Dealing with ESG controversy: The Philippines

Fixed Income Boutique

When investors consider ESG as part of their investment process it most often involves companies, but underlying each company there is a country, a sovereign. How a country is governed dictates how companies can operate. Therefore, country-level ESG analysis should be part of any investment manager’s thinking.

As an emerging market debt manager specializing in hard-currency sovereign debt, the country is at the core of our analysis. While ESG investing has become more regimented and clearly defined in recent years, when it comes to emerging market debt, it should always be a key part of an investor’s investment process. In particular the “G” (the “governance”) plays a big part.

Many investors use exclusion criteria when deciding where to invest. This means closing the door to countries or issuers that do not meet predefined ESG screening criteria. While exclusion is a valid strategy, it excludes the countries or issuers that are progressing in improving their ESG credentials. In my view, it is the laggards who are on their way to leaders that should be rewarded and encouraged. But what happens when a country takes a stumble in ESG? How should an active investor act and what should they do in such a case?

To give an example of this, let’s review a negative ESG case and how an EM sovereign investor should act in such an event.

Controversies elevate governance risk

The spread of the coronavirus is a global event and countries across the world have each had to make decisions as to how they react. An out-of-control pandemic can wreak havoc on a nation’s economy, affecting logistics, employment, trade, etc. In its approach to tackling Covid-19, the Philippines, a major EM economy with a population of nearly 110 million, has not fared well.

Sustainalytics, a company that ranks countries and companies based on their ESG, gave a “high” ranking to the Philippines for “controversy exposure”. This increase in risk classification was due to the government’s mismanagement of the corona crisis compared to its ASEAN neighbors, resulting in a challenging medical situation and a higher economic impact on the country.

Since the incumbent president, Rodrigo Duterte, took office on June 30 2016, his domestic policy has focused on combating the illegal drug trade by initiating a controversial war on drugs, crime, and corruption while supporting extrajudicial killings of alleged drug users and other criminals. As of October 2020, the war on drugs has resulted in 5’800 deaths and 256’000 arrests of suspects in the drug trade. Since his election in 2016, Duterte’s war on drugs policies has resulted in widespread criticism, including from the UN and Amnesty International.

According to MSCI, from a governance point of view, the country is perceived to be at medium risk regarding the level of democracy and press freedom, and at high risk regarding rule of law and corruption.

Pre-covid starting point

Pre-COVID-19, the Philippines economy was growing at around 6% annually (Worldbank) with a below-global-median public debt burden of 42% in terms of the country’s GDP (global median is 47%*).

Whilst the focus of the government (or rather the president) was the war on drugs, (according to the World Bank), significant reforms such as the “Ease of Doing Business Law” and “Rice Tariffication Law” plus changes focused on poverty reduction and public infrastructure investment sustained the economic growth trajectory.

The ESG credit impact of controversies

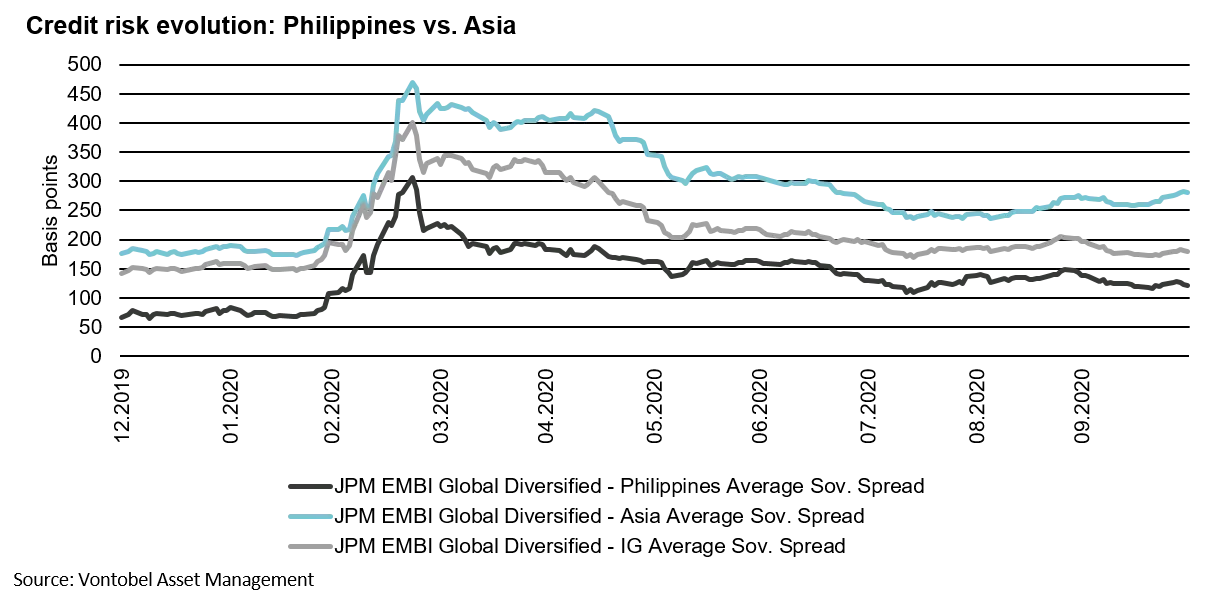

As yet, both the handling of the pandemic as well as the president’s rule of the country, which often appears to be autocratic, have not had a meaningful impact on the market’s perception of the credit risk of outstanding government bonds (in hard currency) compared to both investment-grade peers as well as peers in Asia (as can be seen in the chart below).

We feel there is a significant risk that the lack of action on pandemic prevention and medical care may have an impact on the economy and, therefore, result in downward pressure on the country’s traded debt.

Outlook

While these controversies remain unsolved, we believe the country’s current stance leaves little room for tactical investment opportunities as bond prices do not account for the ESG risks that have been exacerbated by the pandemic and also seem to neglect the authoritarian leadership of President Rodrigo Duterte.

Elections in May 2022 could offer some opportunities though. The Philippines remains a country with potential for bond investors, however, it wouldn’t hurt if the next government were to take steps that show a willingness to move towards more sustainable governance. This would improve their ESG standing, improve conditions for the Philippine people and, as a result, help provide a foundation of sustainable long-term growth and thus attract investors.

*MSCI, Sustainalytics, as of 30.10.2020.

About the author

Read next:

Five reasons to invest in China’s A-SharesRelated insights

Five reasons to invest in China’s A-Shares

Summiting “Peak Growth Mountain” – what you need for the descent