Multi Asset Boutique

Fundamental strategies to protect and grow investors’ assets in their chosen markets.

In the middle of last week, it seemed as if the “most anticipated recession of all time” was truly history. The US yield curve, which had been inverted for more than two years, had begun to “un-invert” again. By Wednesday, July 31, the curve was the least inverted since July 2022.1

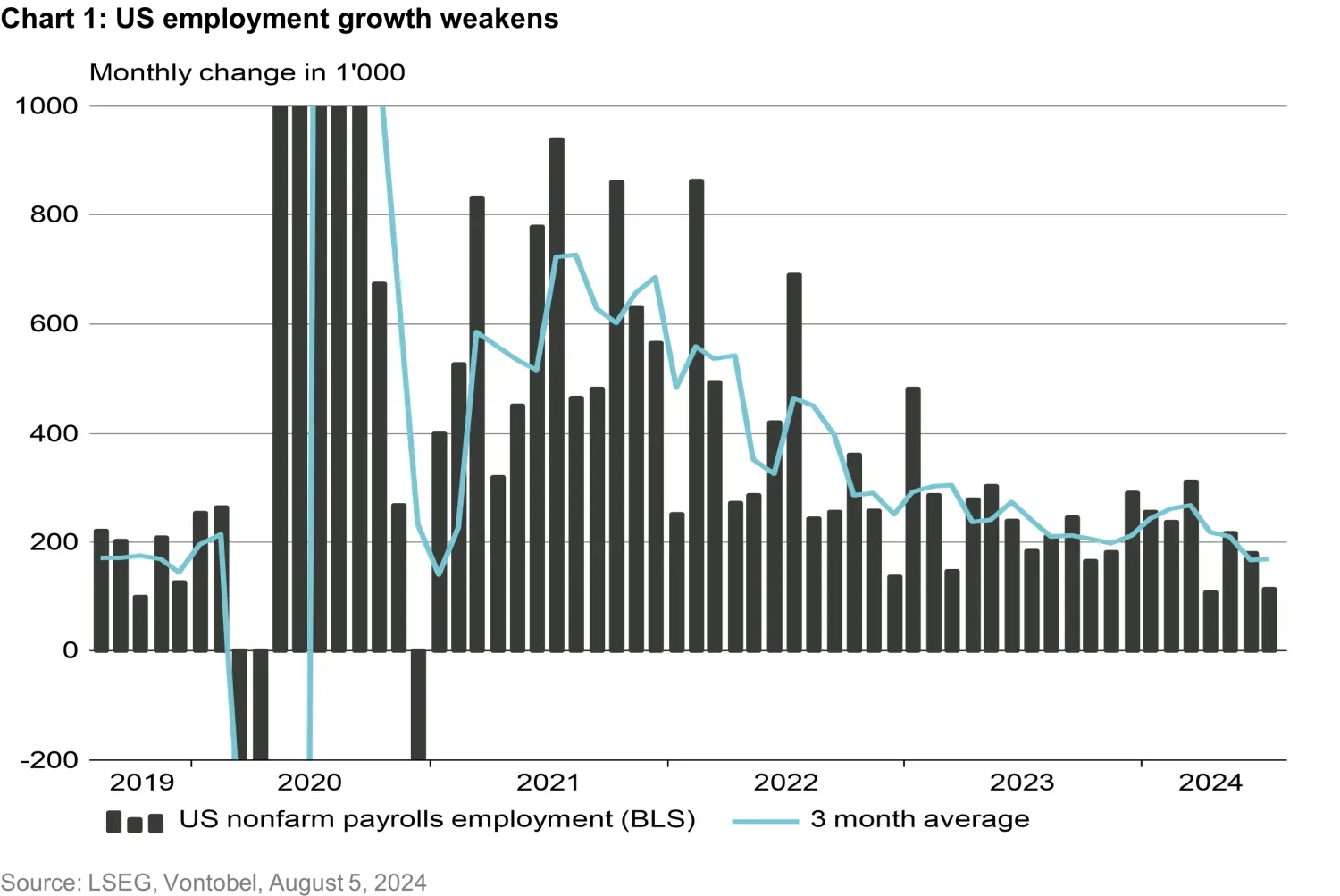

Just two days later, the tide turned: Friday’s US employment report showed that only 114,000 jobs were created in July (chart 1). This was well below the 175,000 jobs expected. Moreover, the data for June and May were revised downwards (from 206,000 to 179,000, and from 218,000 to 216,000 respectively). The unemployment rate also raised eyebrows, rising from 4.1 percent to 4.3 percent.

