Quality Growth

Global equities specialists since 1984. We provide a boutique investment experience for institutional and intermediary clients around the world.

For years, the semiconductor industry was marked by extreme cyclicality and mediocre profitability, driven by fast-evolving chip technology and fierce competition. During ordinary fluctuations in supply and demand, earnings would disappear entirely as chipmakers would implement large price cuts. Simply put, the industry’s growth did not translate to attractive returns on capital.

But over the past decade, a number of transformative changes have taken place. More specifically, semiconductor demand has diversified as the continued digitization of our broader economy has brought about new end-markets. Meanwhile, suppliers have become more disciplined due to rising technological complexity and consolidation. As a result, while the industry will remain a cyclical one, we believe it has entered a new phase of growth, one that is characterized by higher profitability and lower earnings volatility.

About semiconductors

What makes the internet high-speed, a phone smart or many other consumer products from autos to air conditioners safer and more efficient? Semiconductor chips.

Chips serve as the nerve center for virtually all electronic products, from regulating electric flows to processing, storing and transmitting data. While most people can name the constituents of FAANG (Facebook, Amazon, Apple, Netflix, Google) as the tech leaders of our age, semiconductor firms are often overlooked, behind-the-scenes operators, but every bit as critical to the 21st century digital economy.

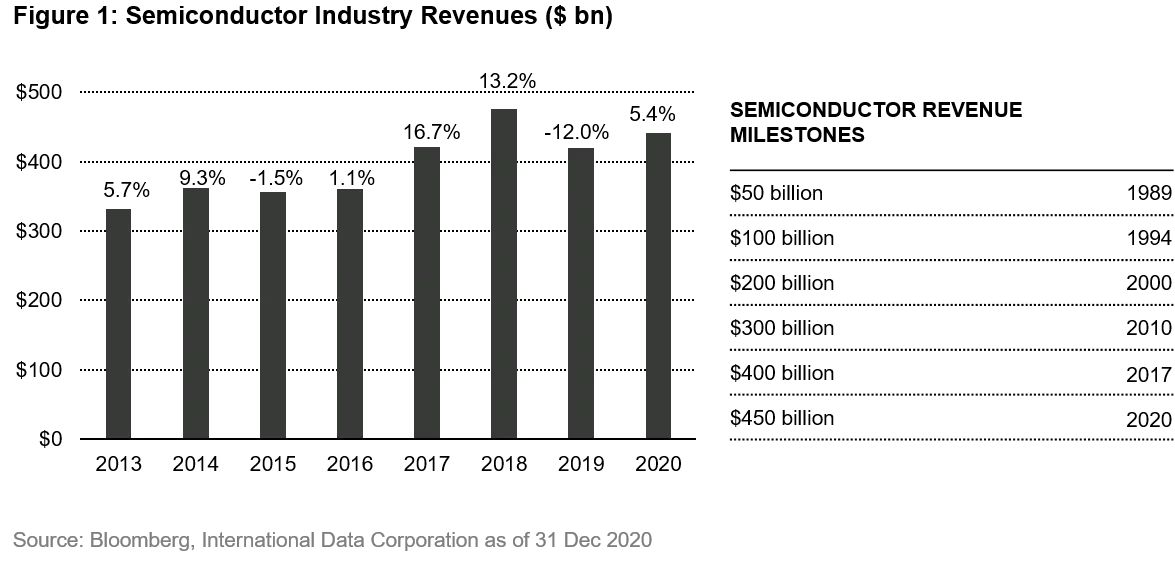

Without chips, even seemingly mundane tasks like sending emails, creating spreadsheets, and running Google searches would not be possible. Semiconductors are also at the heart of emerging technologies, including artificial intelligence (AI), Internet of Things (IoT), quantum computing, advanced wireless networks (5G) and much more. Such dynamics appear to make semiconductors a compelling growth story for investors. In fact, global semiconductor revenues have historically grown at more than double the rate of global GDP, propelling it to the $450 billion industry it is today.

Early Days: A fiercely competitive and cyclical industry

From the late 1990s through the early-2010s, the industry’s relatively low entry barriers paired with the boom in consumer electronics led to an influx of new entrants. But profits were modest: When chip supply exploded, fierce competition lowered chipmakers’ bargaining power. Consequently, much of the chip volume growth was offset by pricing pressure. Any manufacturing cost savings were necessarily passed onto consumers. Given these industry dynamics, semiconductors’ returns on capital were hardly spectacular. In fact, from 1997 to 2012, every semiconductor segment except for the microprocessor and fabless sub-segments were unable to generate any meaningful economic profits.

