Quality Growth

Global equities specialists since 1984. We provide a boutique investment experience for institutional and intermediary clients around the world.

When asked to describe their approach to investing, Buffett’s brilliant partner Charlie Munger famously remarked that the approach was “simple, but not easy.” After nearly 40 years of investing, I have come to more fully appreciate the wisdom of Munger’s words. When I first started out in the asset management business in the early 1980s, and first “discovered” the writings of Warren Buffett, I almost felt that I had happened upon the Holy Grail. Buffett‘s idea of buying good quality companies at prices comfortably below their INTRINSIC VALUE seemed logical, and it was intellectually appealing because it implied that the “true” absolute worth of a security could be determined. In doing so, one could truly INVEST, not just speculate.

Many years later, I listen disdainfully as so many investors allege to know the intrinsic value of such large numbers of stocks in their portfolios. The term “intrinsic value” is thrown around so loosely. Maybe I have become jaded and cynical, but one thing I have found after examining thousands of companies over time is that there are many challenges in trying to determine what the “true” value of a company is.

Yet despite these challenges, getting valuation at least approximately right is as important as it has ever been, but we strain to see how the ever-higher grinding market environment we are witnessing is acknowledging this reality. The 8 points below outline just a few of those intellectual challenges with respect to valuation.

Lastly, I want to make a comment about portfolio construction, although again not the direct focus of individual stock valuation. Let’s start off with a question: “Have you ever seen one sentence written or any words spoken by two of the world’s most brilliant investors, Buffett and Munger, about “portfolio optimization“? I haven’t. But I have seen plenty of words written by “Modern Portfolio Theory“ (not to be confused with Modern Monetary Theory!) advocates from the Chicago School and their acolytes which rely on the concept of “beta” as a measure of risk . Beta, of course, is a measure of a stock’s VOLATILITY in relation to the overall market. Without getting into a long discussion here, suffice to say that Buffett has a lot to say about why beta is an inappropriate measure of risk. I prefer Buffett’s definition of risk as “the permanent loss of capital”, and typical “portfolio optimization” approaches that we see others often employing does not speak to this more proper definition.

I could go on and list even more challenges that go into “making the sausage,” that is, trying to truly invest in asset prices that can be pretty confidently determined, but while I am on a rant, let me now turn to a few of the challenges that the BUSINESS of investment management presents that can further muddy the waters.

Most institutions that give money to investment firms to manage have already made an asset allocation decision a priori that they want their funds to be pretty fully invested in stocks at all times. This precludes the use of cash as a residual if the money manager can find few attractively valued stocks that meet the criteria of his investment approach. During asset bubbles and times of very high stock valuations, this may result in the investment manager feeling the pressure of having to invest in the least relatively OVERVALUED stocks, rather than the best quality UNDERVALUED stocks he/she can find. When Buffett could find little of value in the frothy stock market of the late sixties, Buffett simply dissolved his partnership and returned the capital to his investors, rather than engage in such foolish endeavors. Most institutional investors today would be very reluctant to return assets to the client and forfeit their fees on said assets even IF a fully priced equity market precluded them from executing their investment approach in the desired fashion. Is there any surprise then that bubbles develop in the stock market when so much pressure is on asset managers to play what is predominantly a RELATIVE valuation game?

Investment styles can go in and out of favor for years. Studies have been done that show even investors with the very best historical track records can be out of favor and underperform for many years in a row. As clients’ patience wears thin and assets under management continue to erode, the investment manager comes under what the famed investor Jeremy Grantham describes as “existential pressure”: the fear of losing one’s job and being fired. The pressure builds on the manager to capitulate, to dilute his investment style or valuation discipline. I can personally relate to such pressure having had zero exposure to technology in the US fund in 1999 during the dot com bubble when tech came to constitute 40% of the market capitalization of the S&P. Even Buffett was derided on the cover of Barron’s magazine at that time for having “lost it.” (Déjà vu? Buffett is once again being mocked by the “champion” of the no-commissions, free-trading Robinhood platform crowd by one David Portnoy, who recently remarked, “There’s nobody who can argue that Warren Buffett is better at the stock market than I am right now. I am better than he is. That’s a fact.” We’ll see how THAT plays out!) At times like that, it is tempting to just go with the flow and compromise one’s investment discipline because it appears that(those famous words) “this time is different.”

