US Gets Political on ESG and Proxy Voting

Quality Growth Boutique

Investors are already inundated with ESG brochures each marketing the “ideal” approach. A myriad of approaches, processes and measures are marketed under this shared acronym. Unlike the market’s other favorite acronyms, BRIC and FANG, ESG has a lot of room for individual interpretation in both meaning and application. We had expected to hear from the Securities and Exchange Commission to provide some guideposts for investors. What we got instead was two proposals from the Department of Labor (DOL). Why the DOL? It regulates the massive $10+ trillion1 in employee benefit plans covered under ERISA (Employee Retirement Income Security Act).

Individually, each of the two proposals seems to offer solid investor-first logic for the fiduciaries that run these plans. The first looks to provide rails around what the plans can hold in ESG-themed funds, while reiterating its ban on sacrificing returns for other goals. The second aims to limit proxy voting when it doesn’t benefit performance, in order to save costs.

But taken together, there appears to be an ulterior motive. Both proposals point to a potential government action to reduce active stewardship by owners, framed as maximizing returns to savers.

It is a fluid situation. It appears to us the government may be sensitive to social or environmental special interest groups having undue influence on companies. This influence could be exercised by leveraging the financial muscle of the funds under ERISA. In a market economy, regulators have a role that influences the balance of power between stakeholders. And it appears they are exercising some of that influence.

Any structural change to the balance brings the risk of unintended consequences. We are concerned that returns-focused active stewardship could get pushed back in the process. In our view, active stewardship that includes deep research, including on ESG issues, combined with engagement and voting acts as a guardrail to protect value. It’s common sense. If you rented out an apartment you owned, and didn’t visit it for 10 years, what are the chances it would hold its value relative to one that’s checked and maintained regularly?

We think it is important to recognize that the connection between investors, the choices made by company managements, and a range of real-world consequences works more effectively for savers over the long term with active management. To us, this is the true purpose, power and benefit of ESG.

Proposed New Investment Duties Rule2

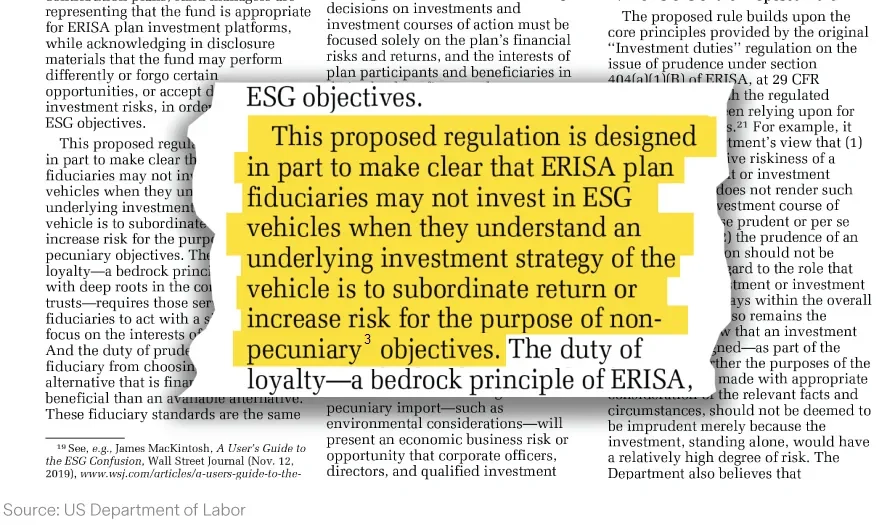

A quote summarizing the goals taken from the Federal Register.

This rule covers both funds and direct investments held by the plans. The main three areas the proposal focuses on:

- Do not give up return for non-financial goals. ERISA rules already ban sacrificing returns for social policy goals4. We see this reiteration aimed primarily at Impact and Socially Responsible Investing (SRI) – which the rule bundles under ESG. These approaches contrast the long-term, returns-focused goal we associate with ESG.

- Reduce investor confusion from the proliferation of ESG choices. The rules point to the inconsistencies of processes followed by ESG funds, as well as those of ESG scores between providers5 such as MSCI and Sustainalytics. It’s challenging to see how this goal will be achieved purely on a forecast returns-based criteria. The rules mention investments should match the plan’s investment objectives, but provides no specifics.

