A Prudent Approach to Navigating Equity Markets in China

Quality Growth Boutique

China can offer an exciting and dynamic opportunity, but investors must navigate a complex regulatory environment and quickly changing competitive dynamics. At Vontobel Quality Growth, we have been investing in China for decades, long before A-shares became accessible to foreign investors. In this video, our research team sheds light on:

- Why investors should not overreact to regulatory concerns around Alibaba.

- Where to find growth opportunities: consumer leading franchises, technology and health care companies that are driven by domestic demand.

- How to address challenges in the A-share universe: shorter average track records, limited transparency, and uncertain sustainability of growth.

China A-shares Investing – The Quality Growth Approach

The first economic reforms introduced by China in the late 1970s opened up the country to new foreign investments and encouraged domestic entrepreneurship and the privatization of traditional state-owned industries. These early financial liberalizations paved the way for the eventual debut of the Shanghai and Shenzhen Stock Exchanges to facilitate capital markets access for domestic private firms and SOEs. Since 1990, and on the tails of China’s massive economic development, the public float of some 3,500 companies has flourished into a vibrant marketplace for companies across many industries—from food and beverage, to home appliances and biotech. This massive onshore equity market is valued today at more than $10 trillion.

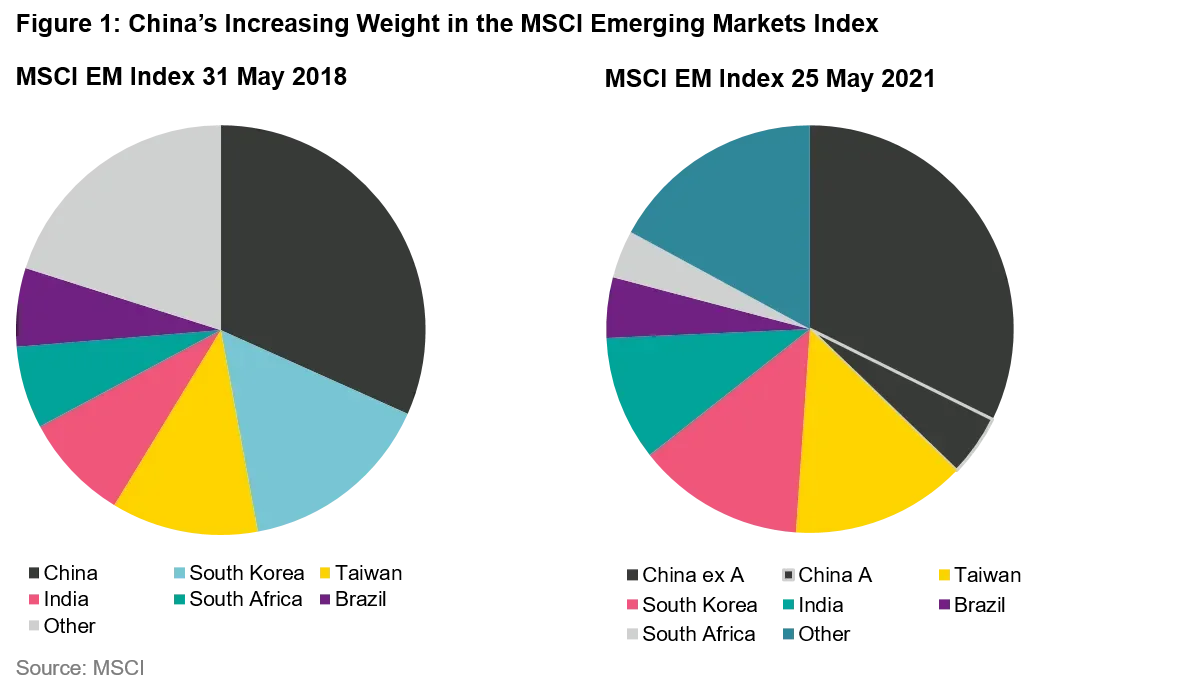

Until recently, the only way for foreign investors to access China’s booming economy was through Hong Kong-listed equities, ADRs, and multinational companies with large exposure to China. The pool of publicly-traded domestic companies, called A-shares, were out of reach given government restrictions on ownership. The turning point came in 2014, when the Hong Kong-Shanghai and Hong Kong-Shenzhen Stock Connect programs were introduced to allow foreign investor participation in the domestic market. Currently 1,500 A-shares are accessible through this program. By the time MSCI included a partial list of A-shares into its marquee emerging markets index in 2018, investing in the domestic market had gone mainstream. Moreover, China overall became a very significant part of the EM index. With a 20% inclusion of A-shares by MSCI, China’s representation in the Emerging Markets Index rose from just above 30% to more than 40%.