This point is a corollary to the previous point: it is rare to meet a true LONG TERM client (fortunately for us, after years of match making we do have a few). Most clients afford an investment manger a three-year window, at best, after which if underperformance persists, the manager is fired and replaced. (A somewhat ironic point is that the poorer performing manager that is more likely to sooner than later start performing better, if nothing is truly broken in their approach, is replaced with a freshly hot performing manager who is less likely to sustain their current streak indefinitely and perhaps enter their own cooler performing period). But clients do have their OWN job security to worry about, after all, so changes must always be made. There is a potential mismatch though between the investor’s long time horizon when evaluating a company’s future business prospects and the client’s much shorter business time horizon. This is yet another factor that may pressure the manager to compromise his investment style and valuations just for the purpose of staying alive and staying in business. An investor like Buffett has the benefit of permanent “captive” capital with which to invest, unlike most professional money managers. Thus the more patient the investor AND the client, the better, whatever the investment vehicle structure may be.

Due to many of the factors alluded to above, such as having to reckon with unpredictable macro phenomena, the difficulty in precisely determining a security’s “intrinsic value” and more, investing has often been referred to as being part science and part art. Books have been written titled “The ART of Investing” because in the end, every investment decision is ultimately an EVALUATION. Although most investment approaches are organized, logical and systematic, the end product, the purchase decision, can never have as much certainty attached to its outcome as would a mathematical proof. Hence, Buffett’s observation that valuation (the intrinsic value of a security) is an APPROXIMATION and his advice that the investor should stay well within his “circle of competence” and be aware of what is and isn’t knowable enough when contemplating any company’s future business prospects. It is INDEED a humbling business.

At Vontobel we are not without tools in our arsenal to help us navigate the often clouded and uncertain investment terrain, which includes the many realities and inherent challenges we have outlined above. We believe we have a SENSIBLE investment paradigm, heavily influenced by our many trips to Omaha over the years. Our approach seeks out better quality, more predictable businesses with strong financials, which gives us a reasonable shot at knowing what a company will look like beyond today. We don’t try to fool ourselves into thinking that we can make forecasts that last for an entire business lifetime, but for at least the next five years of our investment horizon.

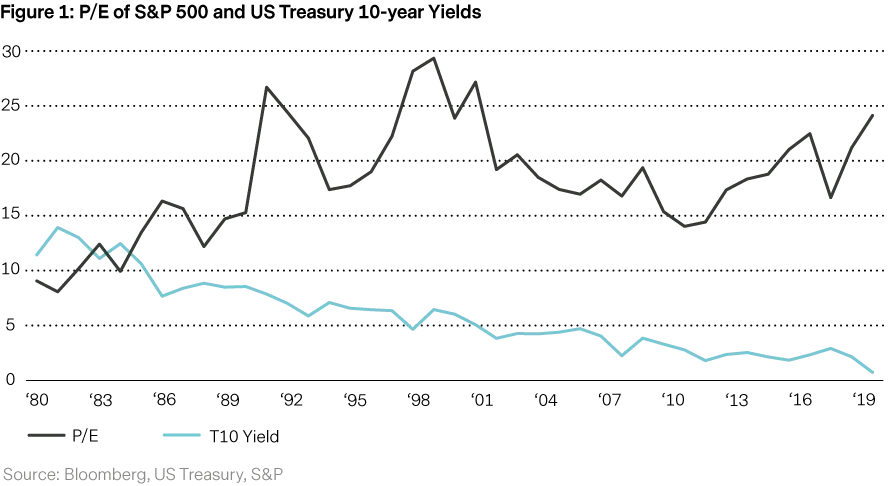

To protect us against some of the possible negative unknowns that may arise along the way, we employ a conservative method in computing the fair values of our stocks, such as using a discount rate well above the market rate when doing our present value calculations. (In contrast, some of today’s most aggressive equity investors seem willing to assume that today’s extremely low levels of interest rates will persist indefinitely into the future, thus rationalizing what, in fact, could be high levels of current valuation. In doing so, they also appear willing to make the furthest reaching predictions that fixed income managers struggle to navigate about a completely unknowable future interest rate and inflation environment).

We have a large team of tenured analysts and portfolio managers with many years of experience in the business. And in this business, because each investment outcome is probabilistic, an evaluation, the EXPERIENCE that comes from looking at thousands of prior “case studies” over the years, matters a lot. We are also a global team, capable of analyzing and comparing similar industries across borders. So while fully agreeing with Mr. Munger that solid investment analysis is not easy, it is not impossible, and armed with some of the tools described above, we believe that we have a good chance to help add value by doing that which is POSSIBLE.