Quantitative Investments

Your partner for leading quantitative investment solutions.

For many multi-asset investors gold has been a constant asset in their portfolio. And rightly so: gold has many beneficial characteristics such as adding diversification to investor portfolios and providing a hedge against global shocks. However, gold can also have its caveats: contrary to common wisdom, it falls short as a hedge against inflation.

In this article we argue that multi asset investors should look beyond investing solely in gold and also consider getting exposure to a broader basket of commodities. And this is because while both gold and broader commodities are strong diversifiers to a traditional equity/bond portfolio, broader commodity baskets are a better hedge against inflation, a concern that’s top of mind for investors these days. Both gold and broader basket of commodities do a good job as a hedge against geopolitical shocks. Gold tends to work better for generic shocks, while broader commodities tend to do better if the shock has an impact on energy supplies, like we’ve seen at the onset of the Russia-Ukraine crisis.

Furthermore, by investing in a broader basket of commodities, a much wider opportunity presents itself. We wrote as much in our last Quanta Byte. While the last decade marked the longest drawdown for commodities, the asset class has the potential for a major upswing in the next decade, due to the confluence of a number of key macroeconomic factors, which we discussed in our previous Quanta Byte.

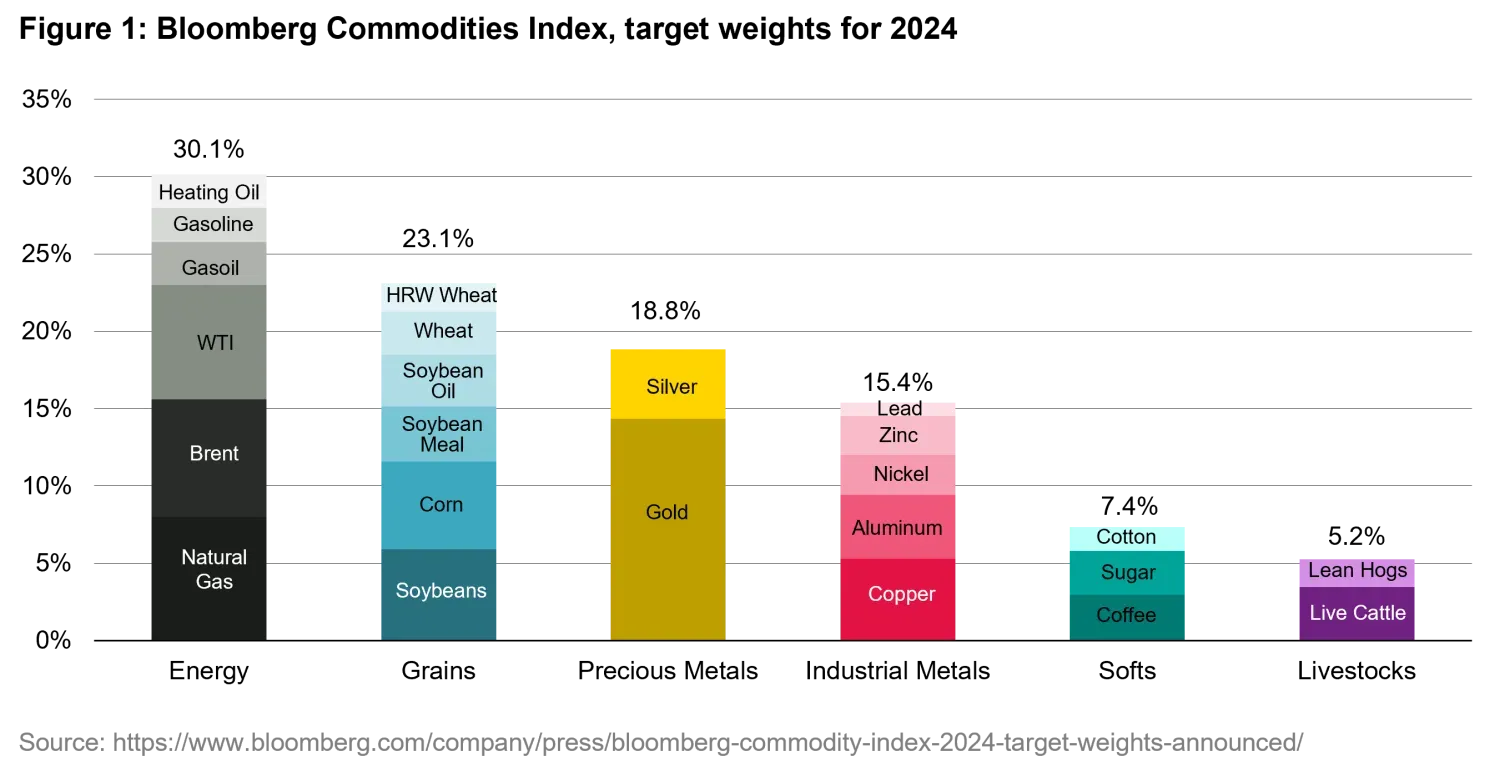

