Conviction Equities

Concentrated and fundamentally driven high-conviction equity portfolios managed by four teams specialized in emerging markets, impact investing, thematic investing, and Switzerland.

From the oil embargo of the 1970s to Europe’s dependence on Russian gas and the latest tensions in the Middle East, energy has always been inseparable from geopolitics. Each disruption is accompanied by economic costs through higher prices, supply uncertainty, and potentially weaker growth. But it also forces countries to rethink security, resilience, and strategic autonomy. What does this mean for the energy transition?

History may offer some useful lessons. The 1970s oil shock exposed the vulnerability created by concentrated supply and ultimately led to strategic petroleum reserves, efficiency improvements, and diversification efforts across advanced economies. Decades later, Europe’s reliance on Russian gas put the spotlight on geopolitical risks embedded in energy markets. Today’s tensions involving Iran and the broader Middle East emphasize a similar message: dependencies that may make sense and be efficient during periods of stability can quickly become liabilities in a fragmented, multi-polar world. But we believe what distinguishes the present is the scale of the energy transition already afoot.

Some of the implications of the war in Iran were immediate and visible. Energy markets priced in a geopolitical premium as both physical disruptions and the risk of escalation increased uncertainty. Oil and gas prices are still highly sensitive to supply risks, while governments are resorting to emergency stock releases and subsidies. The effects also feed into inflation and public finances. But global responses have evolved.