At Vontobel Quality Growth, we follow a benchmark-agnostic approach. This means that we judge a potential investment on its merit, without consideration for sector or country. For example, our exposure to China does not automatically grow with the MSCI EM Index weight. Our level of exposure to any sector or country is purely the result of a consistent application of bottom-up fundamental research. This paper discusses key observations and outcomes from applying our long-standing research approach to the Chinese A-shares opportunity set.

The Quality Growth Approach

The strong performance of A-shares in 2020 (MSCI China A was up 29% year-over-year in 2020 vs. MSCI EM up 16%) sparked further investor interest in Chinese mainland companies. But which ones are the high-quality companies? Will these businesses demonstrate sustainable growth?

With a clear target in mind, our search for portfolio candidates begins with a screen that filters for superior profitability and stability of returns. Then we perform deep-dive research into the screened candidates to determine if they are investable. This requires an understanding of both past and future drivers of success, and the verification of competitive advantages that can sustain future growth. The last step before initiating a position is to help ensure a reasonable valuation. We have been investing in China this way for many years via H-shares and ADRs.

Since A-shares have become accessible via the Northbound Stock Connect in 2014, our pool of investment ideas expanded. A considerable number of these new entrants have demonstrated rapid growth and improving profitability over the past few years. Yet, the number of stocks that have made the cut for our portfolios has not grown commensurately. We want to invest in businesses with predictable and sustainable growth. However, our due diligence has revealed that many A-share companies are lacking in either predictability or sustainability of growth, in our opinion.

Through our research process, we aim to gain sufficient confidence in a company’s long-term outlook. Currently, however, three common shortcomings on quality attributes weigh on our investing confidence in many A-share names:

- Limited track records relative to companies in other EM countries

- Lower transparency stemming from differing standards of disclosure and corporate access

- Uncertain sustainability of future growth

1. Limited track record

A-shares on average have shorter track records relative to companies in other EM countries.

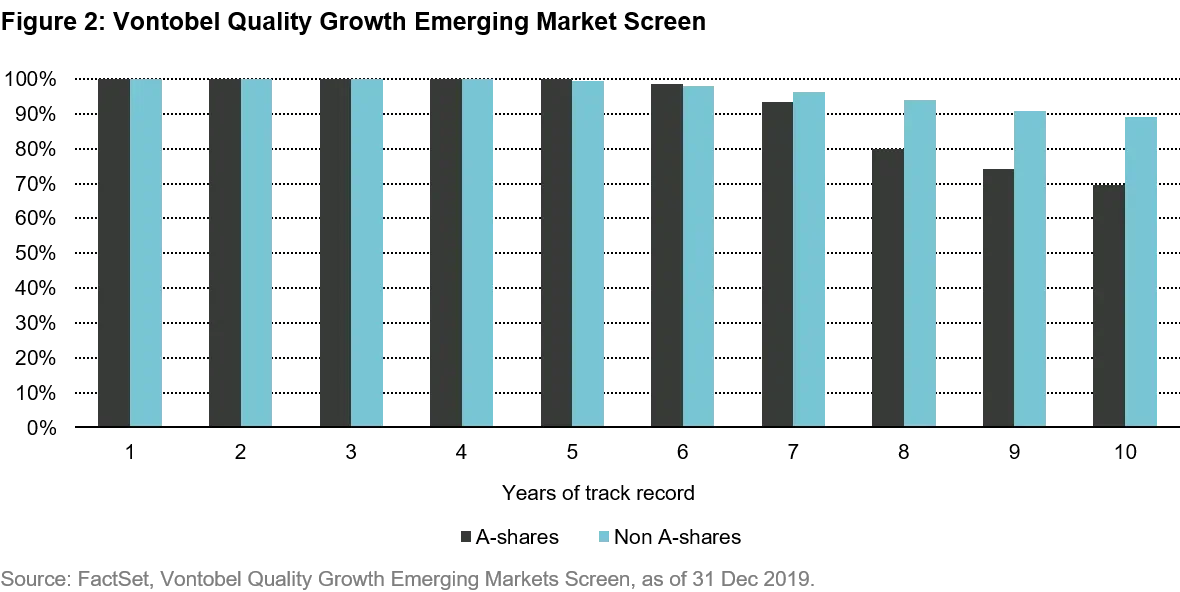

Many A-share companies are highly profitable, but have not been around for a very long time. In fact, A-share companies have a shorter track record on average than other EM companies in our screen: Only 70% of A-share companies in our quality screen have a ten-year track record vs. 90% for all other EM companies on the same screen.