Figure 1 shows the composition of the Bloomberg Commodity Index (BCOM), which is the widely accepted standard for commodities, with index weights grouped by the six underlying sectors. The index is made of 24 distinct assets, including hard commodities like metals and oil, and soft commodities like agricultural products and livestock, such as wheat, coffee, and beef. Within this larger basket, the supply and demand dynamics that affect prices and performance vary significantly, and do not necessarily correlate to one another. For example, natural gas prices are mostly dependent on US weather, while oil prices are driven by global economic growth and OPEC supply policy. Base metals are closely connected to the Chinese credit cycle, while precious metals correlate with monetary policy. Grains and softs on the other hand depend on regional weather regimes. For example, West Africa is relevant for cocoa, while Russia, Ukraine, and the U.S. are important for wheat; for soybeans and corn, South America is the focus.

Due to the large quantity of various drivers, a broad basket of commodities is already diversified in and of itself in comparison to gold on a stand-alone basis.

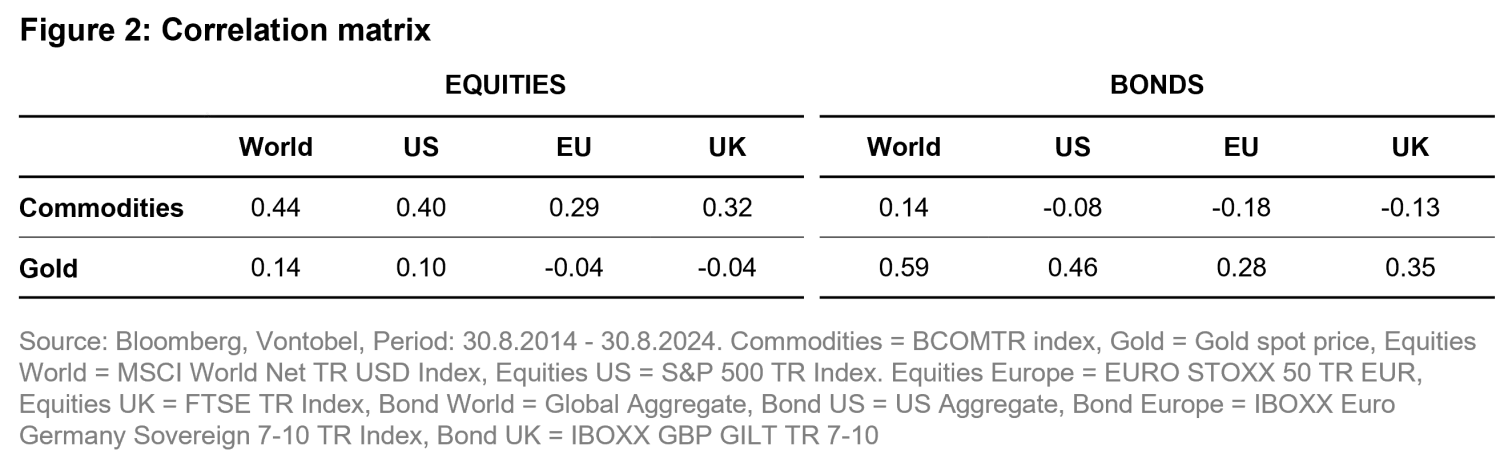

Figure 2 shows the correlation of commodities and gold to common equity and bond indices over the last ten years. When looking at diversification benefits within a multi asset portfolio, both gold and commodities show low correlations to traditional asset classes. While at the margin commodities correlate more with equities and gold with bonds, these effects neutralize versus a traditional 60 / 40 portfolio made of equities and bonds.