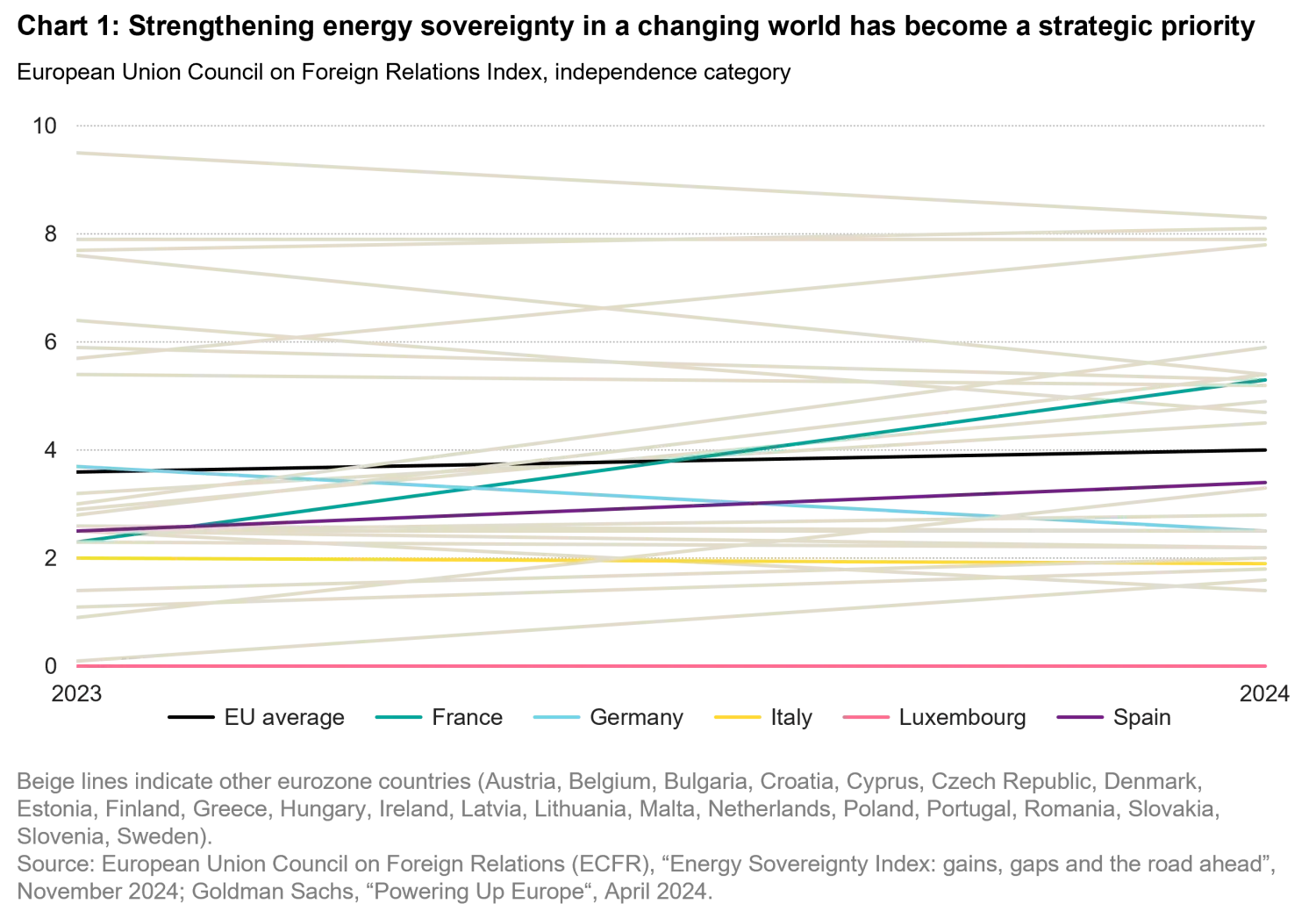

In the past, the solution to an energy crisis might have been to secure additional oil and gas supply. Today, there’s an increasing tendency to lean toward accelerating the transition. In energy markets, there have been three factors driving decisions, namely energy sustainability, security, and affordability. The move to cleaner energy is a steady, ongoing development. Energy security, and by extension energy sovereignty, is especially timely at the moment. Allies may not be as reliable a partner they once were and 24/7 energy supply is not a given anymore, which means governments are looking at affordability through a different lens, where it no longer is about getting the cheapest solution, but making sure it’s always available. In other words, they’re looking at it from a more strategic angle. Energy sovereignty is essentially a policy response to energy security (and perhaps affordability) and we believe it has become one of the main objectives (see chart 1), pursued through two main channels. The first is geographical diversification. Countries are seeking alternative suppliers to reduce dependence on any single region. Europe’s attempt to diversify away from Russian gas is one example. But diversification alone has its limits because it tends to replace one external dependency with another and so doesn’t eliminate systemic risk. Europe learned that lesson the hard way this year, because in trying to replace Russian gas, it had ended up trading one geopolitical risk for another: Iran. The second, and in our view the more sustainable path, is strategic autonomy, so investing in renewable energy and efficiency improvements to reduce exposure to volatile global commodity markets. The objective is to gain greater control over the systems that produce and distribute energy, versus just access to energy.