- Higher Fees. The proposal mentions a study by the United Nations PRI6 that pointed out that passive funds that purchase duplicate data to construct ESG indices will face higher costs, and perhaps ultimately higher fees. Well done Sherlock. The point could be argued that a marginal increase in already very low costs of passively managed funds, is still a bargain (even if it’s supported by stewardship free-riding). It seems counterintuitive to suggest savers would be better off over the long-term dropping a bias towards higher quality just to save a few basis points.

We are not sure how the DOL will grapple with investor confusion and higher fees given the lack of specifics in the proposed rule. One additional feature in the proposed rule was that plans offered as a default option for participants that don’t actively choose their holdings, are not allowed to include ESG-themed funds. They can be offered however, in a fund line-up where participants choose their holdings, as long as they are invested based on ‘objective risk-return criteria’.

Proxy voting and exercises of other shareholder rights (proposed)7

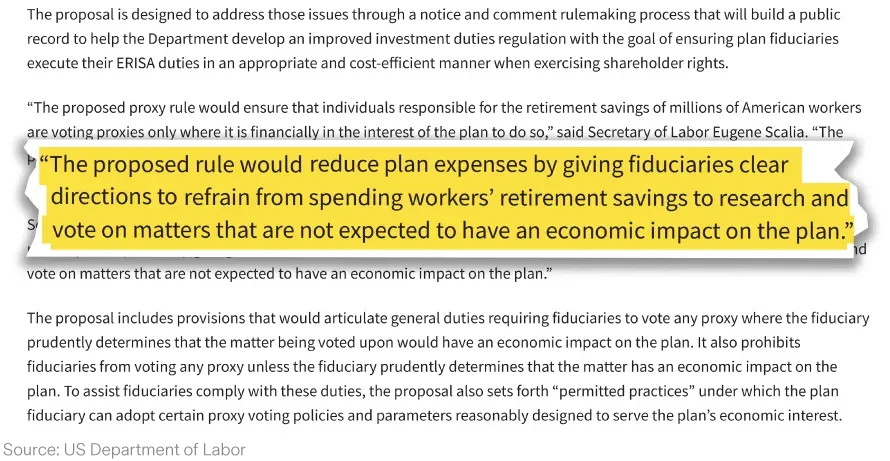

A quote from acting Assistant Secretary of the Department’s Employee Benefits Security Administration Jeanne Klinefelter Wilson from the press release:

This rule focuses on equity held directly by plans, and not on funds. The DOL estimated the value of these assets at $2.1 trillion in 2017 – a fraction of the total covered by ERISA, but still equal to the value of the $1.2 trillion the Norwegian Government Pension Fund Global and $950 billion China Investment Corporation, the world’s largest sovereign wealth funds8, combined.

This rule puzzles us. The proposal follows the same direction as the Investment Duties proposal (the ESG rule), framed as a way to improve returns. The rule suggests returns can benefit from saving time and money by not analyzing or participating in votes that will not economically impact the plan. The first thought that comes to mind from practice is by the time someone has figured out if a vote is valuable or not, most of the work is already done.

Still, the DOL ran a back of the envelope cost analysis of how much could be saved, which they estimate at $540 million a year -- a big number. Although, relative to a $2.1 trillion asset base it’s a guestimated 2.3 basis point saving. Savings would not be evenly spread, with larger plans likely to save less relative to assets.

The DOL is asking for comments on suggested short cuts that can be implemented to save time and money. These include a cap on when a holding falls below a level worth voting on. They have suggested this could be 5% of plan assets! Not analyzing the votes or participating on a stock that accounts for 4.9% of a portfolio would not seem sensible to us – not to mention that a 5% investment in a single stock could be seen as aggressive weighting. A minimum level does make sense. But at a relatively low absolute dollar value not a proportion of plan assets. After all, the costs are absolute.

Beyond the cap, another idea the DOL threw in is to create policies that establish when voting would be restricted. Their suggestions of what a policy could contain include in effect automatically voting yes to management’s recommendations on subjects without significant economic impact for the plan. Another is to not participate on non-binding votes. They suggest votes that would not bring economic value include uncontested director elections and the ratification of third party auditors. These suggestions strike us as an under appreciation of the importance directors play in steering an organization, or the message presented in non-binding votes such as say on pay. Why would corporate savers in an ERISA plan not support a vote against egregious pay to their CEO – especially if the CEO is also chair of a board has not taken on a truly independent member for years? We hope these specific suggestions do not carry through.