The positive correlation between commodities and equities stems from the fact that both are connected to the business cycle. Gold however has a nearly inconsequential correlation to equities but a positive correlation to bonds. This is because both are safe-haven assets. By combining gold and broader commodities these effects neutralize, in the sense that, as a pair, gold and broader commodities do not exhibit any correlation with the traditional asset classes, while, taken individually, they do.

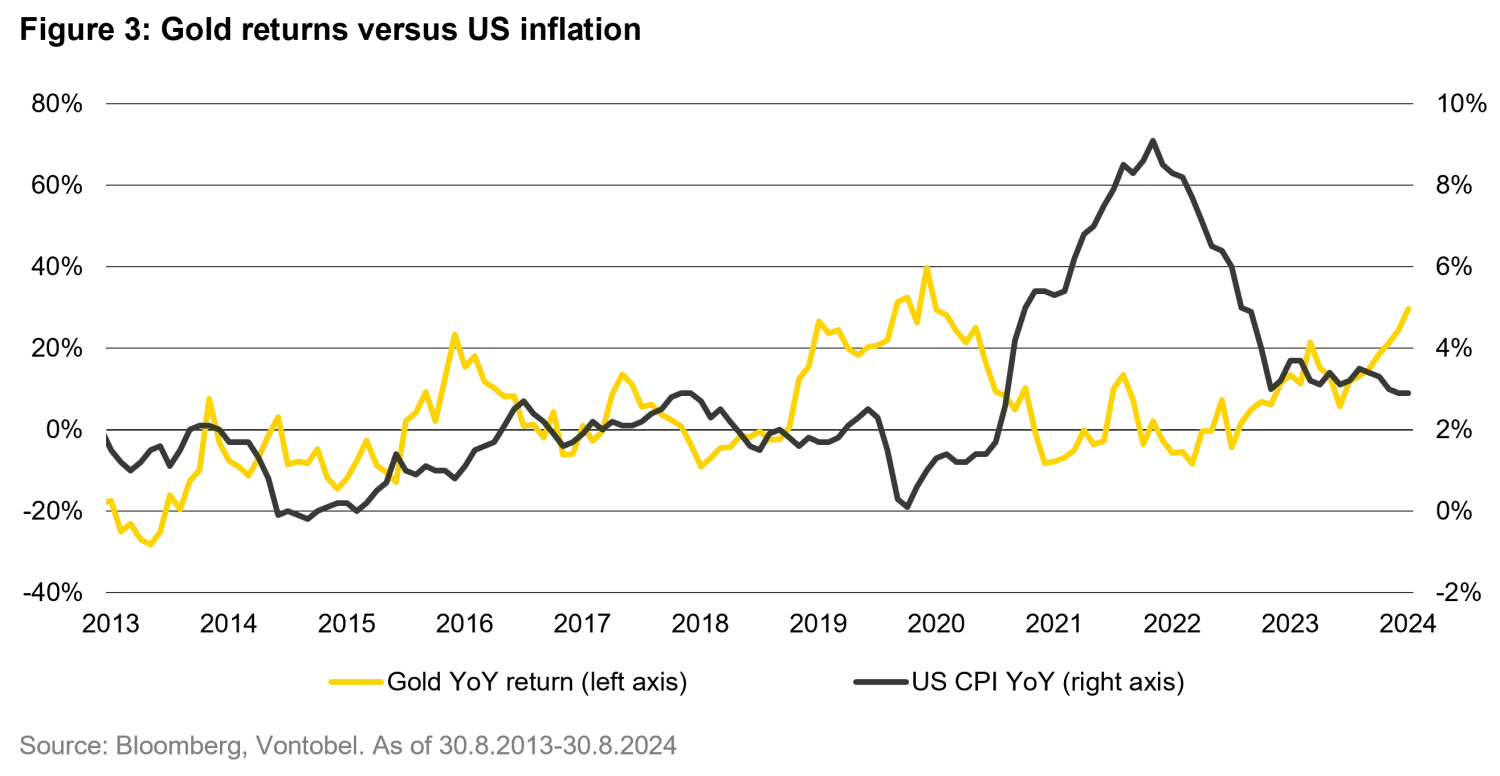