The boom-and-bust cycles of semiconductors are legendary. When times were good, chipmakers often had trouble keeping up with demand and needed to invest into building more production capacity. But lacking long-term order visibility, chipmakers would often overestimate demand and overspend on capacity additions. Making matters worse, this excess production would not get absorbed by the market, and instead led to inventory build-up. Given the fast-evolving nature of chip technology, those focused on leading-edge technology were forced to cut prices aggressively, as they faced the risk of inventory becoming obsolete when newer technologies hit the market.

This Catch-22 can be seen at play in memory chips, a sub-segment of the market that is considered the most cyclical. During the 2008 financial crisis, PC makers started to cut orders for DRAM, a specific type of chip that stores data in memory cells. DRAM suppliers reacted by aggressively cutting prices to unload as much product as possible in order to convert inventories into cash. This caused DRAM prices to collapse, resulting in a 50% decline in revenues.

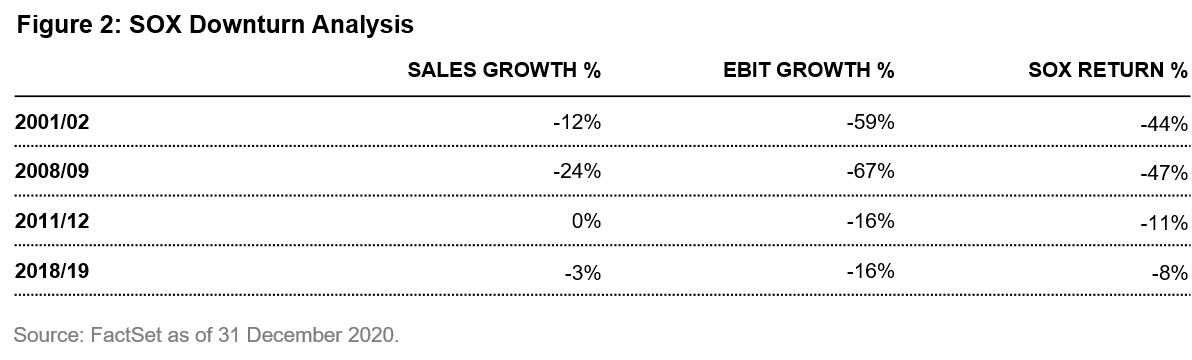

Moreover, semiconductor businesses tend to have a significant fixed-cost base, which amplifies the earnings impact during down cycles. In order to stay competitive and keep up with ever-changing product innovations, chipmakers must make significant research & development investments during good times and bad times. Moreover, in the past, many chipmakers operated in-house fabrication plants; therefore, manufacturing costs were largely fixed regardless of capacity utilization. This meant that fluctuations in revenues could disproportionately impact earnings, a phenomenon very clearly demonstrated in previous industry down cycles (Figure 2). Most notably, during the 2008 – 2009 global financial crisis, the constituents of the SOX Index (a cap-weighted index of 30 semiconductor companies), experienced a 24% sales decline, yet operating income fell 67%. Unsurprisingly, shareholders suffered a negative 47% return during that downturn.

A new normal – higher profitability and lower volatility?

In recent years, a handful of semiconductor outfits have delivered less volatile earnings growth, as well as higher returns on capital. Certain segments of the industry have even started to demonstrate oligopolistic behavior. Are these results sustainable? We believe the answer is yes – the industry’s demand has seen a diversification into more attractive end-markets, and supply has become structurally more disciplined amidst the rising technological complexity and consolidation.

Broadening of end-demand

From the 1990s to 2010, the growth engine of the semiconductor industry was the consumer electronics (CE) end-market, which fed more than 55% of the industry’s revenues by 2009. Consumer electronics tend to have short product lifecycles (up to 18 months) as consumers upgrade frequently. Each generation of devices brought about newer and faster technology, making it critical for channels to clear out old inventory before new products were launched. This caused frequent and pronounced cycles for chipmakers, as they would not think twice about cutting prices.