What concerns us about this rule is that it focuses on costs that can be saved from the physical process of research and voting. But does not acknowledge, or attempt to value, an offset in the long term values from reduced ownership oversight.

Risks

In general, we anticipate a lot of the impact of these rules, if they become final, will hinge on how they are interpreted.

Regarding the ESG rule - what distinguishes between the benefit from a long-term investment in risk reduction, from an expense? Insurance premiums that can roll over for decades are generally regarded as sensible business expenses. The same logic holds for a number of ESG risks.

A way to illustrate this is thinking of ESG as similar to good health. You need to look after your health to perform at full potential. Say you twist an ankle and ignore it, chances are your ankle swells up. If you continue to ignore it could become a serious problem. ESG shares these bookend conditions - structural problems and chronic ailments.

An example of an old structural problem that has turned chronic is decades of cognitive bias that has resulted in lack of U.S. boardroom diversity. An example of structural risks still compounding but not yet chronic is climate change. Dealing preemptively with structural issues are harder to quantify than dealing with chronic problems – but not less important. Would investments into climate change related risk reduction be treated as a benefit or sacrifice to returns for plan holders?

Lets consider a manufacturing plant exposed to flooding if climate change continued to worsen. If they invest in relocating the plant, that would not lead to an immediate increase in profits, that could have happened if they invested in marketing instead. The benefit would come from reduced disruption risk. Generally speaking we would argue a significant reduction in risk has value. But it’s hard to justify quantitatively given uncertainties such as timing or the local effects of climate change.

What if the effect of these rules is that plan managers avoid ESG altogether? A further concern is whether ERISA fiduciaries will become nervous in their ability to justify an ESG investment and choose to avoid rather than embrace the material benefits we believe this approach can bring. ERISA can impose heavy penalties for breaches of their rules – so it’s a serious consideration.

A risk from the proposed voting rule is the unintended consequence withdrawing votes from a large aggregate stake in companies. A company’s shares maybe held in relatively small weights across a range of plans, but the aggregate across the ERISA pool could account for a significant stake in a company.

In conclusion, we appreciate there is a pressure for the government through one agency or another to corral the rapid rise in ESG assets and help investors avoid mistakes. We recognize a principals-based approach offers more flexibility than the prescriptive route followed by the Europeans with the EU Action Plan (that deals with ESG). But in this case the clarity of how these rules will be interpreted is poor, and their construct leaves us suspicious of the underlying role politics may be playing.

ESG as a practical investment tool is about paying attention to risks and getting ahead of them in the real world. We think active stewardship is an approach the government should support, as we believe it will add significant value to savers over the long run.

1. The aggregate value of ERISA plan assets are not published to our knowledge. The Investment Company Institute calculates 401(k) plans alone held $6.4 trillion with a further $3.5 trillion in private sector direct benefit plans as of year-end 2019. Within this value ERISA plans held $2.1 trillion of equity directly in 2017 according to the Department of Labor, Federal Register Vol. 85, No. 173.

2. www.govinfo.gov/content/pkg/FR-2020-06-30/pdf/2020-13705.pdf

3. Pecuniary – DOL defintion ‘a factor that has a material effect on the risk and/or return of an investment based on appropriate investment horizons consistent with the plan’s investment objectives and the funding policy established pursuant to section 402(a)(1) of ERISA’

4. DOL Field Assistance Bulletin 2018-01

5. MIT – Aggregate Confusion: The Divergence of ESG Ratings, August 2019

6. How Can A Passive Investor Be A Responsible Investor? www.unpri.org/download?ac=6729

7. www.govinfo.gov/content/pkg/FR-2020-09-04/pdf/2020-19472.pdf

8. Source: SWF Institute, September 2020

Related insights

Open vs. closed models: Cheap intelligence and the economics of the AI buildout

Quality investing: focus on predictable and resilient growth

China Luxury: Green shoots or a structural shift?

Waiting for the “fat pitch”: Lessons from the 2026 Berkshire Hathaway Annual Meeting

Silicon is the new oil: Why the AI compute cycle still has runway