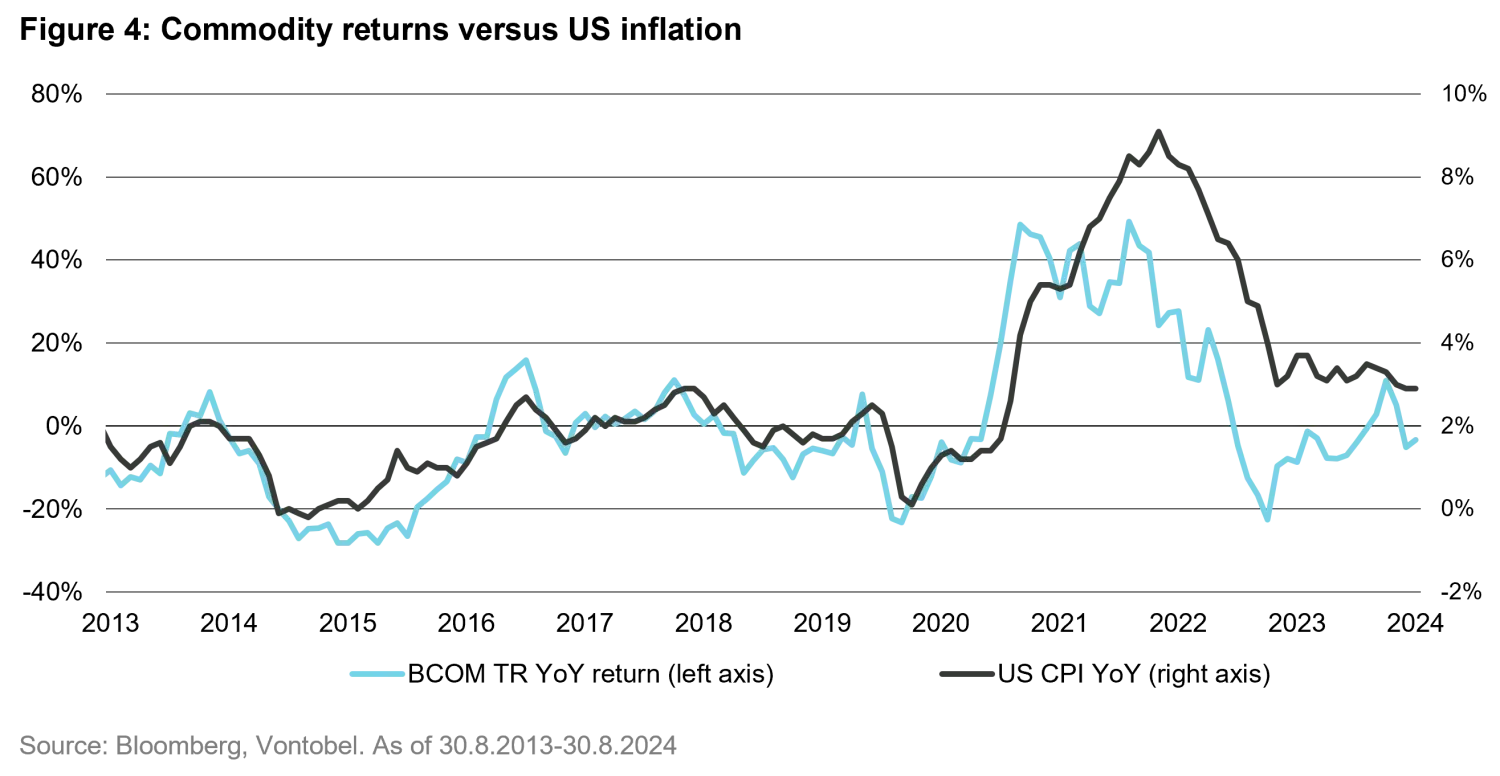

The number one reason why investors hold gold in their portfolio is to have a sufficient inflation hedge. In recent years, this criterion would naturally be top of mind. However, contrary to popular belief, gold is not the best inflation hedge. In fact, a broad basket of commodities does a better job than gold alone. Figures 3 and 4 show year-on-year returns of ‘just gold’ and ‘broad commodities’ over time versus the US Consumer Price Index (CPI), the reference inflation index, respectively.