Nowadays, however, much of the industry’s growth is powered by the rising semiconductor content in non-consumer end markets including autos, industrials, communication equipment and data centers. For example, the average semiconductor cost per car has more than tripled from $150 to $475 over the past two decades, driven by the continued push towards electrification and automation in vehicles. Moreover, we are only at the beginning of our transition to an increasingly data-centric economy. Estimates show that the amount of data we will create over the next three years will likely exceed the cumulative data created over the past three decades. Our need for data centers and cloud infrastructure services will only continue to grow, benefitting computing semiconductors (e.g. GPU, ASIC) and memory chips. In fact, the server end market has already surpassed PCs as a percentage of memory DRAM shipments, accounting for one-third of the demand compared to 10-15% several years ago.

These shifts have resulted in the CE share of industry revenues falling below 50% over the past four years. The obvious implication is that the end demand has become more diversified, thus reducing the impact of CE product cycles on industry revenues. These new B2B end-markets are also higher margin customers. The chip cost often makes up just a tiny part of the total production cost (low bill-of-materials). As a result, customers tend to be less price sensitive, allowing chipmakers to earn a higher margin. Lastly, non-consumer end markets have longer product cycles and rely less on the latest technologies. For example, Analog and Microcontroller devices sold today often utilize technologies that were already available several years ago. During demand downturns, these chipmakers are therefore more willing to keep prices stable and hold onto inventory, ultimately reducing sales volatility.

Consolidation

Globally, there has been over $350 billion in semiconductor M&A deal volume from 2015-2020, more than five times the preceding six years. Notably, deal activity reaccelerated in the second half of 2020 and skewed towards large-scale acquisitions, with announcements including NVIDIA (for ARM), Analog Devices (for Maxim), and AMD (for Xilinx). This acceleration in M&A in conjunction with the absence of new entrants has led to significant consolidation within the industry. The total number of US semiconductor companies has dropped from 110 in 2001 to just 60 in 2020, opening the doors to a more favorable competitive environment.

To illustrate this further, we examine the evolution of the DRAM memory industry. DRAM was originally invented by IBM and Intel in the 1960s-70s, and then massively fabricated by more than 30 newcomers through the 1980s-90s. Due to industry fragmentation, DRAM chipmakers would focus mainly on gaining market share. During demand down cycles, all players would slash prices and dump inventory into the market.

Today, the industry has consolidated down to three key players: Samsung Electronics, SK Hynix, and Micron, which contribute over 95% of the global DRAM supply. More notably, the consolidation has led to a change in behavior. Each player has demonstrated more capex discipline, underpinning a steady rise in profitability. During the last memory down cycle in 2019, the three memory players responded early with meaningful capex cuts and carried more inventory despite the short-term demand hiccup. In fact, DRAM industry operating margins troughed at low-30% level in 2019, a marked improvement over earlier downturns in 2008-09 and 2011-12 when the sector saw negative profitability.

Rising technological complexity and the limitations of Moore’s law

Alongside the emergence of new applications, the complexity and costs associated with designing and manufacturing chips have grown dramatically. The roadmap for innovation in the semiconductor industry during the last 50 years has been “Moore’s Law,” which says that every two years the number of transistors (building blocks of chips) per square millimeter should double, also known as shrink.

The increasing transistor density led to smaller, faster, and cheaper chips that accelerated the adoption of semiconductors across industries. To put this into perspective, the best chips in 1965 had transistors that were 6,000 nanometers wide with over 100,000 transistors. The latest Apple M1 chip, manufactured by Taiwan Semiconductor Manufacturing Company (TSMC), has transistors that are just 5nm wide (10,000 times thinner than a human hair) with 16 billion transistors.