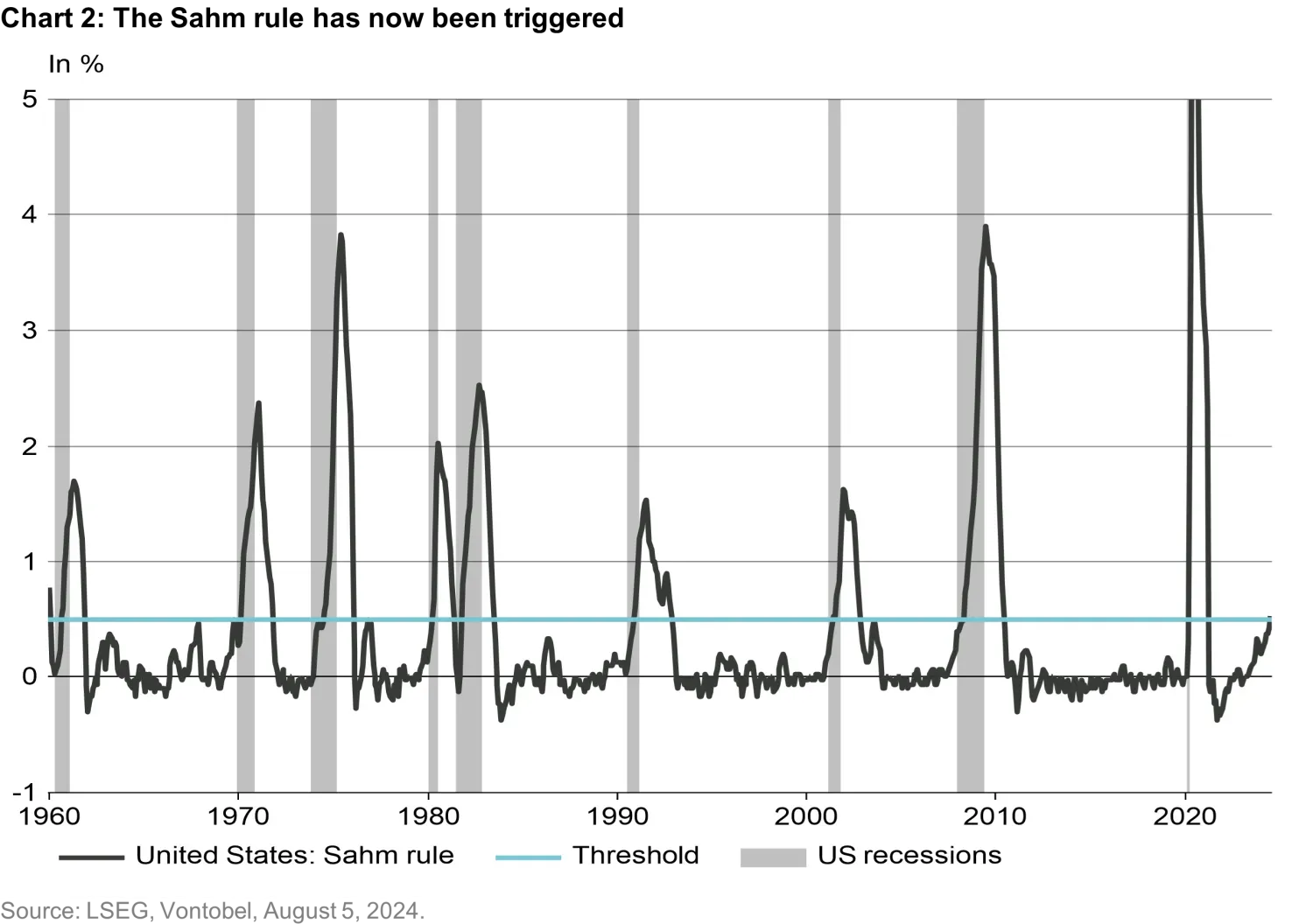

As a result, the “Sahm recession indicator”, coined by the American economist Claudia Sahm, also sounded the alarm (chart 2). The Sahm indicator is considered a fairly reliable recession indicator. It is triggered when the three-month moving average of the US unemployment rate rises by 50 basis points from a 12-month low.

While the official verdict is still out – the National Bureau of Economic Research uses a variety of criteria to decide whether the US economy is in recession or not – market participants already seem to be assuming that the Federal Reserve (Fed) is “behind the curve”. In other words, they believe that the Fed failed to cut interest rates in time and is now unable to stop the impending economic downturn.