Commodities as an asset class include a wide variety of components, many of which are at the heart of a functioning society, including food and energy. When the cost of living rises during inflation, the cost of many of these resources rise in tandem. Indeed, one of the main complaints of those contending with an inflationary environment include prices at the grocery stores and at the gas pump. As illustrated in Figure 4, the Bloomberg commodity index better correlates with US inflation. The only disconnect between the two in the last decade was in 2022, when elevated service inflation caused headline inflation to rise further, while inflation in primary goods already eased. But gold does not traditionally perform in this manner, and is even negatively correlated with inflation in the last decade. Unlike energy and soft commodities, the price of gold does not directly correlate with inflation rates.

The reason why gold is not correlated to inflation rates lies in the central bank reaction to rising inflation. Central banks typically raise interest rates as a way to tame rising inflation. But interest rates act as opportunity costs for gold, which does not generate any yield. As a result, investors tend to shift their money away from gold into higher yielding bonds or money markets funds. This is the reason why global gold ETFs experienced major outflows in the last 2 years. While gold has rallied in the recent inflationary environment (20 percent in the last 12 months), this is less directly connected to inflation itself and more related to more aggressive central bank buying. Central banks these days are abating their USD reserves and stocking up on gold.

It seems obvious that broad commodities correlate with inflation, because inflation is to a large extent measured on a basket of those very same commodities. But if that was so obvious, why is it then that most investors still buy gold as an inflation hedge? We think that this has to do with the (historically) better accessibility of the asset class. Before derivatives and other liquid instruments came to the market that offer investors access to a broad basket of commodities, gold investment was the easier route. With commodity funds available in the market, allowing investors to gain exposure to a broad, diversified basket of commodities, this is no longer the case.