For every name that we consider investable after thorough due diligence, we must have high conviction in long-term prospects. An adequate track record contributes to our confidence that the economics are solid and can be sustained. A few years of positive financial momentum is not a reliable indicator that the good performance will endure.

Track records represent and tell a story about consistency. Historical information sheds a light on the focus and competence of the management to execute a long-term strategy under varying economic conditions, regulatory challenges, and changing competitive dynamics. The track record is a vital tool for assessing corporate governance as well. For example, if a company undergoes significant related-party transactions, historical financial reports can paint a more thorough picture to validate the economic substance and appropriateness of intercompany arrangements. This is especially important for gauging whether management’s interests are aligned with minority shareholders.

A longer timeline is a valuable window into the organization’s DNA and culture. Over time, we are able to gather and piece together important information about how, for example, a company will likely navigate a complex regulatory environment or a change in competitive landscape. Past successes and even failures in operations or M&A are important markers to assess management’s capabilities and weaknesses. A clear view of the past is a better way to evaluate the veracity of management’s statements. This is not about past performance indicating future results; it is about building a body of knowledge on all the mechanisms in the organization that have led it to success. This knowledge contributes to our own confidence about prospects for success. The good news is that shorter track records tend to naturally resolve with the passage of time.

2. Poorer transparency

Transparency is limited by different norms in disclosure and corporate access.

Transparency is a key ingredient in developing a high-conviction investment thesis. Basic financial data can suffice for a straightforward business, but most companies do not fall into this category. While all A-share companies must file financial statements with mandatory disclosures, there is variability in the richness of content from company to company. Limited or complete lack of corporate access further contributes to the opacity surrounding some companies.

Access to and the ability to speak with company management or investor relations is critical. Questions that cannot be answered by publicly available data arise routinely. It is virtually impossible to understand a company’s culture or human capital strategy without speaking with people who are a part of the organization. First-hand information is important to accurately assess sustainability and stability. It is not something that can be gleaned from financial reports for many A-share companies.

Another important issue that comes from our experience with emerging market investing is that of related-party transactions. It is a particularly common occurrence with companies that are majority founder-owned. Dealings among companies that are owned by the same principal are often murky and may not be at arm’s length. While financial reports provide technical details of the transactions, it is also important to speak with management to understand the underlying economic substance of these deals. Even though a company may appear to be high quality based on historical financial data, we would not be taking our fiduciary duty seriously if we did not question management on such activity. Some of these transactions are benign, some are toxic.

Fortunately, while corporate access has been historically inconsistent among A-share companies, we have noticed broad and gradual improvements over the last few years. In the past, there were noticeably fewer resources devoted to investor relations among A-share companies, resulting in poorer communication and thus transparency. To clarify, this is not about a language barrier; we have native-language analysts on the ground who can read through all footnotes and dig deep. The issue is many A-share companies have not felt the need to engage extensively with institutional investors up to this point. Some of them did not previously understand why investors wanted to engage. From personal experience as an example, a company would send its controller to meet with investors even though the controller’s role is backward looking, while investors must look to the future as well as the past. The controller has deep insights related to the financial statements but could not discuss the company’s longer-term strategy in-depth.

As institutional participation in the Shenzhen and Shanghai stock market increases, corporates will increasingly recognize the benefits of shareholder engagement. We expect the standards of corporate access for A-share companies to improve over time.

3. Uncertain sustainability of growth

Pursuit of sustainable growth has proven to be more challenging.

After establishing that a company is high-quality by looking at its track record and the fundamentals, we need to assess the competitive environment to determine the sustainability of future growth. This is to satisfy our preference for companies that can compound earnings over a multi-year time horizon. The trajectory of growth depends heavily on the stability of an industry’s competitive environment.

We have found that competitive dynamics evolve more quickly in China due to shifting trends and regulations, thus resulting in less enduring growth. Compared to other emerging markets, China has demonstrated a relatively faster pace of change in consumer preferences and technological advancements. Some sectors that typically generate stable growth have demonstrated lower longevity of growth in China. The packaged foods industry is a good example of brands and products that were once market darlings, but lost favor as consumers traded up on the back of rising disposable income.