Weak employment data, combined with other poor economic data, the Bank of Japan’s surprise interest-rate hike, and disappointing quarterly results from some technology companies, led to considerable volatility in the markets. Investors sold shares and fled to “safe havens” such as bonds, gold, the Swiss franc, and the yen.

However, following the publication of positive economic data (e.g., ISM survey for the US service industry) and reassuring comments from some monetary policymakers, the markets staged a (partial) recovery rally on Monday, August 5.

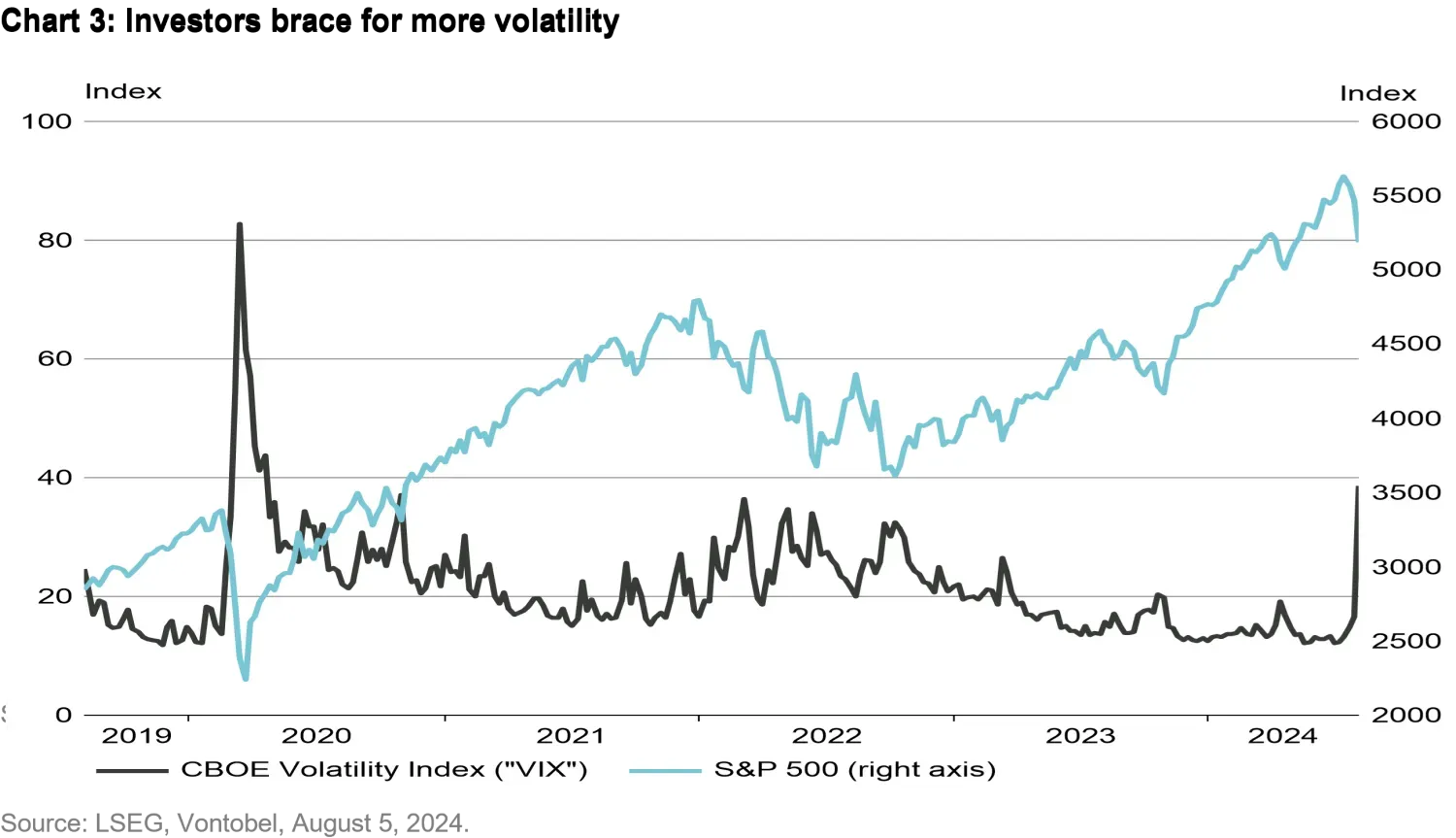

The so-called VIX index, which measures the market’s expected volatility for the S&P 500 over a 30-day period, exceeded 65 points intraday on August 5, and closed at just under 40 points (chart 3).

