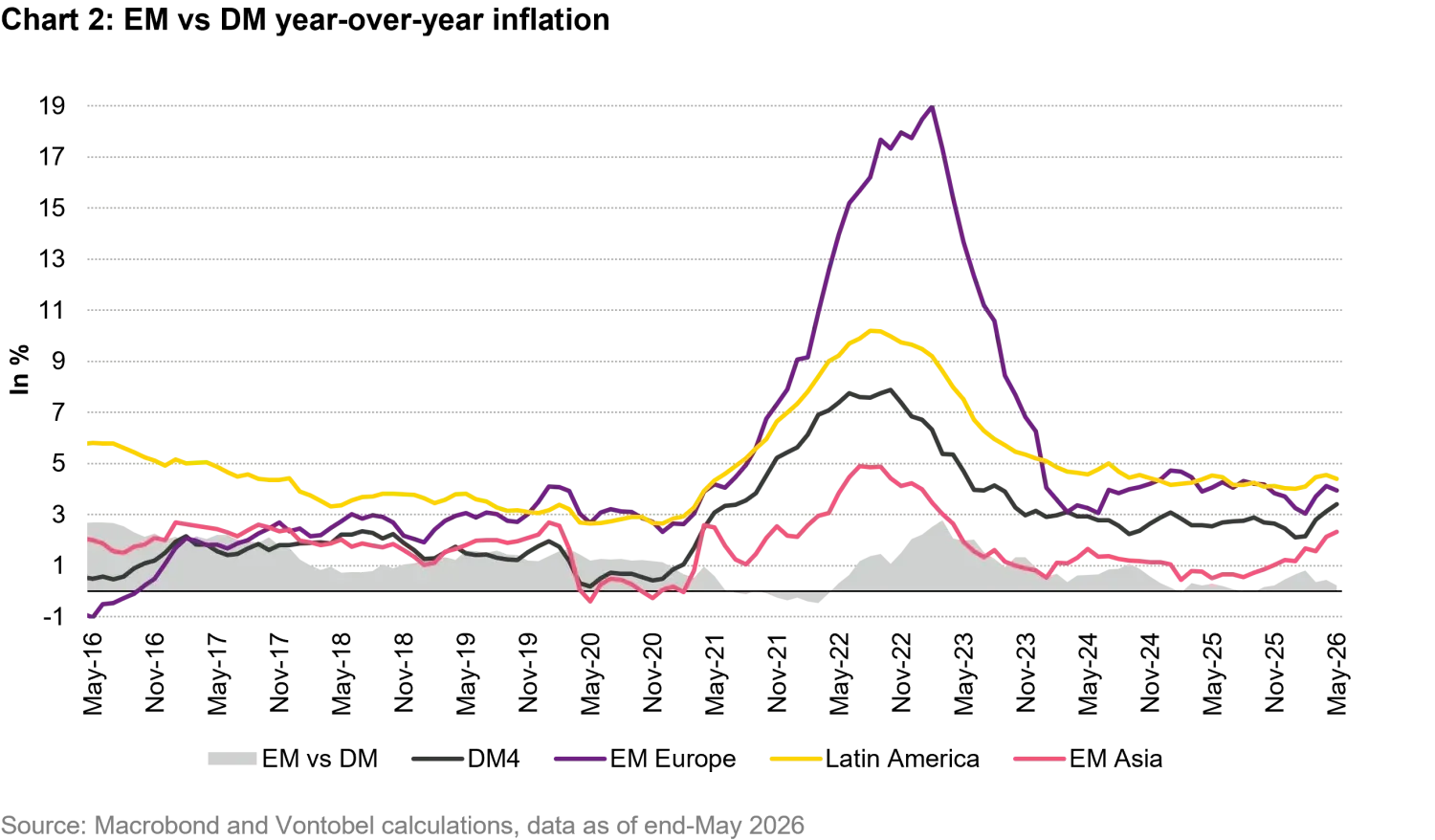

Finally, we believe that lower structural inflation in EM relative to developed markets (DM) is a powerful long-term tailwind for EM local assets. EM currencies no longer need to depreciate nominally at the same pace as they did before the pandemic, now that EM inflation is much closer to DM inflation (see grey area in Chart 2).

Back in April, we were cautiously optimistic given the very high uncertainty. With much of the uncertainty now resolved, and the positive EM trends being reasserted as we had expected, we return to a similar level of optimism as in our December EM fixed income outlook.