Markets have turned the page on war. Have you?

Asset management

Key takeaways

In the current environment, we believe:

- Markets returning to pre-war levels are not a sign of complacency. They are sending a message.

- The macroeconomic shock may be real, but it is unlikely to be big enough to derail the strong industrial upswing driven by uninterrupted capital expenditue in artificial intelligence.

- Any inflationary push is likely to be temporary or ultimately give way to a disinflationary demand shock. Interest-rate cuts may be postponed, but are still on the table. In the meantime, fiscal policies remain extremely accommodative.

- Risks lie elsewhere (credit markets, US employment, AI over-investment, etc.) but are unlikely to materialize before 2027.

- Investors may consider remaining or returning overweighted in equities, with a focus on the winners of the K-shaped economy: Hardware, network equipment, electrification and clean energy, transition materials, etc.

- Emerging markets have already resumed their outperformance and are likely to extend their gains in a context of intensified diversification away from US assets.

On April 15, the MSCI All Country World Index retraced the record level it had reached on February 25, just two days before the launch of US and Israeli airstrikes on Iran. Since the ceasefire announcement on March 30, equity markets have rebounded continuously, erasing the already surprisingly contained impact of five weeks of conflict in 12 consecutive sessions. This recovery has occurred even though hostilities are not officially over, and their consequences, in terms of energy supply and the prices of oil, gas, and a broad range of derivative products, are unlikely to reverse in the very near term.

To many observers, this snapback feels premature, perhaps even reckless. It would indeed be tempting to contrast the extremely strong earnings-per-share (EPS) growth assumptions currently embedded in valuations — +17% for US equities in 2026 (following +13% in 2025) and a striking +40% for Asia ex-Japan, with the rather uninspiring macroeconomic readings of recent months. The US economy closed 2025 on an annualized growth of just +0.5% and may have rebounded to no more than +1.25% in Q1 2026, while a (distinctly) less favorable volume/inflation composition is likely to weigh further on activity in the weeks/months ahead, in our view. This divergence continues to leave many investors circumspect, struggling to reconcile the equity rally with any conventional reading of current or expected macroeconomic fundamentals.

Yet this market dynamic points to a dual reality. First, markets have internalized over the past year what may be the only true guardrail likely to reverse the initiatives of the US administration: financial asset prices — equities and interest rates — and their feedback into public opinion. The paradox is that this early “TACO”1 assumption at the start of the conflict helped contain declines across equities, credit, and rates, perhaps prolonging hostilities beyond the initially anticipated horizon. The acceleration of the decline in US indices from March 25, combined with rapidly increasing fuel prices for American drivers, appears nonetheless to have precipitated the pause in hostilities. Precarious as it remains, far from guaranteeing a rapid normalization in energy prices, the ceasefire was sufficient to redirect market attention back to more fundamental drivers of equity valuations over the next few months.

The deeper foundation: An AI/industrial upcycle likely to resist the oil shock

The second reality markets point to is that the current macroeconomic shock, while real, is not of sufficient magnitude to derail the powerful industrial upswing that has been underway since 2024. The engine of that upcycle is AI-related capital expenditure (capex), which shows no sign of throttling down. In a global economy where growth has become so uneven between industries, sectors, themes, and factors (i.e., the K-shaped economy in the US, the dual-speed economy in China), focusing on aggregated GDP growth as a single guide for the underlying dynamic of the economies has become increasingly irrelevant. While “New Economy” sectors enjoy double-digit revenue growth, very high expectations, and strong earnings momentum, traditional sectors that do not benefit directly or indirectly from this skyrocketing demand continue to display uninspiring figures. Of the very optimistic 23% EPS growth expected for S&P 500 companies, more than 70% would come from “New Economy” listed entities, mostly in hardware and semiconductors, along with transition materials and energy, while “Old Economy” sectors’ EPS growth would be limited to 7%.