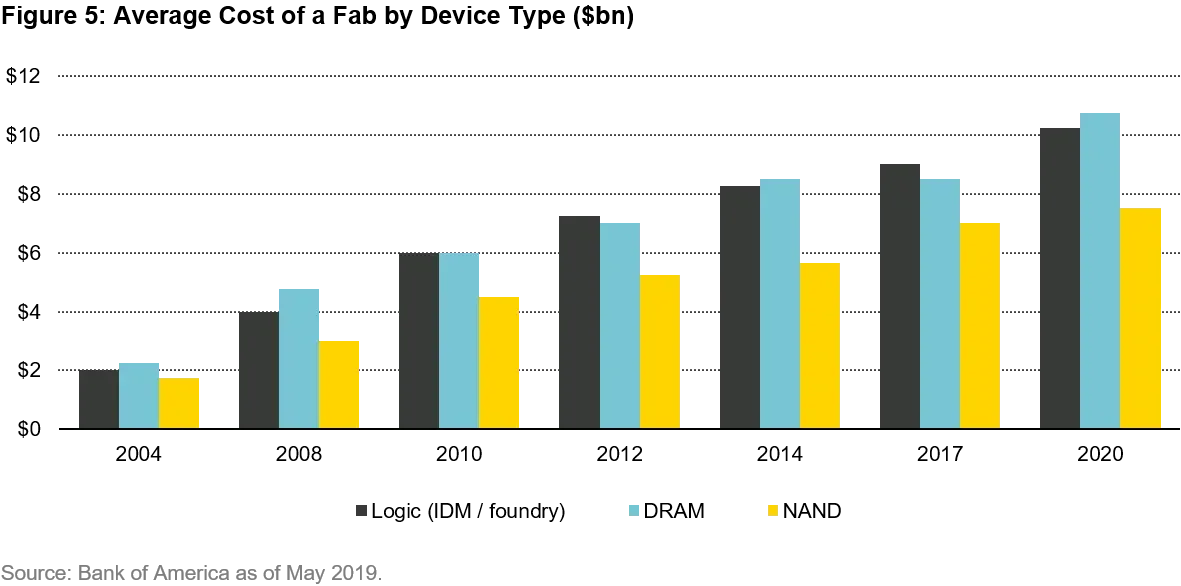

But now we have started to approach the limits of Moore’s law. The incremental manufacturing improvements have become far more complex and expensive to pursue, driving up the capital intensity of chipmakers. The capital investment required to build a leading-edge fabrication plant has grown more than 5-fold from $2 billion in the early 2000s, to around $10-15 billion today. In fact, global semiconductor companies collectively spent about $100 billion in 2020 on capital expenditures, equivalent to 20-25% of revenues. Meanwhile, chip design costs have also skyrocketed. The US semiconductor industry now spends an average 17% of revenues on R&D, second only to the pharmaceutical and biotechnology industry. Thus, the barriers to entry keep increasing.

Last but not least, incremental cost reductions are shrinking. Transistor unit costs, which previously declined by 20-30% per annum based on Moore’s Law, have started to come down more slowly and non-linearly since around 2013. In other words, the industry is facing a flattening cost curve, which has created a fundamental change in chipmakers’ capital allocation decisions. We expect more constrained supply growth going forward, driven by more disciplined capex and limited shrink-led supply growth. This will have a favorable impact on the industry’s cyclicality, as the less frequent periods of overspending and excess capacity will create a solid backdrop for more resilient through-cycle pricing.