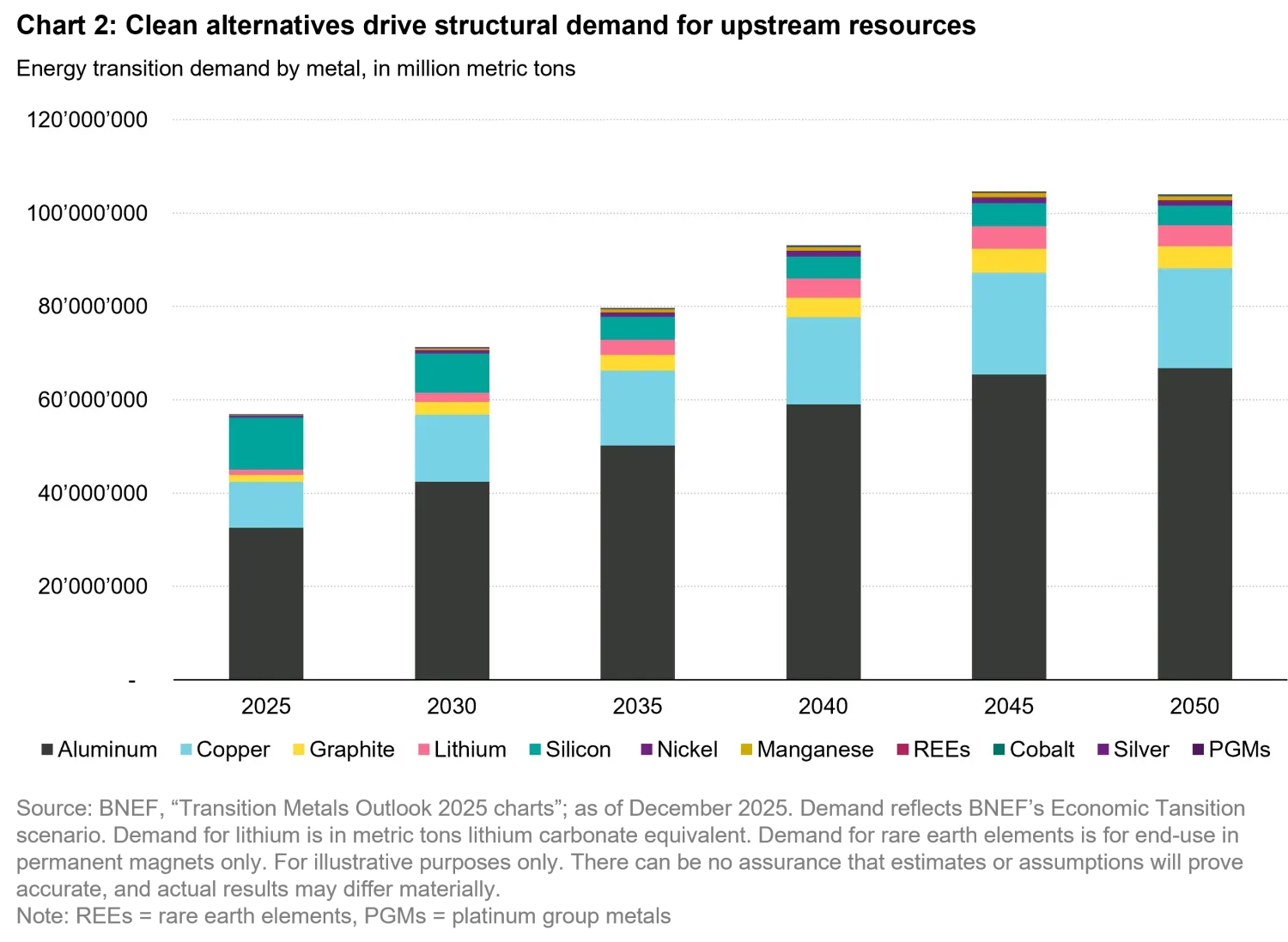

The push for renewables has a second-leg effect on the materials needed for the transition. Grids, storage, electric vehicles (EV) and heat pumps are just a few examples of areas that require a significant amount of materials. In addition, with all the buzz around artificial intelligence (AI), it’s important to remember that the race for AI is also a race for power as the infrastructure buildout requires massive amounts of energy.

That means that the geopolitical map of energy is changing. Influence is gradually moving away from traditional oil-producing states toward countries that control the technologies, processing capacity, and supply chains that support the energy transition.

Solar panels require silicon, silver, and indium. Wind turbines require rare earth elements for their permanent magnets. EV batteries require lithium, cobalt, nickel, and manganese. Grid-scale storage requires similar inputs at enormous scale. In our view, access to these resources and the ability to process and manufacture them has turned into a growing source of geopolitical leverage (see chart 2).

China currently occupies a leading position across large parts of the transition, especially in lithium refining, rare earth processing, battery manufacturing, and solar supply chains. Recent export restrictions on certain critical minerals to the West show how concentrated supply can be used as a strategic tool. This mirrors earlier forms of energy leverage, although the chokepoints are now minerals, processing facilities, and advanced manufacturing capacity instead of just oil pipelines.

That’s why governments are increasingly focused on securing the entire value chain, from upstream mining rights, midstream refining and processing, and downstream industrial manufacturing. Building supply chains outside of concentrated production hubs has become a strategic objective for the US, Europe, and several Asian economies. Policies now include tariffs, export controls, production subsidies, and the accumulation of strategic reserves for critical materials1, mirroring the logic of the Strategic Petroleum Reserve.