The AI-driven industrial upcycle at play since 2024 has proven, through five weeks of geopolitical shock, essentially immune to disruption. Hyperscaler capex commitments across the major US platforms are running at an aggregate annualized pace in excess of USD 250 billion, with revisions so far only to the upside. This wave of spending is not discretionary in the short run: it reflects strategic imperatives tied to competitive positioning in a "winnter-takes-all" technology race. The result is a (very high) floor under demand for semiconductors, networking hardware, power infrastructure, and a wide range of industrial inputs — a floor that geopolitical turbulence has so far failed to crack.

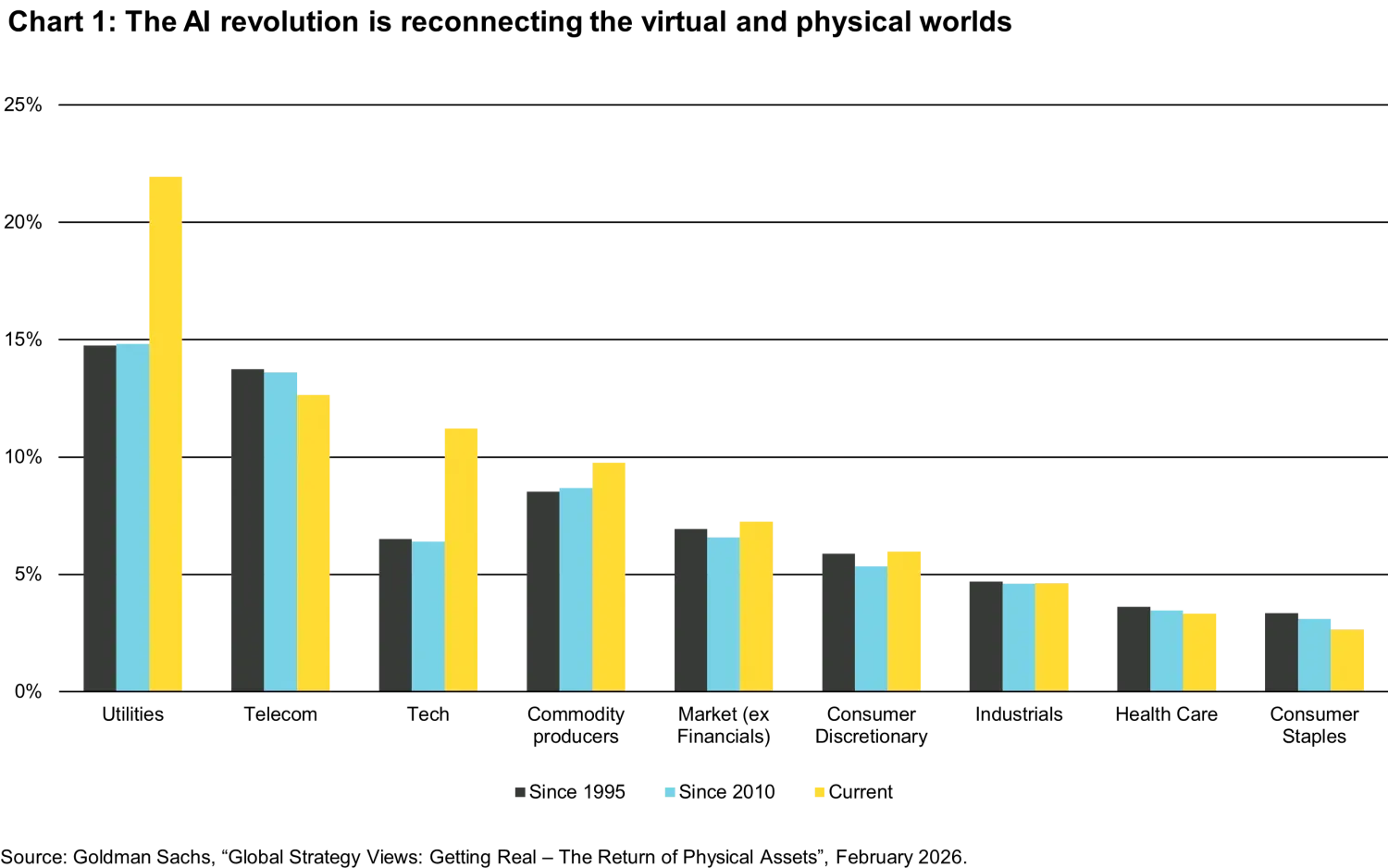

The electrification theme has offered one of the most vivid illustrations of this dynamic. Utilities, grid infrastructure, and energy equipment names not only held up during the conflict but in several cases outperformed broader indices. That's a counterintuitive but telling signal. Paradoxically, the geopolitical shock has reinforced the case for energy sovereignty, accelerating policy commitments across Europe and Asia that translate directly into equipment demand, as highlighted at the very start of this year2. What began as a theme driven primarily by AI-related power consumption has acquired a second, equally durable engine. We believe this powerful combination is likely to make electrification among the more compelling themes within equities.

Inflation: Decoding signal from noise

One of the most persistent sources of investor anxiety is the inflationary impact of tariffs and supply-chain disruptions. Energy cost pass-through is likely to generate significant volatility in headline inflation in the coming months. Investors were already struggling to disentangle the impact from past tariffs and expected interactions between possible tariff reimbursements following the US Supreme Court decision and the new temporary measures decided by the US administration. We do not dispute that, in the coming months, inflation is likely to be higher and real growth is likely to be lower than the average baseline scenario most economists had in mind at the start of the year. However, in terms of growth impact, this deviation is likely to be felt mostly in traditional sectors, accentuating the fractured dynamic within economies. The risk is not that this dynamic is ignored, but that it becomes over-interpreted as evidence of a new inflationary regime. With an oil intensity reduced by nearly a factor of four since the early 1970s, and with much less rigid labor markets, a much bigger energy shock would be required to trigger such a regime change.

