Quality Growth

Global equities specialists since 1984. We provide a boutique investment experience for institutional and intermediary clients around the world.

Many of us are familiar with Aesop’s fable, The Boy Who Cried Wolf. A young shepherd repeatedly tricks villagers into thinking a wolf is threatening their flock. When a wolf finally appears, his cries are ignored, and the flock is lost. In some retellings, the wolf eats the boy as well.

Are investors acting like villagers assuming the real wolf will never show up?

After the Global Financial Crisis (GFC), markets have become desensitized to a barrage of voices crying wolf. Headlines about the Eurozone crisis? Buy the dip. China slowdown? Buy more. A global pandemic? Load up. Tariffs? No problem. Initial sell-offs have been followed by sharp rebounds as central banks and governments (quantitative easing, zero-rates, direct stimulus, policy reversals) have come to save the day. All this has led to complacency about the safety of the proverbial flock and a dismissiveness of potential threats. And so far, that has paid off handsomely.

In this environment of seemingly little risk, it’s not surprising that investors open their wallets when markets get shaky and that valuations have expanded. At the same time, many investors decided they don’t need to own defensive companies (those that grow slower than the market but protect in a downturn), since downturns rarely come and when they do, they don’t last.

This nonchalance, however, comes at a cost. Periods of increased stability can lead to structural fragility, and eventually a Minsky moment.1 Minsky moments occur after an extended period of calm that lends to more risk-taking, which sets the markets up for an extended and deep decline. By assuming all recoveries are V-shaped, many investors have removed from their portfolios the defensiveness needed when markets don’t quickly recover. Higher valuations, investors not positioned for any type of extended downturn, and increasing global debt levels are a toxic brew, in our view. By shunning steadier investments, investors risk lacking the funds to buy great companies at attractive prices during these downturns.

When and what sets off the markets is not predictable. Why did the dot-com bubble blow up in March of 2000? Why did Lehman fail in September of 2008? Whether the current hostilities in the Middle East or the instability in private credit becomes the catalyst for a major market fall is less important than the protective perimeter around the village. Having some defensive exposure is perhaps even more critical as market complacency increases. “Buy the dip” is great if declines are shallow and quick. However, as they extend, investor flows can reverse, often dramatically and without warning.