The examples above show that commodities are seen as the backbone of this transformation as the enablers of the future. But the transition also faces an important structural challenge. Supply growth is struggling to keep pace with projected demand. New mining projects often require years of development, while environmental constraints, permitting requirements, and geopolitical considerations can slow expansion. This growing mining gap is likely to keep commodity markets structurally strong over the coming years. That’s why we believe the circular economy (recycling and reusing materials) will play an increasingly important role, even if it can’t replace primary supply.

We believe the transition won’t be linear, but instead proceed in phases, with periods of acceleration followed by setbacks and bottlenecks, like two steps forward and one step back. In our view, long-term strategies trump reactive policymaking, which may address short-term disruptions, but does little to resolve the structural imbalances emerging across energy and commodity systems. This is already visible in commodity markets. The world may be in a new commodities bull cycle that kicked off in 2020, driven by resilient demand, structural supply constraints, and a growing wave of global stockpiling, which we believe warrants a strategic rather than tactical allocation to commodities and real assets. The current conflict in the Middle East, on top of the geopolitical and supply chain disruptions of the past few years, has created an incentive for countries and companies alike to increase inventories of oil, metals, rare earths, and even food as a buffer against future shocks. We believe oil prices are poised to stay elevated over the next year or two as governments plan to refill inventories more than before the war in Iran, and countries that previously didn’t have strategic reserves will start building them. We believe commodities are in a position to benefit from this stockpiling trend going forward. This will also likely encourage efforts to accelerate electrification as it is one way to reduce dependencies on oil and gas imports.