Our Investment Committee is currently slightly overweight in equities, with a preference for select quality stocks. We acknowledge that this slight overweight is not ideal in the current environment, as further setbacks cannot be ruled out in the short to medium term.

However, we believe the rest of the portfolio is well positioned in the current environment: We have been overweight in “safe havens”, such as government bonds and gold, for some time. The overweight in emerging-market bonds in hard currency has also benefited from last week’s bond rally. We are underweight in high-yield and investment-grade bonds.

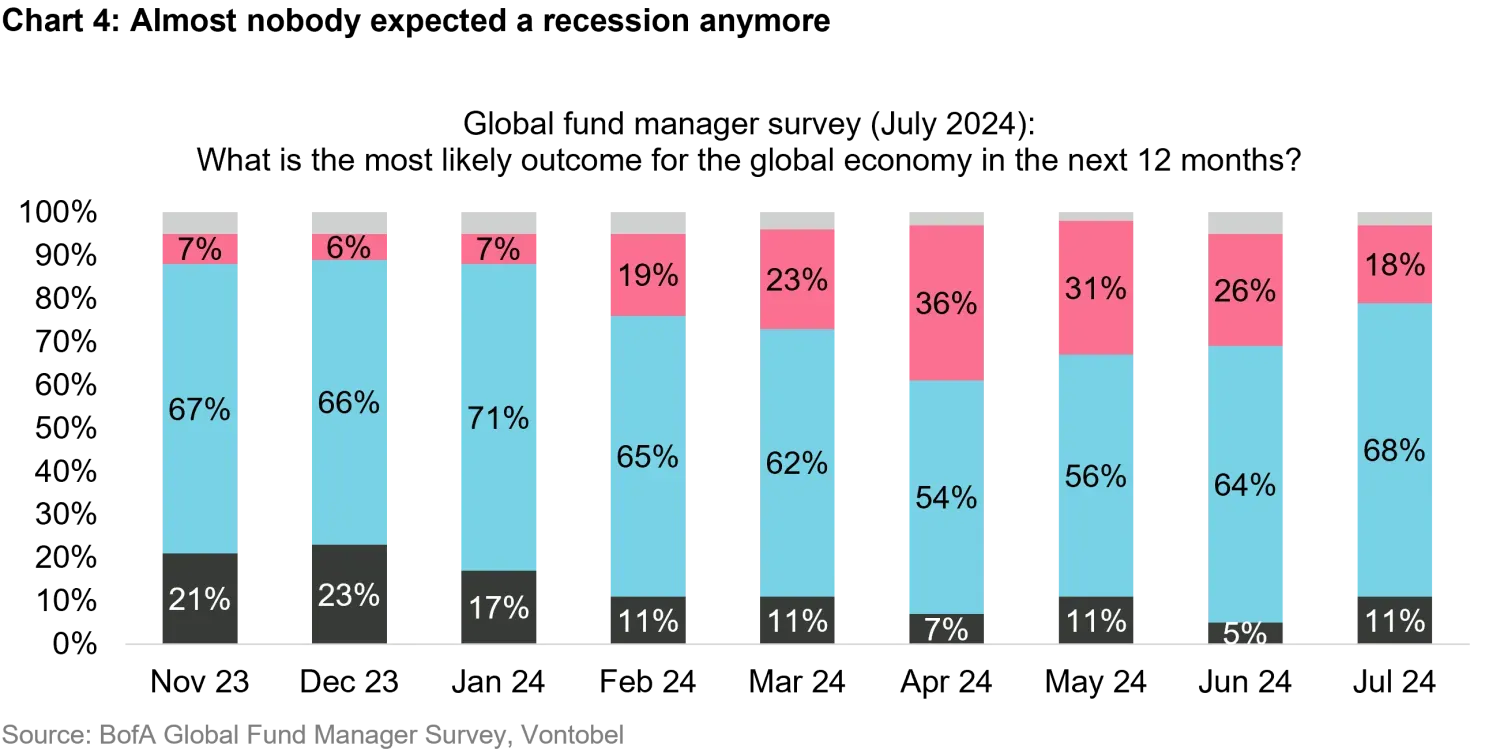

We have repeatedly pointed out in the past that we believe the markets to be overly optimistic about the US economy. This is reflected, for example, in Bank of America’s Global Fund Manager Survey, according to which the majority of respondents (68 percent) expect a “soft landing” of the economy, i.e., a return of inflation to the Fed’s 2 percent target without a recession (chart 4).

A recession remains part of our economic base-case scenario for 2024, but we expect it to be a short and shallow one.

