Quality Growth

Global equities specialists since 1984. We provide a boutique investment experience for institutional and intermediary clients around the world.

At Quality Growth, we rarely invest in IPOs. We want to see a long history of profitability and understand how the business evolves in both good and bad times. Galderma’s IPO was a special case: It began as a joint venture between Nestlé and L’Oreal, two great global consumer companies we had owned and followed for decades. A dermatology-focused franchise, with brands from Cetaphil to Sculptra, it was built on the same compounding logic as these consumer staple stalwarts.

Galderma’s aesthetic business was easy to understand. What’s not to get about an aging, affluent population with disposable income in search of eternal youth? In a massive global market growing at double-digits where AbbVie’s Botox is the “Kleenex,” Galderma’s fillers and biostimulators were gaining traction. In fact, Botox has been underperforming while Galderma's Dysport has been taking share. AbbVie is a sprawling $300 billion pharmaceutical giant and aesthetics is simply one division among many. Galderma is a pure-play dermatology company where aesthetics is an existential priority. The focus on dermatologists also helps Galderma’s skin care brands compete versus more diversified competitors.

Most of what the therapeutics business sold was off-patent, dermatological medication that wasn’t growing. However, the company had a pipeline biologic called nemolizumab, or “Nemo” for short. This drug wasn’t like other itch medications — Nemo goes straight to the nerve that signals the brain that a part of the skin is itchy. This would be Galderma’s first biologic and had the potential to turbocharge the company’s growth. But it also added risk to the forecast: Would it be approved? And how big could it be? Would dermatologists prescribe it? These were unknowns.

In terms of approval, we thought the risk of a rejection was minimal. Galderma only had the rights to the drug outside of Japan and Taiwan, and Nemo was already approved in Japan. This meant that safety and efficacy had already passed one regulatory body. Interestingly, Zoetis had a similar type of drug approved for dogs. The questions we had were therefore largely commercial. We didn’t know if insurance would reimburse it, or if it could compete in a category defined by Regeneron’s blockbuster drug, Dupixent.

I spoke to a friend of mine, a dermatologist, who was excited about a potential approval. She explained that one of the worst feelings she has as a doctor is when she knows what is wrong with a patient but doesn’t have a way to fix the problem. Dupixent was a gamechanger for many patients, but there were some patients for whom it was not the right solution. I was encouraged by this but not wanting to rely on an “N of 1,” I asked our investigative analysts to speak with more dermatologists, specifically those who specialize in the treatment of itching. They secured access to The American Skin Association annual gala, where they spoke to prior Galderma leadership who are now pursuing private ventures. They made appointments at medspas, spoke with aestheticians, and attended conferences dedicated exclusively to atopic dermatitis. We participated in the IPO, and as we gained conviction, we increased our holding in the company.

In our investigations, we learned that the reason the pharma industry had neglected “itch” (vs. pain) for so long is that the source is often unknown. It’s very difficult to tell whether an itch starts with the skin, the kidneys, the liver, the thyroid, the nervous system, an undiagnosed cancer, or a mental health condition — all of which look the same on the surface. As a result of this, and a lack of great products, itch was treated as an afterthought, a symptom rather than a condition, to be managed with antihistamines and corticosteroids developed generations ago. But the science improved, and doctors were learning that biologics (drugs made from living cells vs. synthesized compounds) allowed medicine to make connections between symptoms and causes with more precision.