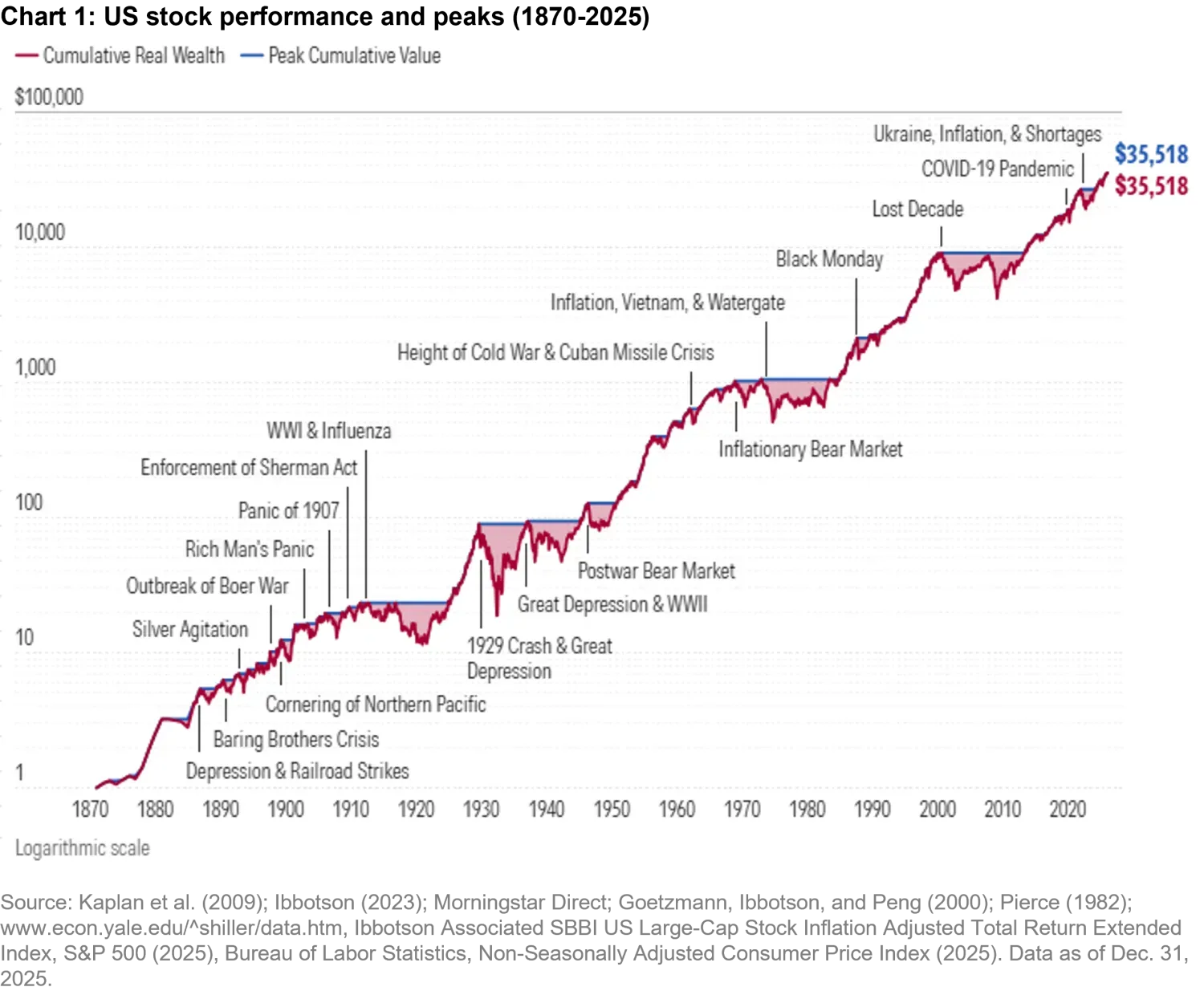

Morningstar2 recently published an interesting chart. It shows US stock performance from 1870 to today and examines large market declines and the time it takes, in real terms, to return to previous market peaks. Using Morningstar’s definition of major drawdowns, from 1870 until the GFC, the average large decline was about 36%, and it took roughly 4.6 years from the market’s peak to achieve real new highs. Since the GFC, the average decline has been closer to 24%, with peak-to-trough drawdowns only lasting about 1.4 years before new highs, roughly 70% faster than before the GFC.

We’ve seen other shallow declines and short-duration downturns. These periods have all eventually been followed by deeper, longer declines.