The practical implications for central banks are straightforward. Neither the US Federal Reserve nor the European Central Bank faces a scenario in which rate hikes would become a rational response to a first-round supply shock, even a significant one. In a benign scenario, tariff-induced price pressures prove transitory as supply chains adjust, allowing market prices to revert closer to their initial levels. In a more adverse case, the resulting demand destruction it induces would eventually lead to disinflation, again mostly concentrated in traditional sectors. Our base case now pencils in the first Fed rate cut at the end of the year rather than Q3, but the direction of travel is unchanged. A rate-hiking cycle would require a dislocation in long-term inflation expectations that the current data, volatile as it is, has not produced and is, in our view, close to producing.

Fiscal policy: Global reloading of the fiscal engine

Fiscal policy is emerging as the final piece of the resilient global growth story, with a positive impulse building across major regions. In Germany and the broader euro area, the shift has been driven by higher defense and infrastructure spending, marking a move away from years of fiscal restraint. In the US, the One Big Beautiful Bill is providing a near-term lift to household disposable income through tax refunds, helping to cushion the impact of higher oil prices, while also offering incentives for corporate capital expenditure. At the margin, the US fiscal stance could become even more supportive if lost tariff revenues linked to the International Emergency Economic Powers Act (IEEPA) are scaled back and not fully replaced through alternative trade measures. In Japan, policy under Prime Minister Sanae Takaichi remains firmly oriented toward continued fiscal expansion, with targeted stimulus measures aimed at reinforcing domestic demand.

Risks worth monitoring — and when they may matter

A bullish tactical view does not ignore risks; it requires being honest about their hierarchy and timing. We identify three areas that may deserve close monitoring, none of which we believe poses a material threat to markets within a six- to nine-month horizon.

- Private credit markets. The rapid expansion of this asset class over 2022–2025 has created exposures whose quality is difficult to assess in real time. Should economic conditions deteriorate more than our base case assumes, refinancing pressure and potential covenant breaches could generate negative feedback loops for broader risk appetite. We are monitoring credit spreads, secondary market liquidity in private credit vehicles and deal flow statistics as leading indicators.

- Labor markets. US employment data appear resilient and anemic at the same time. The unemployment rate has remained remarkably stable, but mostly as a result of a decline in the labor force (probably due to a negative immigration-related supply shock). Employment data (jobless claims, the quits rate, ISM employment sub-indices) have softened enough to warrant attention. Growth in the "New Economy" has been relatively jobless, and how this transition will unfold (human replacement or productivity gains generating higher real labor income growth) is not clear yet. A decisive deterioration would lead us to revise our earnings outlook for consumer-cyclical sectors and challenge the sustainability of the EPS growth trajectory currently priced in by the market.