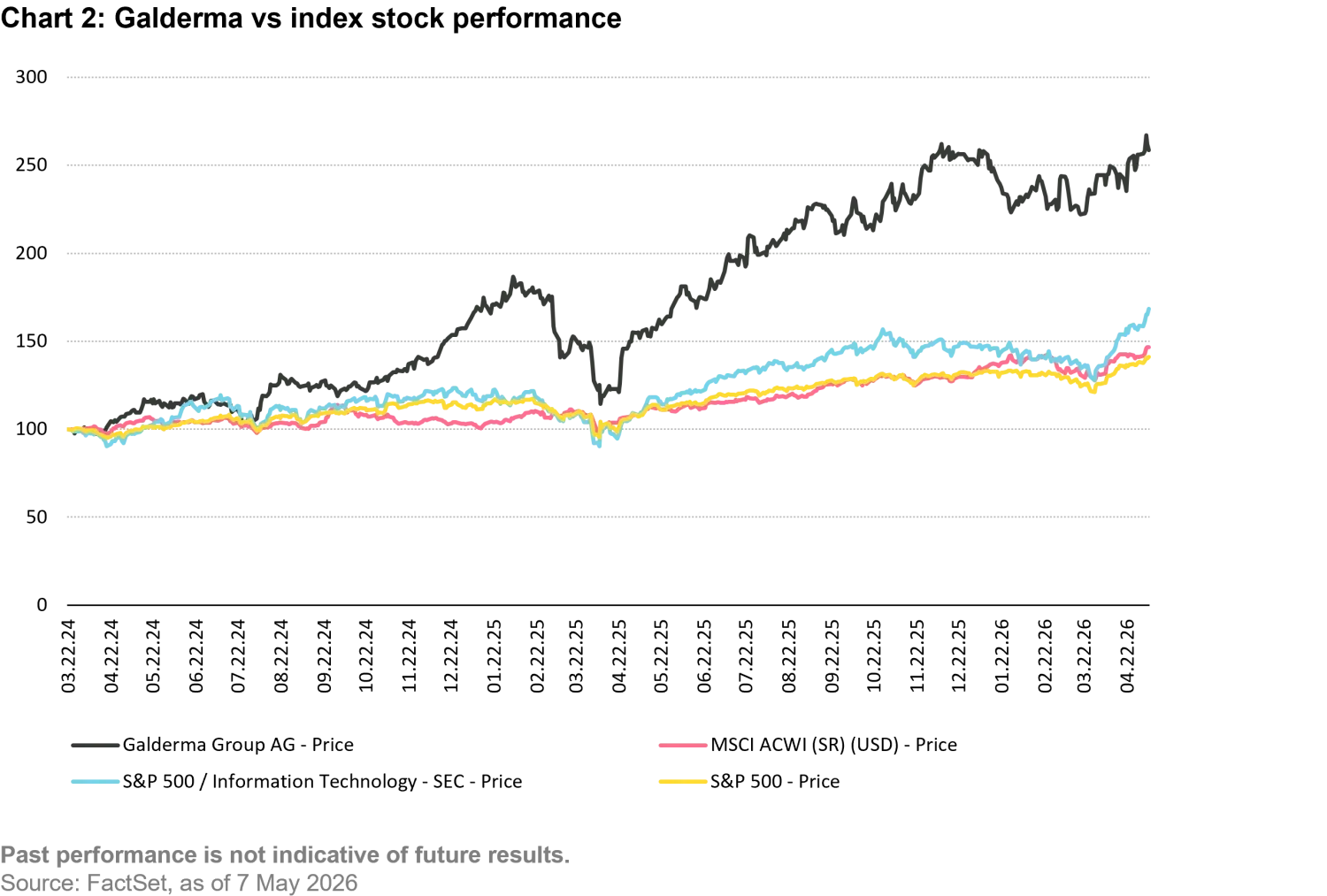

Our thesis did not rely on Nemluvio (as Nemo was named after approval) to dominate the market for severe skin conditions. Dupixent is a very good product and we expect it to remain the leader. However, for some patients, itch is the dominant feature of their disease. The market, however, is very large, and is growing quickly; if Galderma secures a share of only 10%, it would be a blockbuster. We also forecast that overall company profitability would improve as development costs declined and revenues grew. Since the IPO, the company has reported very strong results, with the aesthetic and skin care businesses growing consistently, and Nemluvio taking off. Galderma’s original guidance for Nemluvio was for a peak of $2 billion in sales. The company recently raised that to $4 billion, roughly the size of the sales of the entire company in 2023. Turns out, itch was a growth business.