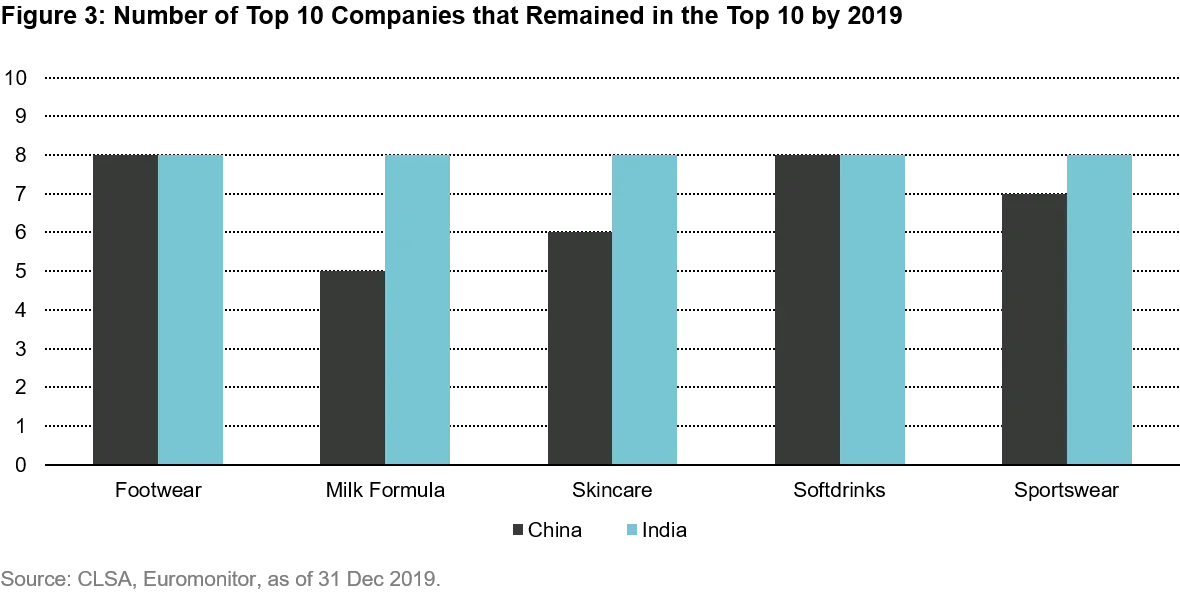

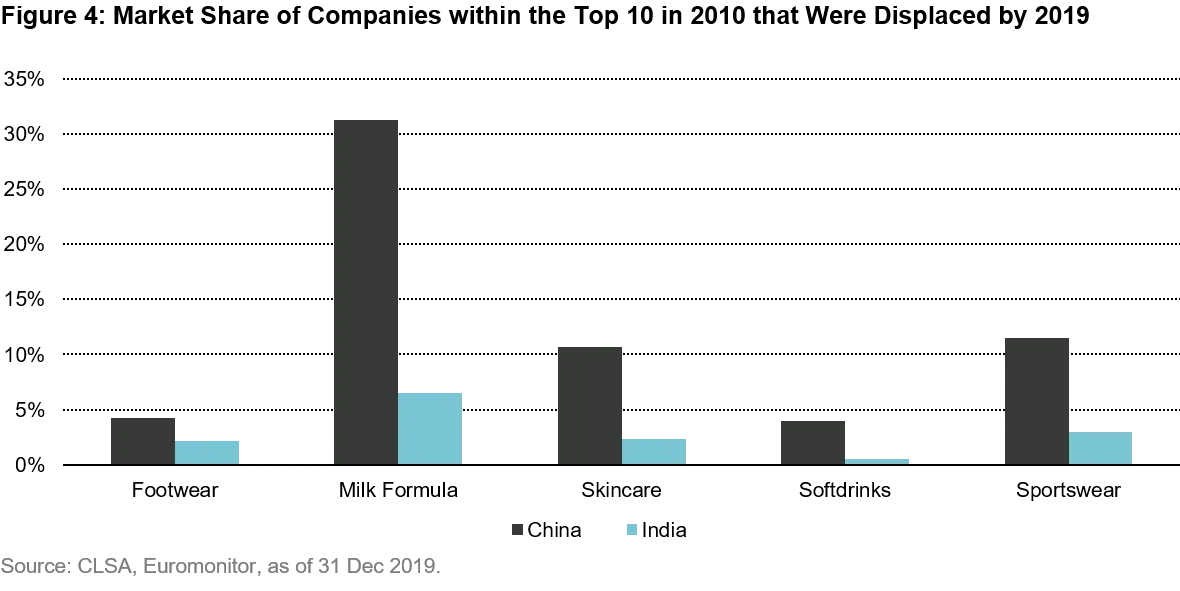

To illustrate the faster pace of change among consumer companies in China, we compared market share data for a few consumer categories in China to the same categories in India. Figure 3 demonstrates that a lower number of Chinese companies within the top 10 in 2010 had held on to market positions by 2019. Figure 4 shows us how much of the market in 2010 was represented by the top-10 companies that were displaced by 2019. It has been more difficult for leading Chinese companies to maintain their market positions over time compared to their Indian counterparts.