- AI deployment velocity and structural sustainability. The pace of AI adoption raises legitimate questions about absorption capacity: whether enterprises can monetize the technology quickly enough to justify current infrastructure spending levels, and whether workforce displacement effects begin to generate social or regulatory friction. This could result in a capital overhang and capex destruction, or simply in a normalization of equipment demand that may lead to large overcapacities across industries. In our judgment, this is a 2027 issue at the earliest, not a 2026 one — but it is worth flagging as a source of potential volatility once the current capex cycle matures.

In the meantime, we believe the window is wide open and is one of the few offering such good visibility. EPS growth, both from technology leaders and from cyclical and industrial companies riding the wave of AI-driven demand, is tracking toward one of the stronger years of the cycle. We see no near-term catalyst that would close that window prematurely.

Investment implications

Our positioning reflects both the conviction and the risk hierarchy described above and currently translates as follows in our equity portfolios:

- Overweight semiconductors and AI-enabling technology. AI capex spending shows no sign of plateauing, and earnings revisions in this segment have been the most consistent across the market. Our highest conviction remains in infrastructure enablers: hyperscaler suppliers, advanced packaging, and custom silicon.

- Overweight electrification and energy infrastructure, and transition materials. The conflict has reinforced, not weakened, the political and economic case for grid modernization and energy sovereignty. This is a multi-year structural theme with a growing list of policy catalysts across Europe and Asia. We believe relative valuations remain interesting given the visibility of the earnings stream.

- Selective overweight in capital goods and industrials. Companies with direct exposure to data-center construction, power equipment and critical infrastructure supply chains are benefiting disproportionately from the AI build-out. We remain selectively overweight in names combining pricing power with long order backlogs, which we believe can offer a degree of earnings visibility that is rare in the current macroeconomic environment.

- For all the reasons above, and because they have again demonstrated their resilience in face of a global trade and geopolitical shocks, as they did last year following Liberation Day, we maintain an overweight position in emerging markets, especially in parts of Asia and Latin America, relative to developed markets, especially the US. The conflict has further eroded confidence in US institutional pillars, a cornerstone of its past exceptionalism. Diversification is likely to favor those emerging markets and industries likely to benefit from AI, electrification, and energy sovereignty themes.

- Beyond the AI/industrial upcycle, conviction is more selective, with healthcare and financials currently providing shorter-cycle tactical opportunities, in our view. We remain neutral to underweight on most other market segments. In such a bifurcated global economy, we believe focusing on the winners can be an effective strategy.

Many investors missed last year's exceptional rebound that followed the Liberation Day correction as they remained cautious in the uncertain political and geopolitical environment. This type of backdrop is becoming part of the new normal. But when risk is “everything, everywhere, all at once,” it is practically nowhere. This does not mean it should be ignored, but its true economic consequences should be factually analyzed and confronted with current structural dynamics. In the present case, while anything is possible, we don’t see the conflict – in its current equilibrium – morphing into something that could derail the very strong dynamic supported by AI capex and accelerated transition towards a new economy. We believe investors may want to consider these factors to help prevent similar missteps.

1. Unofficial term, acronym for "Trump always chickens out", suggesting US President Donald Trump makes threats or announcements and then doesn't follow through.

2. See https://am.vontobel.com/en/insights/our-world-in-flux-calls-for-energy-sovereignty

Important Information: Any projections or forward-looking statements herein are based on a variety of estimates and assumptions. There can be no assurance that those estimates or assumptions will prove accurate, and actual results or events may differ materially.

About the authors

About the authors

Topics:

Related insights

Replay: Rates, credit & market reality — what matters now?

Power moves: The new energy order

Portable Alpha: Rethinking the Architecture of the Portfolio

Still waters run deep in global markets

Emerging markets: the train has left the station, but you can still catch it