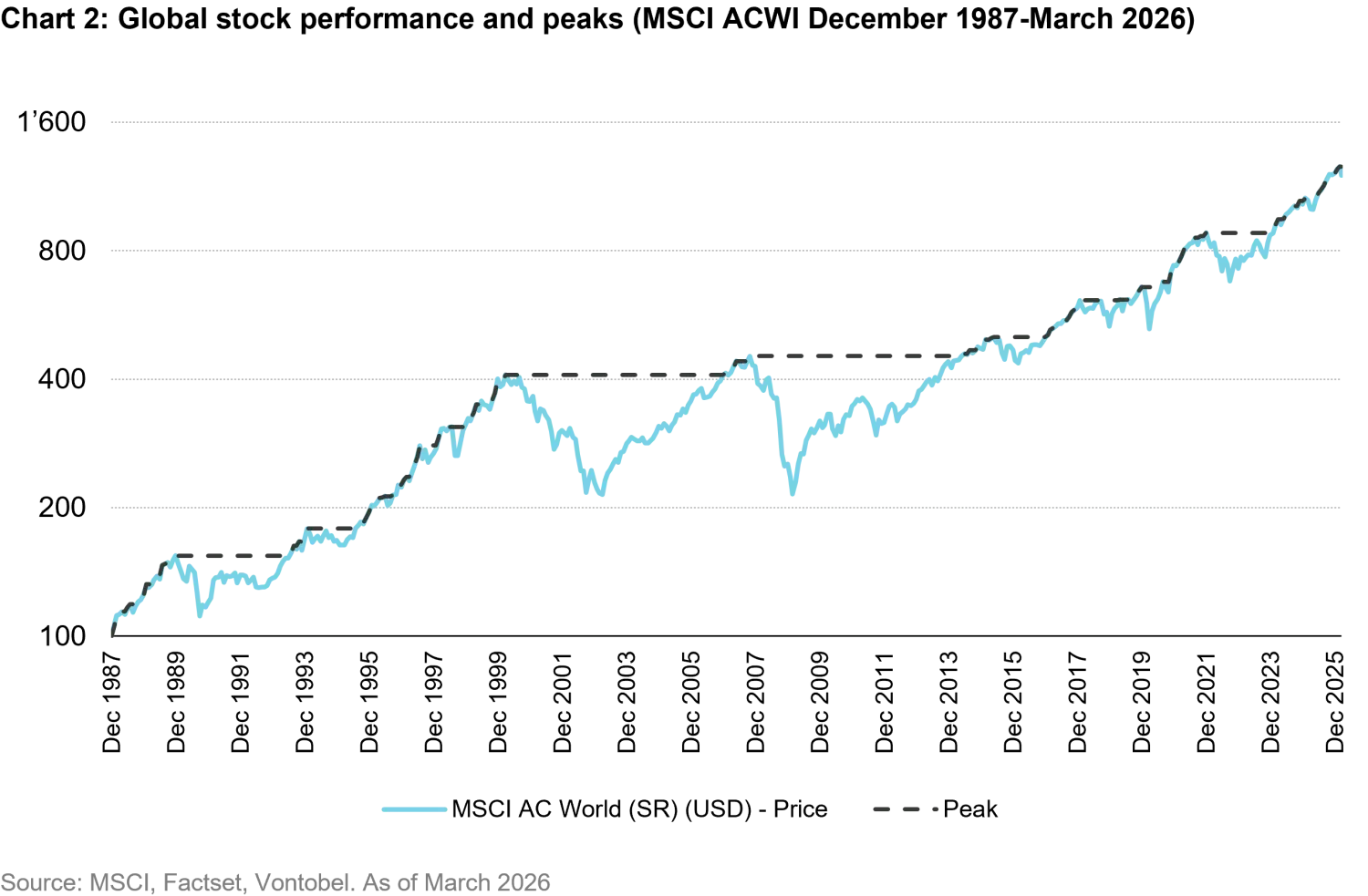

For those who think this is safely in the distant past and therefore cannot happen today, it is useful to remember that a lost decade is a modern reality. It was only 13 years ago, in 2013, that the US market finally returned to its year-2000 levels in real terms. As shown in Chart 2, this pattern shows up globally as well.

Around the world, short and shallow downturns have conditioned many investors to step further out on the risk curve. We think that’s a mistake. In our view, investors should not extrapolate from the last 15 years and assume there can never be a wolf. Downturns are inevitable. We believe that higher-growth quality businesses balanced with steadier but more moderate growers improves investment returns over a full cycle. The steadier companies protect capital during downturns and become the funding mechanism to rebalance into faster-growing opportunities, when the wolf retreats to its den.

1. “Minsky moment” was coined in 1998, referencing economist Hyman Minsky’s financial instability hypothesis that posits stability in markets leads to instability.

2. https://www.morningstar.com/economy/what-weve-learned-150-years-stock-market-crashes