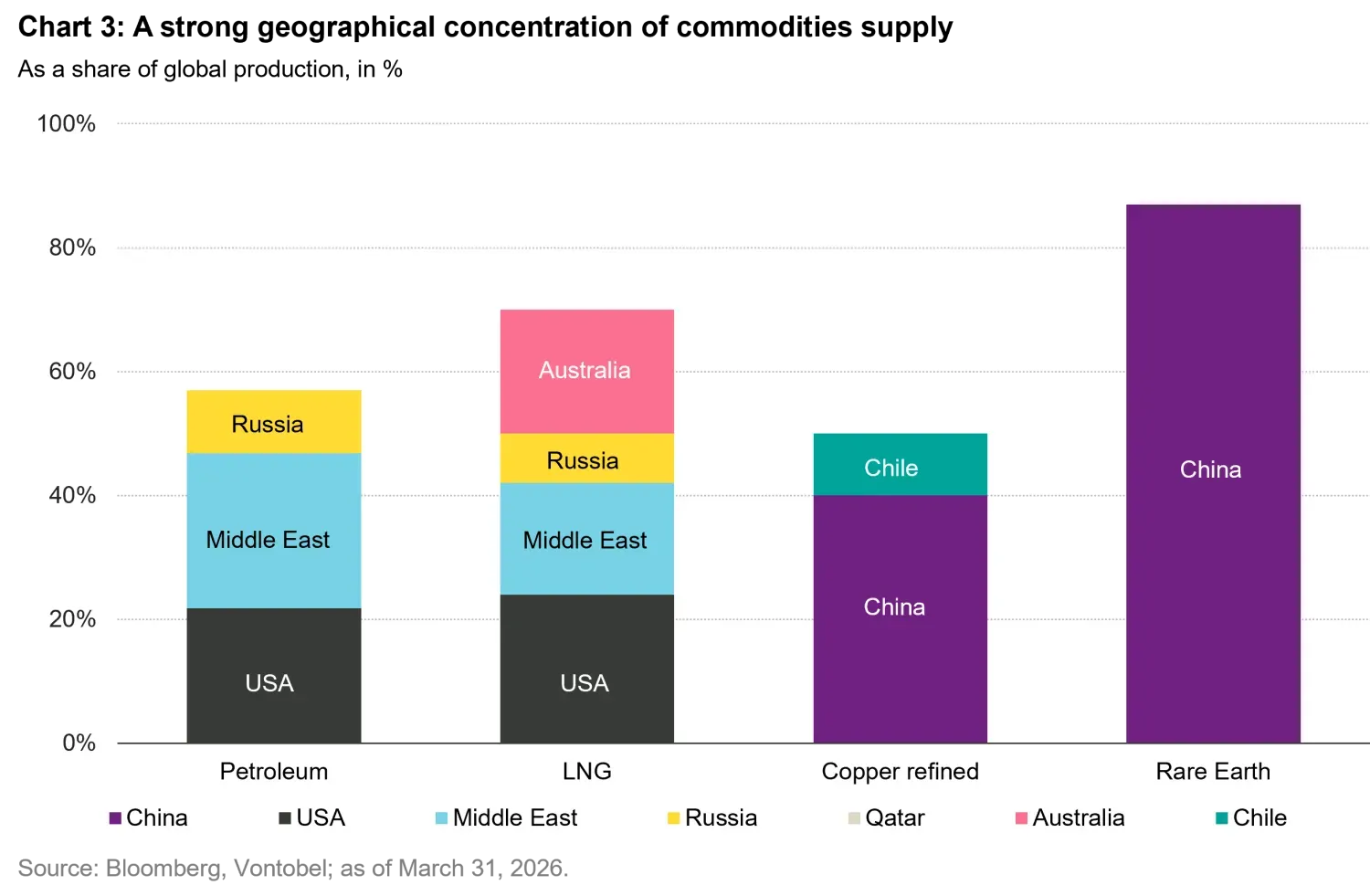

The last few years have showcased the risks associated with concentrated commodity supply (see chart 3). Russia’s reduction of gas flows into Europe, China’s restrictions on critical mineral exports, and the US cutting off Venezuelan oil to China and India have illustrated that access to key commodities can no longer be taken for granted. And in an increasingly deglobalized environment, governments are prioritizing domestic supply chains where possible and building strategic reserves where they are not, and not just for metals like copper and aluminum, but for energy and agriculture as well.

The ongoing conflict in the Middle East only emphasizes these trends. Higher and more volatile energy prices may also accelerate certain forms of structural adjustment in demand, as companies and households invest in more efficient technologies, electrification, and alternative energy sources. This raises the possibility that the current period could eventually be viewed as an important inflection point for global oil demand growth (as in, are we approaching peak oil demand in 2026?). We believe oil demand is unlikely to fall abruptly. Electrification takes time, and oil will likely still play a crucial role in transportation, industry, and petrochemicals for years to come. Demand may plateau for a decade and then gradually trend lower, but continued investment in exploration and production will be necessary during the transition period. A premature withdrawal of capital from the sector could create severe supply shortages and price spikes that would disproportionately affect energy-importing economies in Europe, Asia, and across emerging markets.

We believe the world is moving toward a new energy order that prioritizes autonomy, diversification, and strategic security. The repeated supply shocks of recent years (first through Russia and now through tensions in the Middle East) have shown the importance of both energy independence and commodity security for long-term economic stability in a world where energy and geopolitics are increasingly intertwined.

1. Source: The New York Times article, published February 7, 2026. https://www.nytimes.com/2026/02/02/business/trump-critical-minerals-stockpile.html; European Commission, Critical Raw Materials Act, https://single-market-economy.ec.europa.eu/sectors/raw-materials/areas-specific-interest/critical-raw-materials/critical-raw-materials-act_en

Important information: For educational and informational purposes only. Diversification does not protect against the risk of loss. References to companies for illustrative purposes only. Information provided should not be considered a recommendation to purchase, hold, or sell any security nor should any assumption be made as to the profitability or performance of any company identified or security associated with them. Any projections or forward-looking statements regarding future events or the financial performance of countries, markets and / or investments are based on a variety of estimates and assumptions. There can be no assurance that the assumptions made in connection with the projections will prove accurate, and actual results may differ materially.