Conclusion: The new normal

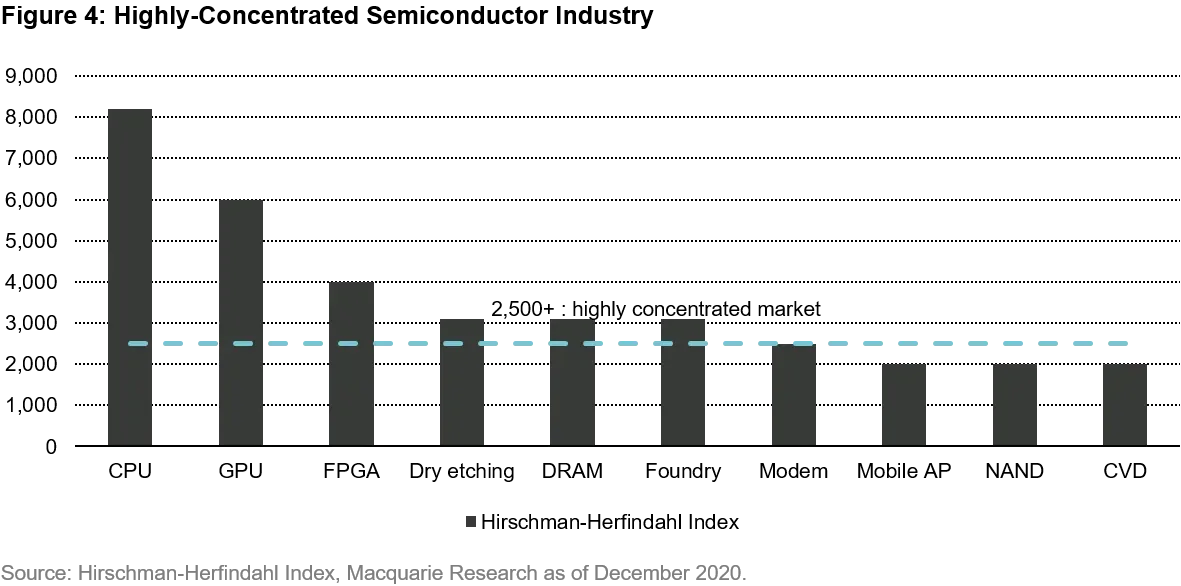

There was a time when semiconductor cycles whipsawed investors on a routine basis. While cyclicality will remain to some degree, we believe that the industry has entered a new phase, characterized by long-term secular tailwinds, more rational competition, and higher profitability. In fact, certain sub-segments like microprocessors, GPUs, semiconductor capital equipment, memory, and foundries have already evolved into attractive oligopolistic markets with high barriers to entry.

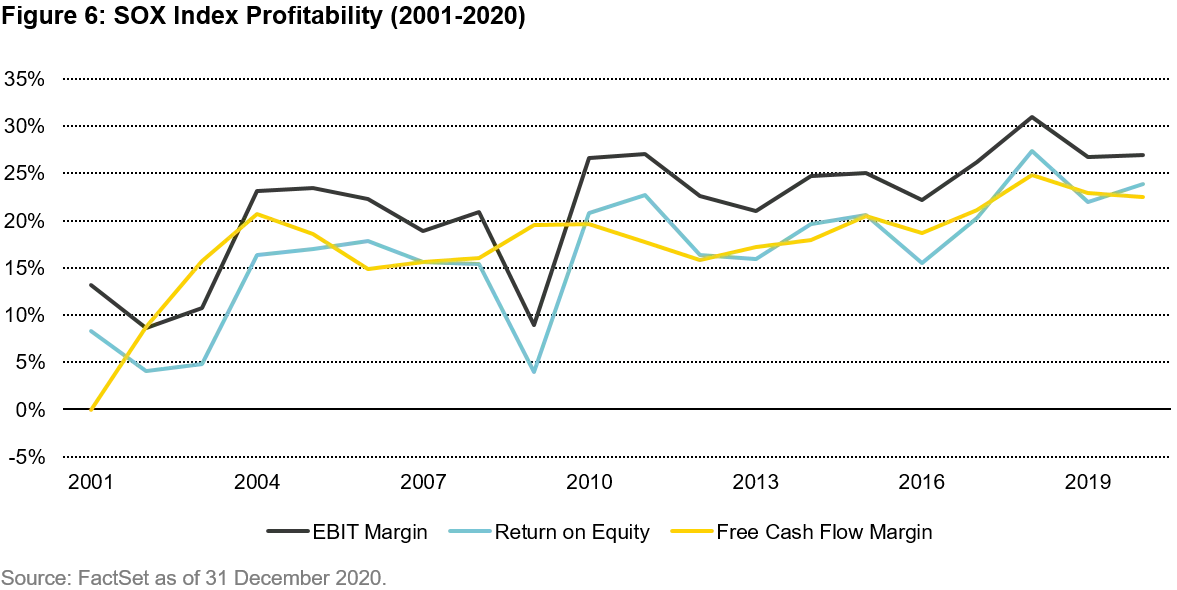

The financial impact of the structural changes occurring in the industry is already becoming apparent. The constituents of the SOX generated an average 20% return on equity over the past decade, nearly double that of the preceding decade, all while maintaining low leverage. Margins and free cash flow generation also climbed, while earnings volatility nearly halved. Even in a year like 2020, amidst negative global GDP and corporate earnings growth, semiconductors delivered positive earnings growth of 11%. We believe these strong fundamentals create a favorable backdrop for long-term investors to identify quality growth companies in the semiconductor space.

Any investments discussed are for illustrative purposes only and there is no assurance that the adviser will make any investments with the same or similar characteristics as any investments presented. The investments are presented for discussion purposes only and are not a reliable indicator of the performance or investment profile of any composite or client account. Further, the reader should not assume that any investments identified were or will be profitable or that any investment recommendations or that investment decisions we make in the future will be profitable.

Certain of the information contained in this whitepaper is based upon forward-looking statements, information and opinions, including descriptions of anticipated market changes and expectations of future activity. VAMUS believes that such statements, information, and opinions are based upon reasonable estimates and assumptions. However, forward-looking statements, information and opinions are inherently uncertain and actual events or results may differ materially from those reflected in the forward-looking statements. Therefore, undue reliance should not be placed on such forward-looking statements, information and opinions.