The explosion of GLP-1 weight-loss drugs are an ongoing boost to Galderma’s bottom line. Drugs like Ozempic have solved one problem for millions of patients and created another. Rapid, significant weight loss deflates the face, producing what has become known as “Ozempic face.” For Galderma, the GLP-1 wave is not simply expanding an existing market, it is creating an entirely new patient population. To solve for Ozempic face, patients want fillers. A McKinsey survey of aesthetics providers found that well over half of patients seeking facial treatments had never been active cosmetic medicine users before1.

A final wrinkle, if you will: L’Oreal has come around to our way of thinking and is an owner in Galderma once again. The company that co-founded Galderma, and then sold out a dozen years ago, is now a 20% owner. We see this as a strong vote of confidence from a former owner, and from an organization that clearly knows something about skin.

In our view, Galderma has an understandable business model, category leadership, durable growth drivers, and improving economics. Nemluvio has transformed what was once a neglected symptom into a meaningful, scalable therapeutic opportunity, and its aesthetics franchise benefits from powerful secular tailwinds and expanding use cases. With multiple growth engines, we expect Galderma has a strong trajectory ahead.

Chart 1: Galderma’s evolution to a global pure-play leader

| 1947 | 1981 | 2014 | 2019 | March 2024 |

Cetaphil Invented | L'Oréal-Nestlé Joint Venture | Nestlé Acquires L'Oréal's 50% | EQT-Led Consortium Acquisition | Galderma Goes Public |

Cetaphil Gentle Skin Cleanser: original formula remains unchanged today. | Galderma formed as a 50/50 JV between L'Oréal and Nestlé | Stake Nestlé consolidates full ownership & rebrands as Nestlé Skin Health. | Nestlé Skin Health is acquired. Rebrands as Galderma; becomes the world's largest independent dermatology company. | Listed on SIX Swiss Exchange, the largest Swiss IPO since 2017 & among the largest healthcare IPOs globally. |

| Aug 2024 | Aug 2024 | FY 2024 | Dec 2024 | 2025 |

L'Oréal Returns: 10% Stake | Nemluvio® FDA Approved for PN | Record Full-Year Revenue | Nemluvio® FDA Approved for Atopic Dermatitis | L'Oréal Doubles to 20% Stake |

L'Oréal re-enters Galderma after a decade, citing aesthetics as a core strategic adjacent to its beauty business. | Galderma's first biologic, for adults with prurigo nodularis. Peak sales potential guided at $2B+. | Galderma reports $4.41B in net sales for FY2024, up 9.3% at constant currency and Core EBITDA crosses $1B for the first time in company history | Cleared for patients 12+ with atopic dermatitis, substantially expanding the ddressable market. | L'Oréal reaches 20% ownership of Galderma. L'Oréal expected to gain two board seats at the 2026 AGM. |

Source: Galderma

Important Information: References to portfolio holdings and other companies are for illustrative purposes only as of the date of publication to elaborate on the subject matter under discussion. Information provided should not be considered research or a recommendation to purchase, hold, or sell any security nor should any assumption be made as to the present or future profitability or performance of any company identified or security associated with them. There is no assurance that any securities discussed herein will remain in the portfolio at the time you receive this communication, or that securities sold have not been repurchased. Securities discussed may represent only a certain percentage of a portfolio’s holdings. Refer to the “Related Strategies/Funds” for further evaluation. Any projections or forward-looking statements regarding future events or the financial performance of countries, markets and/or investments are based on a variety of estimates and assumptions. Such information should not be regarded as an indication that Vontobel considers these forecasts to be reliable predictors of future events and they should not be relied upon as such. Actual events or results may differ materially and, as such, undue reliance should not be placed on such forward-looking information.