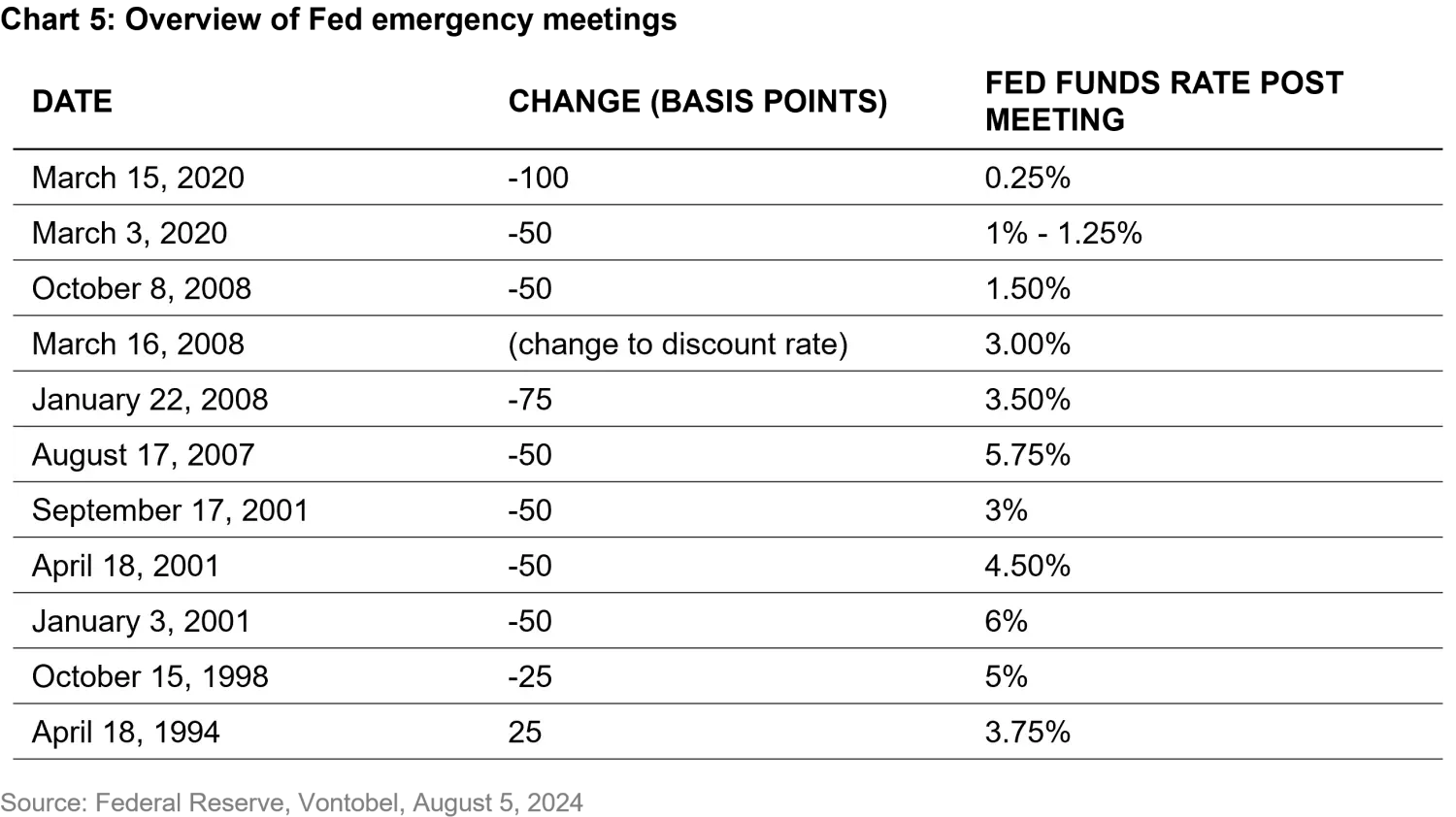

In our view, the latest developments increase the pressure on the Fed to act. As their next official meeting is not scheduled until 17-18 September, calls for an unscheduled Fed meeting (and an “emergency rate cut”) are growing louder. Such moves are rare, but possible.

Since 1994, the Fed has held a total of eleven emergency meetings, most recently in March 2020, when it lowered the US key interest rate by 100 basis points (chart 5).

After weighing all the factors we deem relevant, we stick to our current positioning. For long-term investors, we see the recent sell-off as more of an opportunity to buy shares selectively.

We will continue to monitor the situation closely and adjust our positioning as necessary.

1. With an inverted yield curve, short-term debt instruments offer higher yields than their long-term counterparts. This usually indicates a lack of confidence in future economic development.