For a company to be considered investable, we need to verify sustainability of growth. More rapidly evolving competitive landscapes reduce the likelihood that companies can compound earnings over multiple years. True gems are harder to come by in China.

Navigating the China Opportunity

After establishing that a company is investable, valuation is a final and critical consideration. While there may be short-term gains to be had, we cannot risk our clients’ assets chasing momentum at unreasonable prices. Since we can invest globally, we are always looking for the best value-for-money among the global emerging markets opportunity set. We are currently invested in a handful of A-share companies and have, in our opinion, a well-vetted list of names on deck to start buying at sensible prices.

For instance, Netease is one of China’s most popular internet portals and a leading online gaming developer and operator. We believe it is an example of a high-quality business with good corporate governance that has maintained its leadership in China’s expanding mobile gaming and internet sectors. Another example in China is Wuliangye, one of two ultra-premium baijiu producers with the heritage and brand that can continue taking share from lower-end baijiu on the back of consumption upgrade. Baijiu as a category is expected to remain a staple since it has been a part of Chinese culture for centuries.

In addition to the deep dives performed by research analysts, our former investigative journalists help us further vet companies by speaking with stakeholders, such as former employees, suppliers, customers, and so on. The information gained helps to sculpt a more three-dimensional image of the company and often exposes risks that may not have been apparent on paper or in standard disclosures and company discourse.

In a recent example, one of our former investigative journalists based in the Hong Kong office found sources from a relevant Chinese NGO, a lawyer with industry expertise, and a representative from an industry association, to help the research analyst better understand ESG risks for an A-share company. As a result, they discovered unsustainable environmental practices by a company that otherwise possessed many traits of a high-quality business. In another example, the former journalist reached out to her contacts to confirm that a food and beverage company’s distributor relationships were more entrenched and better managed than its competitors. This helped confirm the strength of the company’s competitive moat and in this case ultimately led us to invest in the A-share company. It is important to note that these discoveries are not related to confidential information and are available to the public but just requires further digging.

Conclusion

We rely on our investment approach to help find the right companies that have a long runway of sustainable growth. By applying this research process, we have found some challenges that are more common among A-shares: shorter average track records, limited transparency, and uncertain sustainability of growth.

These challenges are not unique to A-shares, but they are more prevalent in the A-share universe. It is also important to note that just because one of the above obstacles is present, it does not immediately rule out a name as investable. But the challenges do compound when more than one of the above hurdles are in the way. In some instances, we cannot gain enough conviction in an investment case and therefore will have to keep monitoring the company until the limitations are resolved. As the issues of limited track record and transparency improve with time, the weight of A-shares may likely grow in our portfolios.

The Vontobel Quality Growth team has been investing in China for decades. Even before A-shares became accessible to foreign investors, we were on the ground learning about mainland Chinese businesses and the development of the economy. We have seen the emergence of and met many impressive entrepreneurs and high-quality companies. We believe our accumulated experience has been useful for navigating the exciting and dynamic A-shares opportunity while our disciplined approach keeps us focused on searching for the rare gems, high-quality companies with enduring profitability and growth.

Certain of the information contained in this viewpoint is based upon forward-looking statements or information, including descriptions of anticipated market changes and expectations of future activity. Adviser believes that such statements and information are based upon reasonable estimates and assumptions. However, forward-looking statements and information are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements and information.

This presentation is not an offer to sell or the solicitation to buy any security. It does not constitute a recommendation to buy or sell any security. Past performance is not necessarily indicative of future performance, future returns are not guaranteed. There is no assurance that the adviser will make any investments with the same or similar characteristics to the investment presented.

About the authors

About the authors

Topics:

Related insights

Open vs. closed models: Cheap intelligence and the economics of the AI buildout

Quality investing: focus on predictable and resilient growth

China Luxury: Green shoots or a structural shift?

Waiting for the “fat pitch”: Lessons from the 2026 Berkshire Hathaway Annual Meeting

Silicon is the new oil: Why the AI compute cycle still has runway