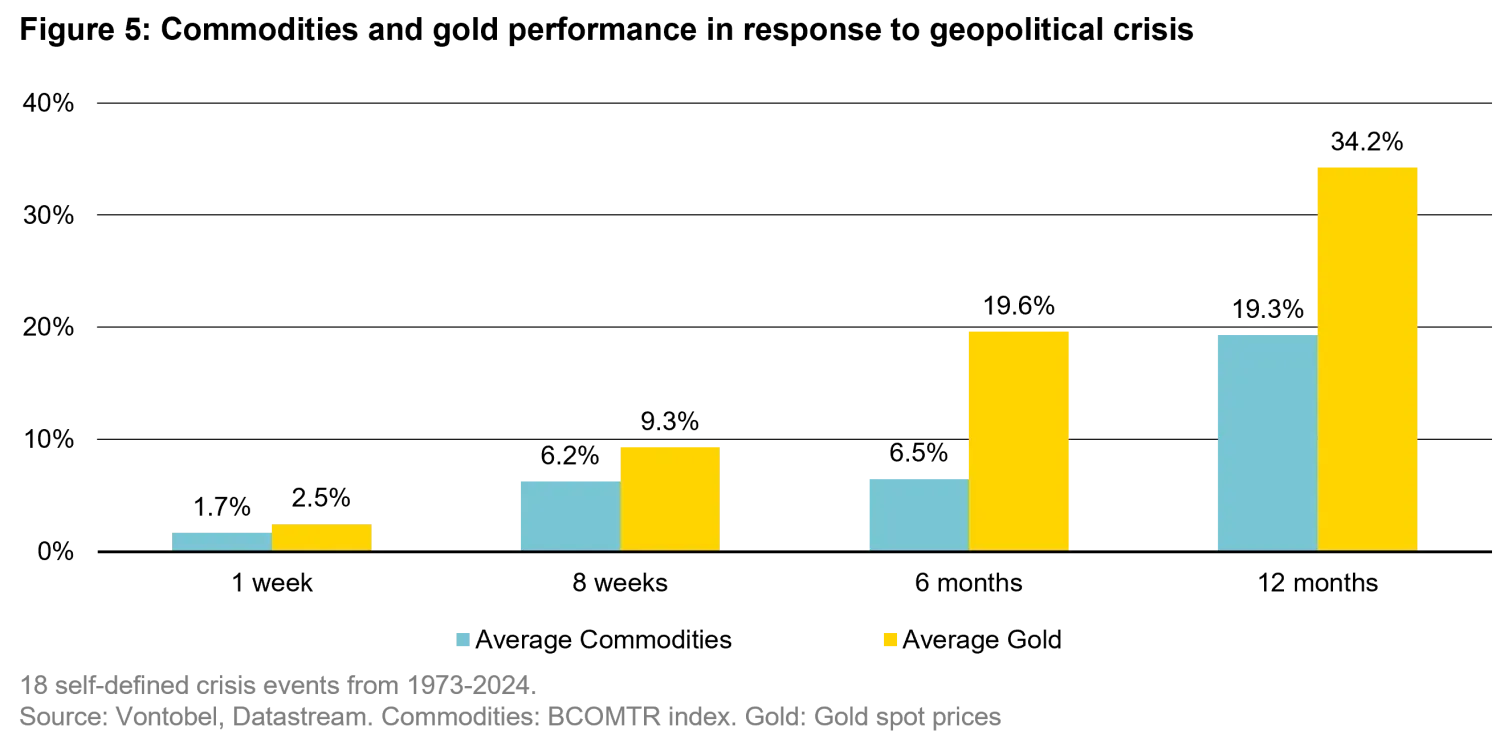

Gold is also considered as a safe haven against geopolitical shocks, and indeed lives up to this reputation. Figure 5 depicts the average performance of gold and commodities following 18 crisis events that we identified between 1973 and today. The averages were calculated across all 18 crisis events, at 1 week, 8 weeks, 6 and 12 months after the onset of the crisis. The analysis shows that gold has particularly outperformed as a geopolitical hedge.

However, a broader basket of commodities can also operate as a shield against geopolitical risks, (but to a lesser extent than gold alone), as resources like oil and gas are usually in the crossfire of crisis events. A good example of this is the Russia Ukraine war that began in 2022. Russia is a major oil and natural gas producer, but it’s also the most important wheat exporter in the world, as well as producer of metals such as palladium, nickel or aluminum. Not surprisingly, the Bloomberg Commodity TR Index rose 18 percent in first half of 2022 (Source: Bloomberg). Meanwhile, equities (MSCI World Total Return Index) fell 21 percent in the same time span.

Despite commodities being a volatile asset class at times, it stands to benefit from multiple long-term trends as mentioned in our former Quanta Byte on commodities. On the one hand, we believe the rise of the middle class in emerging markets may increase demand for soft commodities like meat, and population growth in those regions may increase demand for energy overall, including oil and gas.

On the other hand, the turn to Net Zero in developed economies, including regulations that favor the increased purchase and use of electric vehicles (EVs) will bump demand for metals that are essential in their construction like copper, aluminum, silver, platinum, tin, and nickel. In addition, demand for biofuels may ramp up, drawing on soft commodities like grains.

It stands to reason that a portfolio that includes oil and gas, as well as metals and soft commodities can result in not only stability, but positive growth in response to these trends. In addition, the energy transition may bring protracted periods of inflation in the future as we may see a shortfall in essential resources. By investing in these commodities that are causing this so called “greenflation”, investors can hedge themselves against a potentially unfavorable trends for other assets in their portfolios.

While gold has long been a preferred, and rightly so, asset for hedging against geopolitical shocks, a broader approach to commodity investments can offer enhanced benefits that gold alone cannot provide. By adding a wide range of commodities to a traditional gold allocation—such as energy, metals, and agricultural products—investors can achieve superior diversification, a better hedge against inflation, and a hedge against geopolitical shocks that involve the energy sector. An exposure to broader commodities also offers investors an option to participate to a wider range of opportunities, as they stand to benefit from secular trends such as emerging market development and energy transition. In short, we are advocating investors to consider adding an exposure to a broader commodity basket in addition to their traditional gold allocations.